Shares of Macy’s, Inc. (NYSE: M) remained red on Tuesday. The stock has dropped 14% over the past three months. The retailer is scheduled to report its third quarter 2024 earnings results on Tuesday, November 26, before market open. Here’s a look at what to expect from the earnings report:

Revenue

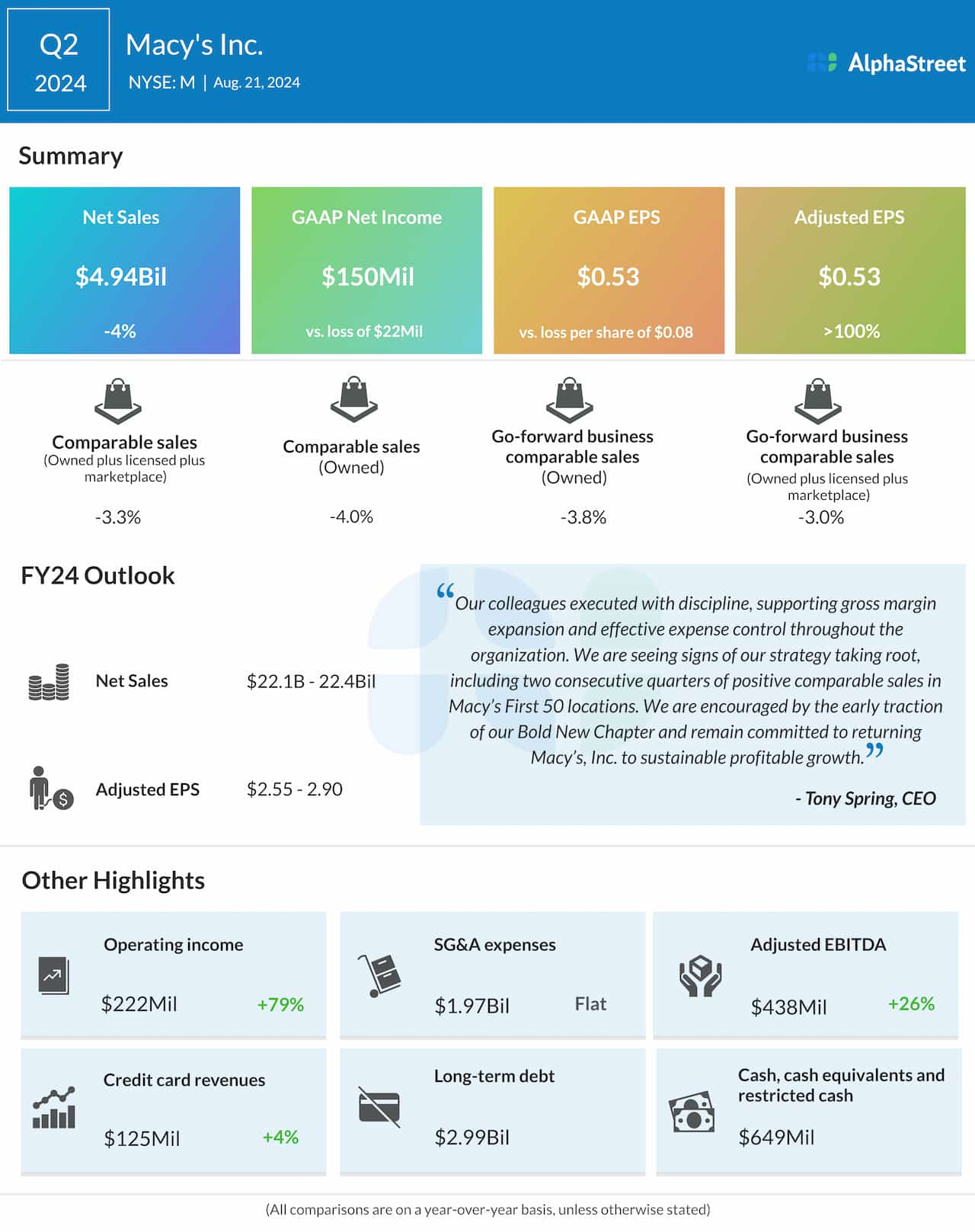

Macy’s has guided for net sales of $4.70-4.82 billion for the third quarter of 2024. Analysts are projecting revenue of $4.72 billion. This compares to sales of $4.86 billion reported in the third quarter of 2023. In the second quarter of 2024, net sales dropped nearly 4% year-over-year to $4.9 billion.

Earnings per share

Macy’s has guided for adjusted EPS in Q3 2024 to range between a loss of $0.04 per share to earnings of $0.01 per share. Analysts are estimating a loss of $0.01 per share for Q3. This compares to adjusted EPS of $0.21 reported in Q3 2023 and $0.53 reported in Q2 2024.

Points to note

Against an uncertain macroeconomic backdrop, consumers are likely to have remained discerning in terms of their discretionary spending. Macy’s had anticipated a heightened promotional environment for the back half of the year. The company has been aligning its assortments and strengthening promotions to provide value, and these actions may have had an impact on the top line in the third quarter.

Meanwhile, Macy’s is making progress on its Bold New Chapter strategy and the performance of its first 50 go-forward stores has been encouraging. In Q2, these stores delivered a comp sales gain of 1%. These locations also saw higher traffic and conversion compared to other go-forward locations, with all merchandise categories witnessing improvement. These trends may have continued in the third quarter.

Macy’s expects other revenues to be around $152 million, including credit card revenues of approx. $110 million, in Q3 2024. Last quarter, other revenues amounted to $159 million, while credit card revenues totaled $125 million.

The retailer expects gross margin for the third quarter to be 40.3-40.5%, and end-of-quarter inventories to be up mid-single-digits versus last year. In Q2, gross margin improved 240 basis points YoY to 40.5%, helped by lower discounting. Merchandise inventories increased 6% YoY.