Semiconductor company Advanced Micro Devices, Inc. (NASDAQ: AMD) had an unimpressive start to the new fiscal year, reporting weak numbers for the first quarter and issuing cautious guidance amid continued softness in chip sales. In the near term, the ongoing slump in the PC industry is likely to weigh on the company’s finances.

For AMD shareholders, there was nothing much to cheer about in 2022 as the stock entered a downward spiral in the early months of the year, after retreating from the peak, and slipped to a two-year low. But it made a modest recovery this year, bringing some relief to investors. Experts, in general, are of the view that the uptrend would continue and the stock is on track to reach $100.

In the Cards

Right now, the low price is the only attraction, but AMD has the potential to create decent shareholder value in the long term, considering the immense growth prospects for the semiconductor industry. It is worth noting that the stock has grown six-fold in the past five years.

The main strength of AMD is its diversified portfolio and competent products, including the latest Zen-based processors that give tough competition to rivals like Intel Corp. Its consumer PC products like the Ryzen CPU and graphics processing units, are considered among the best in the segment. That should enable the company to return to the growth path in the second half when the PC and server markets are expected to gain strength. Following the latest trend in the tech sector, the company is currently working to accelerate its AI roadmap, while rolling out multiple products with a focus on the Data Center and Embedded businesses.

From AMD’s Q1 2023 earnings conference call:

“We remain confident in our ability to grow in the second half of the year, driven by the adoption of our Zen 4 product portfolio, improving demand trends in our client business, and the early ramp of our instinct MI300 accelerators for HPC and AI. Looking longer term, we have significant growth opportunities ahead based on successfully delivering our road maps and executing our strategic data center and embedded property priorities, led by accelerating adoption of our AI products.”

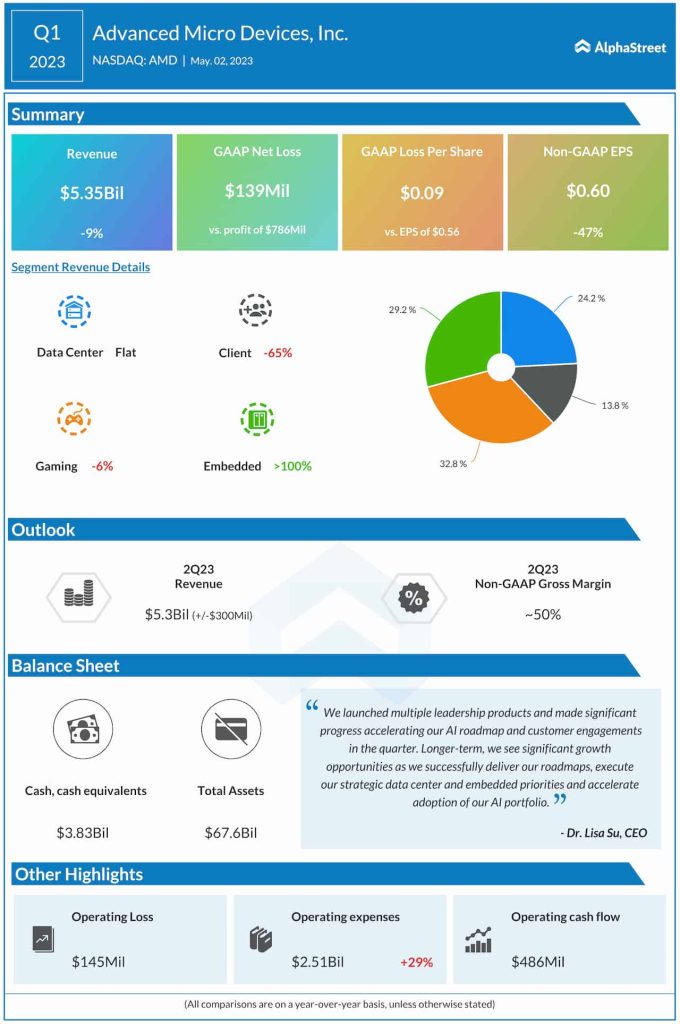

Q1 Outcome

First-quarter earnings and revenue declined but beat estimates, while the tech firm’s outlook for the current period fell short of expectations. The main operating segments contracted during the quarter – The Gaming segment, which develops GPUs for gaming PCs and processors for consoles, contracted 6% and Client revenues dropped a dismal 65%. Meanwhile, revenues of the Embedded business more than doubled, with contributions from Xilinx which joined the AMD fold last year.

Total revenues declined 9% from last year to $5.35 billion in the first three months of 2023. As a result, adjusted earnings fell sharply to $0.60 per share from $1.13 per share in the prior-year period. On an unadjusted basis, it was a net loss, compared to a profit last year. The estimated revenue for the June quarter is around $5.3 billion, which is below the consensus forecast.

After being punished by investors for the unimpressive first-quarter performance and the management’s weak guidance, AMD is yet to recover from the selloff. However, the stock traded slightly higher on Thursday afternoon.