Shares of Campbell Soup Company (NYSE: CPB) were down over 2% on Thursday. The stock has dropped 19% over the past 12 months. For its second quarter of 2024, the company delivered lower sales and flat earnings, which managed to surpass expectations. It reaffirmed its outlook for the full year of 2024, anticipating continued sequential improvement in its top and bottom line.

Sales and profitability

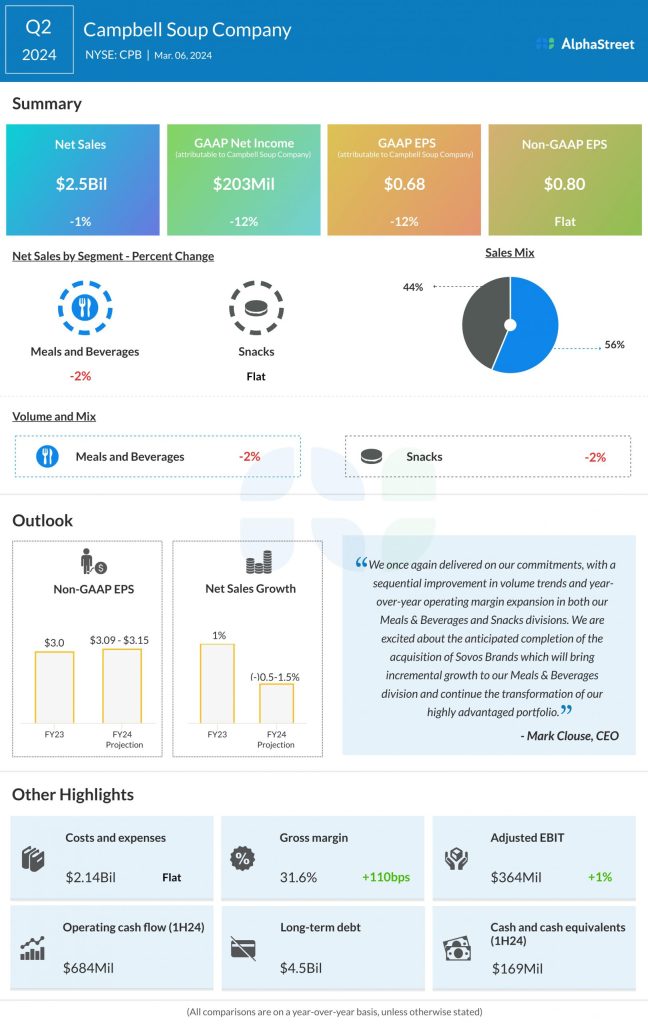

In Q2 2024, Campbell’s net sales decreased 1% year-over-year to $2.5 billion. Organic sales dropped 1%, lapping a 13% increase in the prior-year quarter. The top line benefited from net price realization of 1%, but this was offset by volume/mix, which was down 2% versus last year.

As mentioned on its quarterly call, Campbell anticipates a modest sequential improvement in its top line through the remainder of FY2024. It expects to see flat to low single-digit organic sales growth in the third quarter, with continued sequential improvement in the fourth quarter.

Adjusted EPS of $0.80 remained flat in Q2 2024 compared to last year. Gross margin improved to 31.6% from 30.5% last year.

During the second half of 2024, Campbell expects to see earnings growth and margin progress, especially in the fourth quarter, helped by improvements in volume and mix, moderate inflation levels, and the effect of productivity improvements currently in progress. In Q3 2024, adjusted EPS is expected to be in the lower $0.70 range.

Segment performance

In Q2, net sales in the Meals & Beverages segment declined 2%, on a reported and organic basis, to $1.4 billion. The decrease was driven mainly by declines in US soup, beverages, and Pace Mexican sauces. US soup sales were down 3%, primarily due to a drop in sales of ready-to-serve and condensed soups. The decrease in soup was partly offset by an increase in broth.

Looking at the rest of the year, Campbell remains optimistic about the growth and margin trajectory of this business. Customers continue to give priority to value as they cook more meals at home, prepare stretchable meals, and make smaller and less frequent shopping trips. The company believes its soup portfolio is well positioned to cater to these needs. It is also seeing strength in its condensed cooking and broth portfolios.

Campbell is bullish on the long-term outlook for ready-to-serve soup, based on innovation in the Chunky brand and the expansion of Pacific ready-to-eat soup. It is also optimistic about the addition of the Rao’s soup line, which will come with the Sovos acquisition.

Sales in the Snacks segment remained flat at $1 billion on a reported basis and increased 1% on an organic basis compared to last year. Organic sales growth was driven by a 4% growth in power brands. The company saw strong performance from brands such as Goldfish, Lance, Kettle Brand, and Cape Cod. It remains optimistic about its core portfolio in this segment.

Outlook

For the full year of 2024, Campbell expects net sales growth to be down 0.5% to up 1.5% and organic sales growth to be flat to up 2%. Adjusted EPS is expected to range between $3.09-3.15, representing a year-over-year growth of 3-5%.