Shares of the J.M. Smucker Co. (NYSE: SJM) stayed green on Friday. The stock has dropped 8% year-to-date. The company delivered mixed results for the fourth quarter of 2024, as earnings beat estimates while revenue fell short. Here’s a look at its business performance during the quarter:

Quarterly numbers

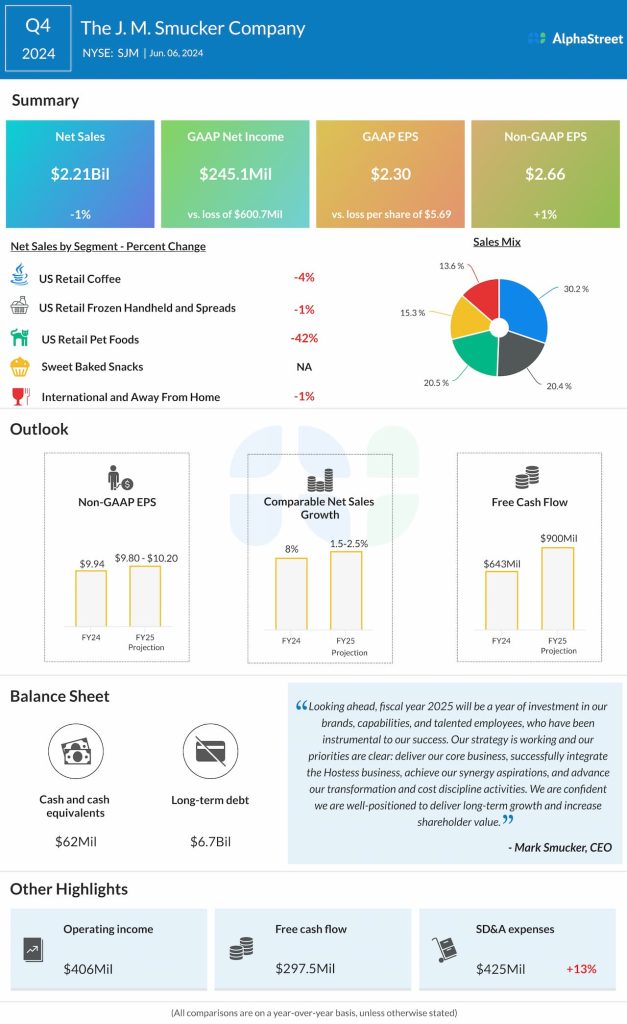

Net sales dipped 1% to $2.21 billion in Q4 2024 compared to the prior-year quarter and missed expectations. Comparable sales increased 3%, benefiting from higher net price realization and favorable volume/mix. Adjusted EPS rose 1% to $2.66 and surpassed projections.

Business performance

In Q4, net sales in the US Retail Coffee segment decreased 4%, mainly due to price declines as the company passed on the benefit of lower coffee costs to consumers. SJM saw volume/mix growth for its Café Bustelo and Dunkin brands during the quarter, but the Folgers brand witnessed a decline due to high competition.

As mentioned on the quarterly conference call, the coffee category continues to experience meaningful inflation. SJM plans to roll out price increases across parts of its portfolio in order to tackle higher green coffee costs that it will incur in the first quarter of 2025. It expects this category to remain resilient despite inflationary pressures and volume declines.

Net sales in the US Retail Frozen Handheld and Spreads segment decreased 1% in Q4. Comparable sales grew 1%, helped by double-digit growth for Uncrustables sandwiches. Net sales for Jif peanut butter were in line with last year. The company is facing tough competition from private label within the category. Sales for Smucker’s fruit spreads declined during the quarter.

Net sales for the Pet Foods segment fell 42%. Excluding the contribution from the divested pet food brands, sales increased 11%. The company saw gains from the Meow Mix, Milk-Bone and Pup-Peroni brands. As indicated on the call, the revamped pet portfolio is performing well in terms of sales and margins.

Within the Sweet Baked Snacks segment, the Hostess brand gained volume share in Q4. The business is expected to benefit from favorable long-term snacking trends, strong innovation and expanded distribution.

Sales in the International and Away From Home segment dropped 1%. Excluding contributions from divested brands, sales rose 8%, driven mainly by double-digit growth in the Away From Home business.

Outlook

For the first quarter of 2025, SJM expects net sales to increase a high-teen percentage, primarily reflecting sales from the Hostess acquisition and volume/mix growth for the business. Adjusted EPS is expected to decline in the low-single digits.

For the full year of 2025, net sales are expected to increase 9.5-10.5%. Comparable sales are expected to increase around 1.5-2.5%. Adjusted EPS is expected to range between $9.80-10.20.