The second half has been highly rewarding for design software maker Adobe Inc. (NASDAQ: ADBE) amid stable demand for digital content solutions. The company has remained unaffected by the virus-related slowdown and movement restrictions so far. It was widely expected and the Silicon Valley tech firm is betting on the strength of its cloud products to repeat the impressive performance in the final months of the fiscal year.

Read management/analysts’ comments on Adobe’s Q3 2020 results

Adobe has been an investors’ favorite for quite some time, sailing through adversities and setting records regularly in recent years. Currently priced slightly above $485 and raring to go up in the coming weeks, the stock is considered a safe bet. Though affordability could be a concern for some of the prospective buyers the valuation looks fine, which is justified by the strong buy rating. The stock has outperformed the market over the past several years, all along creating solid shareholder value. The company has been generating profit that consistently tops expectations.

Strong Buy

Since the hangover of the recent tech selloff is still lingering, there is apprehension over the future of technology stocks, and Adobe is no exception. Nevertheless, the long-term outlook for businesses dealing in cloud, software, and artificial intelligence solutions is quite bullish. It is estimated that digital technology platforms would play a crucial role in ensuring the smooth conduct of business when the new normal fully sets in.

Reaffirming Adobe’s resolve to provide users the ability to create and amplify their stories on multiple platforms, chief executive officer Shantanu Narayen said during his post-earnings interaction with analysts, “Overnight, small mid-size and large B2C and B2B companies shifted every aspect of their customer relationships from acquisition all the way through renewals to digital. As a company that’s been through its own digital transformation, we have a deep understanding of what it takes to be a digital business and that experience makes us the ideal partner to help other companies do the same.”

Looming Uncertainty

It is a fact that Adobe added many new customers this year, especially for the Creative business, and managed to retain most of the existing ones. If the market volatility persists and extends into the next fiscal year, it could result in enterprises slashing investments in non-essential technology assets. I short, when it comes to maintaining the current uptrend, a lot will depend on the course of the pandemic.

