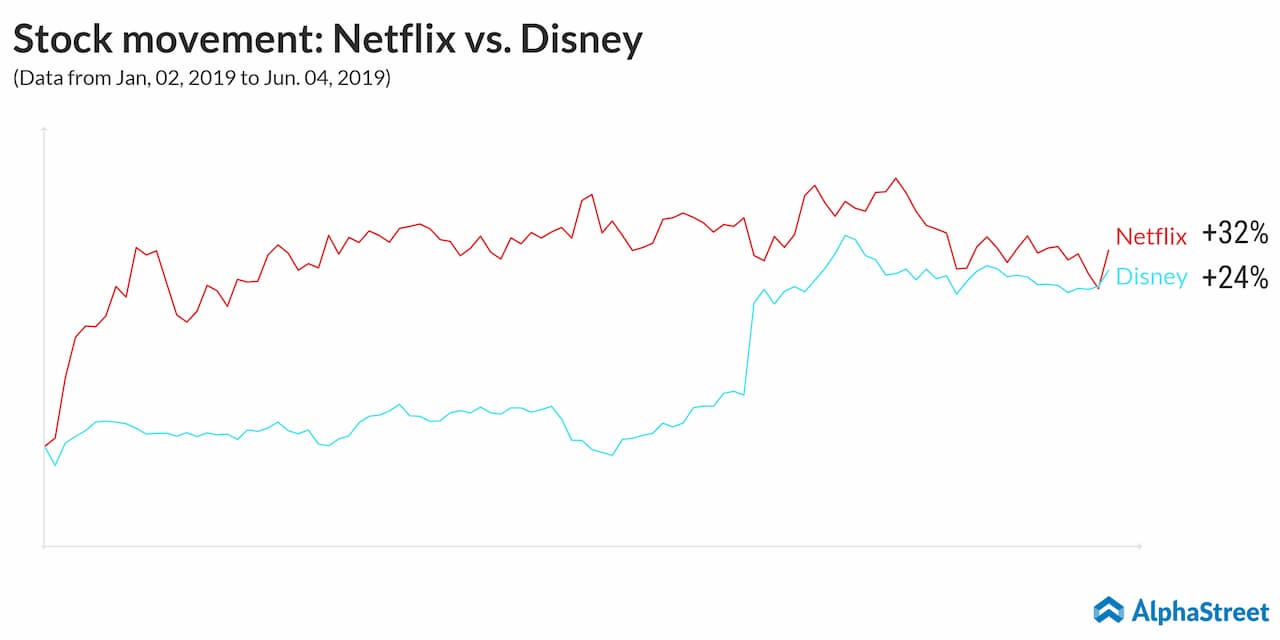

Thanks to some great content,

Netflix (NASDAQ:

NFLX) is often perceived as the future of video content. It has revolutionized

the way we consume content, and started creating high-quality original content even

before its rivals could think of launching a pursuit.

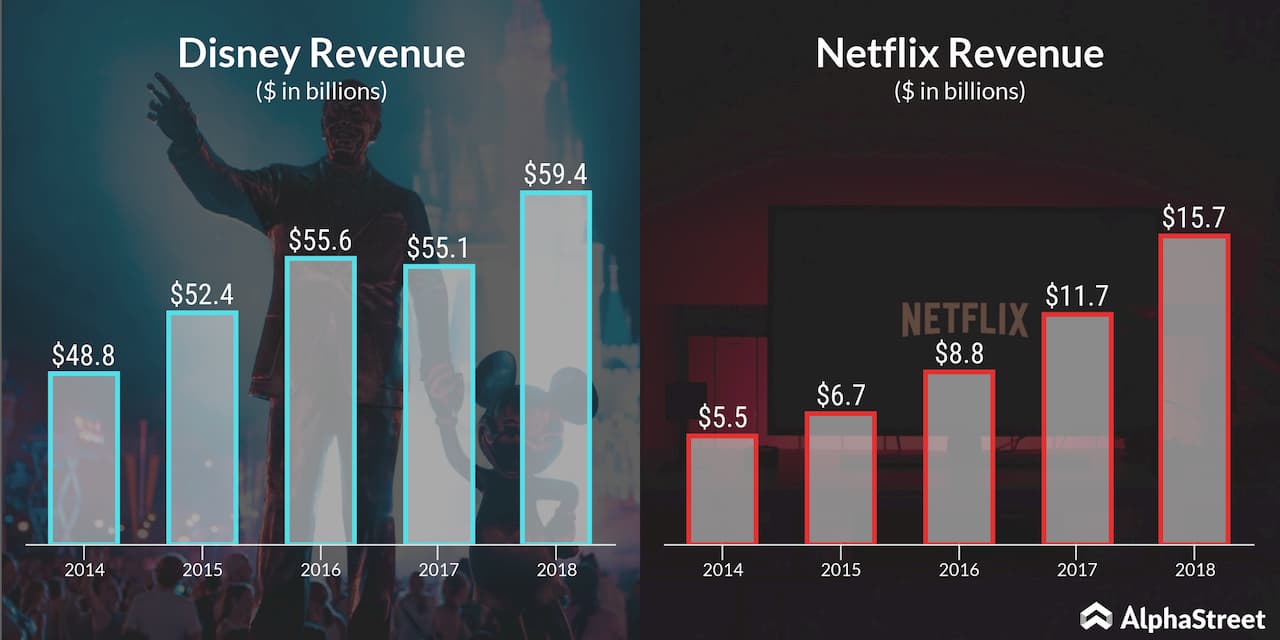

But there has been one thing that has been worrying even the most bullish investors: The ever-increasing spend on content, which has been squeezing margins, despite steady growth in customers additions. This concern should escalate once Netflix’s biggest rival Disney (NYSE: DIS) enters the streaming space in another five months.

