After being hit by supply chain issues last year, network gear maker Cisco Systems Inc. (NASDAQ: CSCO) is almost back on track amid continued innovation in its core networking hardware business. The company has successfully transitioned into subscription-based model and is currently busy revamping its strategy with focus on new opportunities in areas like cybersecurity and artificial intelligence.

At the Bourses

Over the years, the San Jose-headquartered tech firm’s profit and revenue topped expectations consistently, bringing cheer to its stakeholders. Interestingly, the business has stayed unaffected by adversities like the pandemic and economic slowdown, and all the key metrics indicate positive momentum.

Cisco’s healthy financial performance did not insulate its stock from the recent stock market mayhem and tech selloff. However, the stock is recovering steadily from the sharp fall in the second half of last year, but it remains well below the 2021 peak. The valuation is favorable, and CSCO is one of the cheapest tech stocks right now. Moreover, the company pays a reasonably good dividend.

Cisco executives are optimistic about maintaining decent revenue growth in the remainder of the fiscal year, though last year’s exceptionally strong performance makes comparisons tough. Encouraged by the positive third-quarter outcome, the management raised its fiscal 2023 financial outlook — currently targets 10-10.5% revenue growth and adjusted earnings per share between $3.80 and $3.82.

Opportunities

Overall, the company’s prospects look bright, thanks to the supply chain recovery, healthy backlogs, and recurring revenue streams. Operating cash flow rose to a record high in the third quarter. As far as long-term growth is concerned, the leadership bets on continued increase in subscriptions/recurring revenue and new opportunities in cybersecurity, which has become a key priority for many enterprises.

From Cisco’s Q3 2023 earnings call:

“We already see early design wins in AI infrastructure and continue to see other wins and competitive displacements, leading to continued share gain in this space. In our networking business, we remain focused on building solutions that drive a higher return on investment and sustainability. In March, we introduced 800-gig capability to our Cisco 8000 platform with the industry’s first 28.8 terabit line card powered by Cisco Silicon One ASICs and pluggable optics.”

Cisco Security Cloud, an integrated cloud-based platform for securing on-premises, cloud, and hybrid environments, is designed to support innovations in the changing technology landscape. The company is already using predictive AI extensively across the portfolio, and some of the leading AI models run by hyperscalers are using its core networking technology.

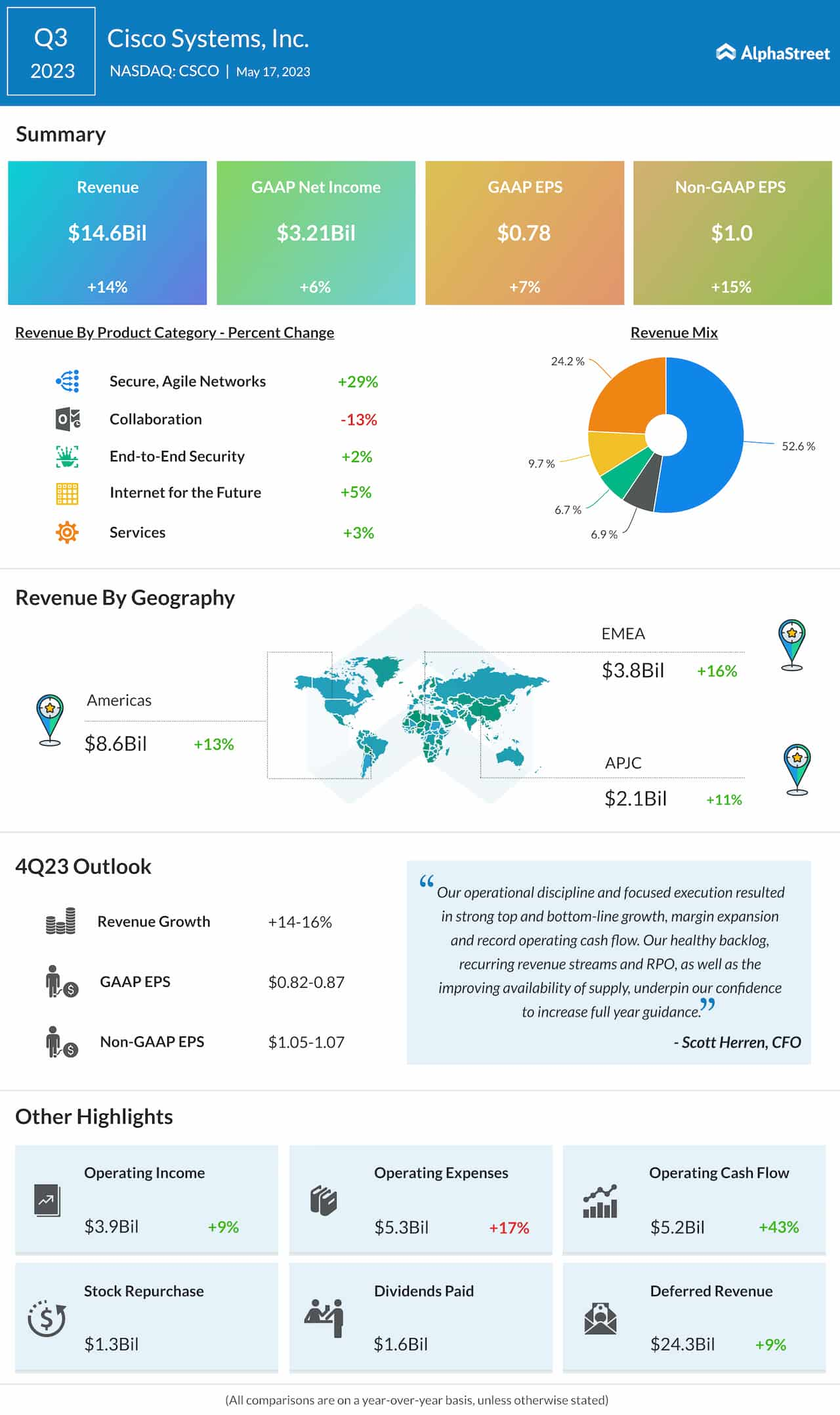

Strong Q3

Once again, Cisco has reported better-than-expected quarterly results – third-quarter 2023 revenues and adjusted earnings increased in double-digits to $14.6 billion and $1.0 per share, respectively. Secure, Agile Networks, the main business division that accounts for more than 50% of total revenues, grew an impressive 29%. Services, the second largest segment, was up 3%.

Reflecting the company’s successful shift to the subscription model, software revenues increased by 18% in the most recent quarter, continuing the recent trend. Remaining performance obligations, a key metric that represents the sum of deferred revenue and backlog, rose to $32.1 billion, and the momentum keeps accelerating.

This week, Cisco’s stock stayed a tad above the 52-week average. It traded higher in the early hours of Thursday, after remaining flat post earnings.