Record Revenues

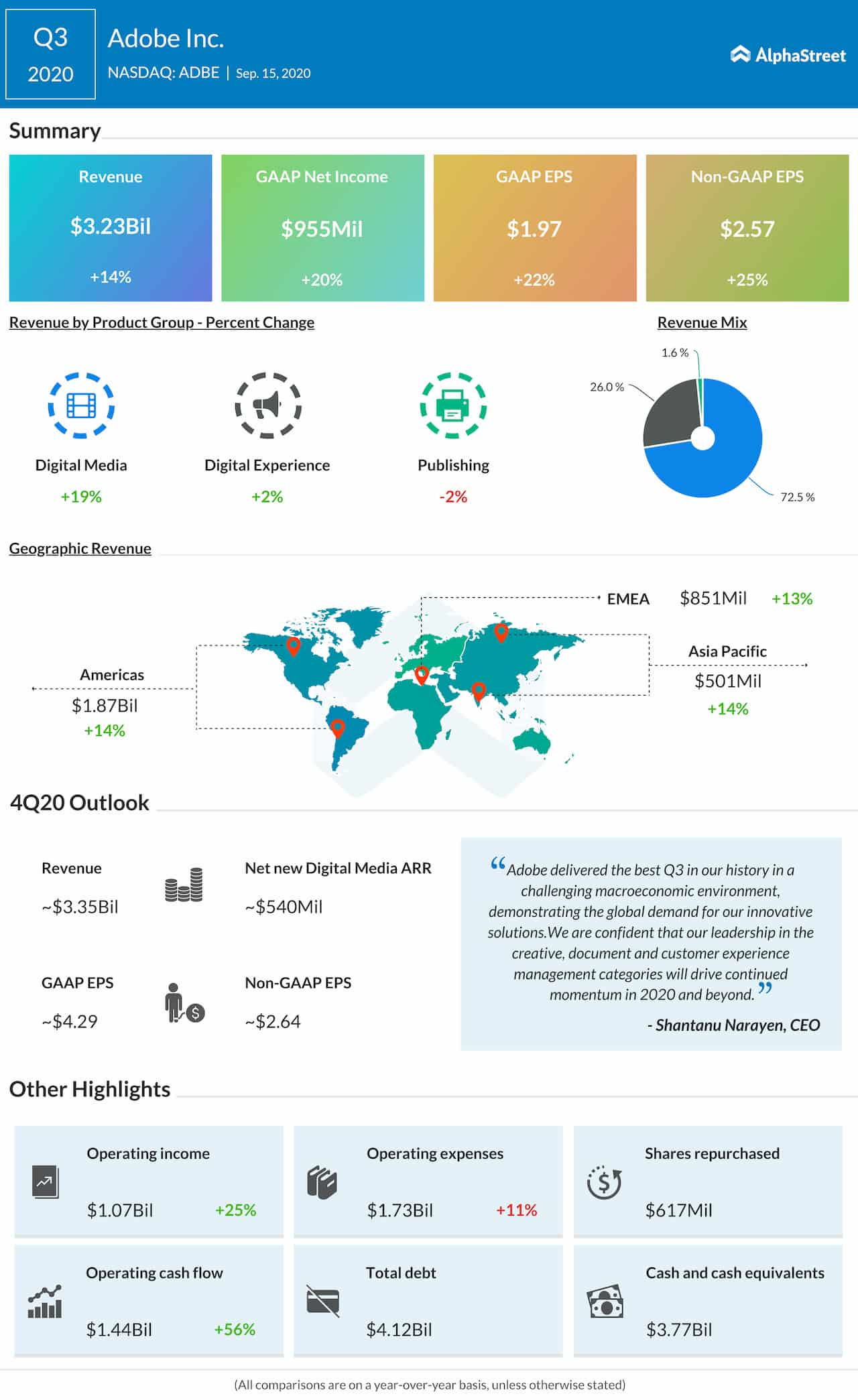

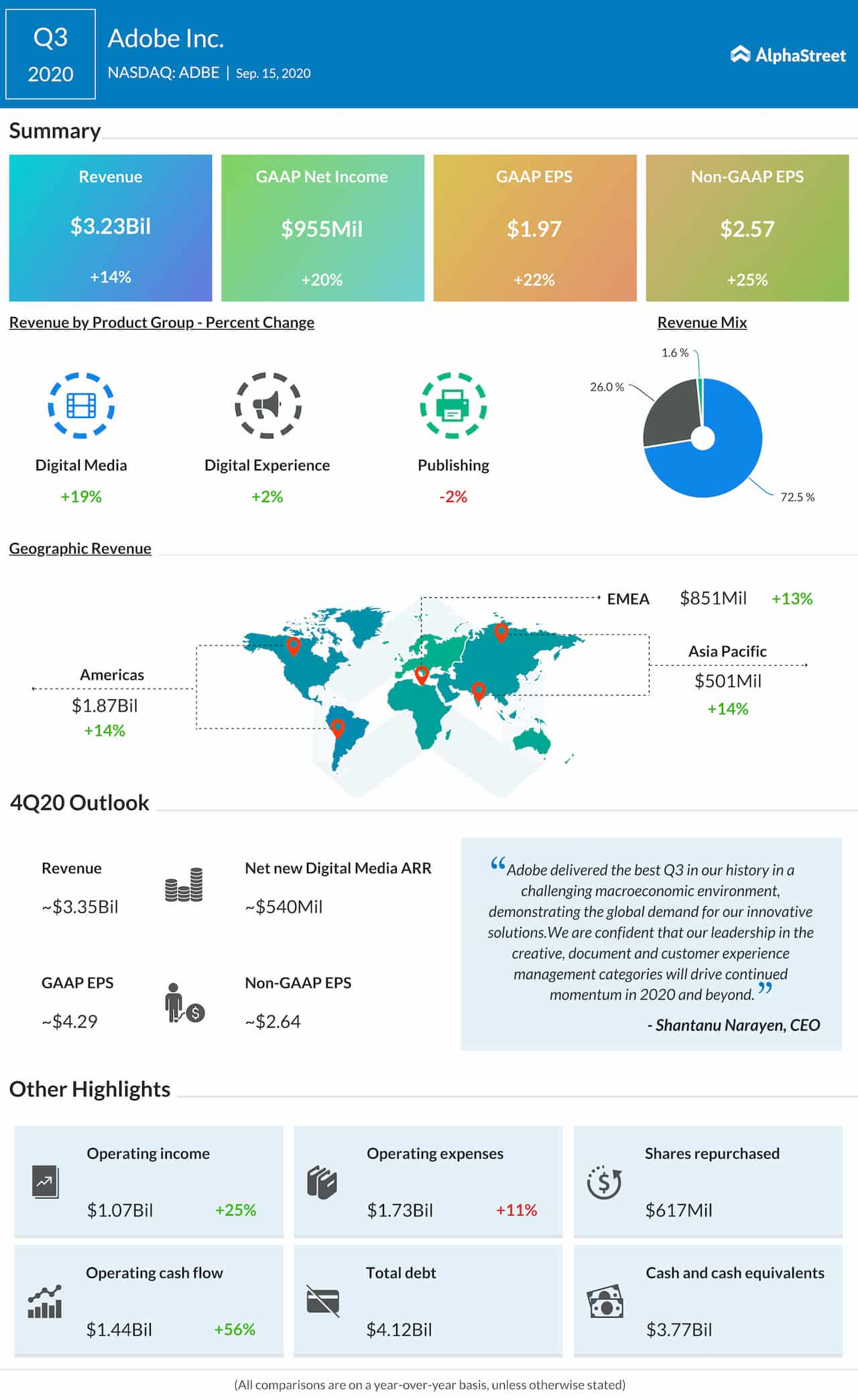

In the third quarter, the core Digital Media segment witnessed robust demand and drove up total revenues by 14% year-over-year to a record high of $3.23 billion. There was double-digit growth across all geographical segments. Consequently, earnings rose by a quarter to $2.57 per share. Though the third quarter is typically a low period for the company due to seasonal factors, that was more than offset by the rapid adoption of virtual tools for academic learning and business purposes.

Exuding optimism that its Creative and customer management prowess would drive growth in the fourth quarter, the management predicts strong earnings and top-line performance that is broadly in line with analysts’ estimates. The bullish view can be linked to the high demand from educational institutions and small enterprises. The SaaS business model followed by the company to license products to end-users helps it maintain recurring revenues and override the cyclical factors.

Future Perfect

Plans are afoot to increase hiring in the current quarter and next fiscal year to better serve customers and expand market share. The reduction in operating expenses due to the lock-down is having a positive effect on cash flow, which gives the management extra leeway to pursue its expansion goals.

Our success was driven by Adobe’s unique ability to draw insights across our business in real-time, utilizing our data-driven operating model. This enables us to understand demand for our solutions, make strategic investments to capitalize on the highest returns and drive engagement and conversion across our channels, most notably, our web properties.

ADVERTISEMENTJohn Murphy, chief financial officer of Adobe

Adobe’s stock made solid gains on Tuesday evening after the market responded positively to the earnings report, but changed course pretty quickly and retreated to the pre-earnings levels. The shares had climbed to a record high earlier this month, after staying on the upward trajectory for several months. They opened Wednesday’s session lower and maintained the downtrend throughout the session.