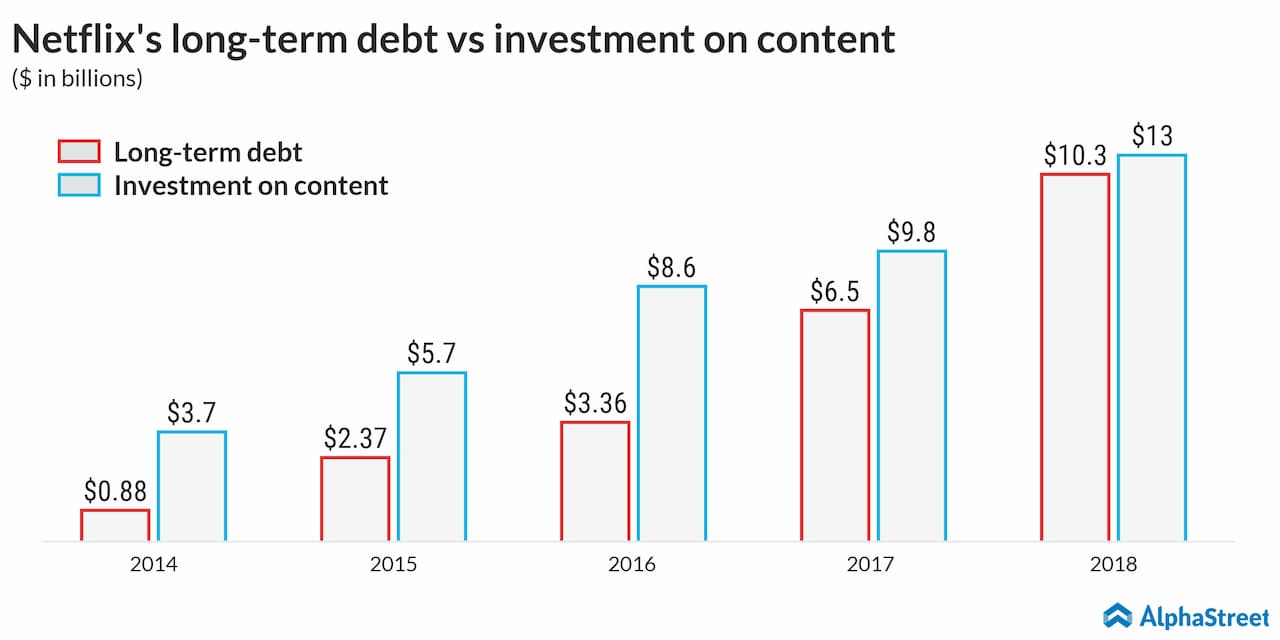

With the arrival of Disney, which comes with an artillery of popular content creators including Marvel, ESPN, and Pixar, Netflix will be forced to raise its already sky-high content costs. Netflix’s spend on content has soared over 250% between 2014 and 2018, which in turn, has lifted its long-term debt more than 10 times.

Wall Street expects Netflix’s content spend to increase to $13 billion this year.

Disney will also have to invest more cash into original content, but its dominant presence in the movie-production space is a clear advantage. For example, Disney had produced four of the top-grossing movies last year – Avengers: Infinity War, Black Panther, Incredibles 2 and Bohemian Rhapsody. If Disney+ (Disney’s streaming service) is the only medium to rewatch these blockbusters, that itself makes the service attractive to users at no extra spend on content or marketing.

Read: The Walt Disney Company (NYSE:DIS) Q2 2019 Earnings Conference Call Transcript

In addition, Disney also has a majority stake in Hulu, arguably the fastest growing streaming company, as well as slew of popular kids’ content. Competitively priced at almost half the subscription fee as Netflix, Disney+ turns out to be a very attractive package.

Netflix is not in a position to experiment with its pricing, with margins already at a threshold level. Hence there is no denying the fact that, even with great content, Netflix would be at a slight disadvantage over this new rival. Netflix may have taught the millennials a new way of watching content; it may have close to 150 million global users, a vast portion of them being brand-loyal binge watchers, but a better deal is a powerful thing.

READ: American Airlines stock hits a 3-year-low, yet risks galore

Disney also enjoys a decent subscriber base in the streaming space. Over 2 million people use ESPN+ and over 25 million have Hulu subscription. Barclays analysts predict that Disney’s overall user base would expand to a staggering 1,170 million in the next six years.

While we still love Netflix,

Disney seems to be a more prospective candidate to take over the Iron Throne of

content.

All hail Mickey the Mouse!

Get access to timely and accurate verbatim transcripts that are published within hours of the event.