Salesforce, Inc. (NYSE: CRM) this week reported positive first-quarter results and issued bullish guidance but warned of a slowdown in the coming months citing weak enterprise spending and delays in new contracts, mainly reflecting the economic downturn and muted business confidence. Meanwhile, the management is busy streamlining sales and marketing activities, using advanced technologies like artificial intelligence to increase efficiency.

After rebounding from a multi-year low at the beginning of the year, shares of the San Francisco-based customer relationship management platform have been trading well above their 12-month average. Meanwhile, the stock suffered a selloff following the company’s earnings announcement this week, despite the positive results. Investors were apparently worried about the continued deceleration in revenue growth – in the latest quarter, the top line rose at the slowest pace in about 10 years.

Revenue Model

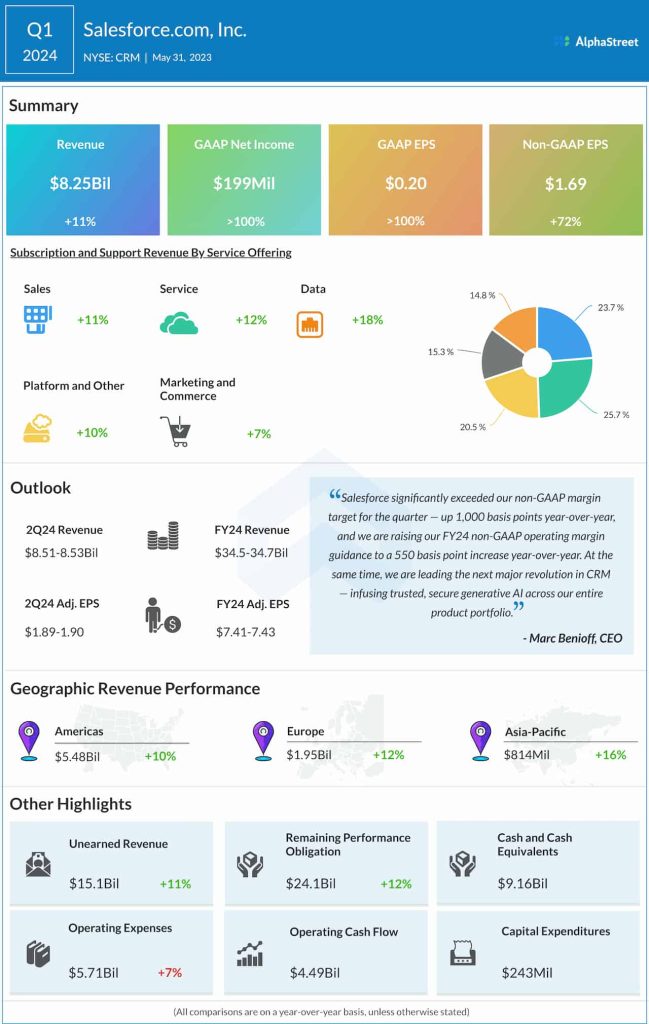

Interestingly, all of Salesforce’s operating divisions play a key role in driving revenue growth since it is almost equally distributed among the four segments – sales, service, data, platform & other, and marketing & commerce. So, a potential weakness in one particular area is unlikely to have a material impact on total revenues. Since there is a slowdown across the board, the management is currently focused on taking measures to boost margins and profitability.

Results Beat

The company has an impressive track record of beating analysts’ earnings estimates, with the bottom line exceeding expectations in every quarter in the past seven years. The top line also exceeded Wall Street’s predictions mostly during that period, and the trend continued in the most recent quarter. Net income, adjusted for special items, surged 72% annually to $1.69 per share in the first quarter. That reflects broad-based growth across all operating segments that pushed up total revenues to $8.25 billion, up 11%. The remaining performance obligation, an indicator of total future performance obligations arising from contractual relationships, rose 12% to $24.1 billion.

From Salesforce’s Q1 2024 earnings conference call:

“Customers continue to scrutinize every deal, and we see elongated deal cycles and deal compression, particularly in our more transactional revenue streams like SMB, create and close, and self-serve. Also, in Q1, our professional service business started to see less demand for multiyear transformations, and, in some cases, delayed projects as customers focus on quick wins and fast time-to-value. But for this reason, we saw a strong performance from some of our fast time-to-value efficiency-focused products with sales performance management, sales productivity, and digital service, all growing annual recurring revenue above 40% in the quarter.”

Outlook

Non-GAAP operating margin increased a whopping 1,000 basis points to 27.6% in the April quarter. Salesforce’s leadership is optimistic about extending the uptrend into the remainder of the year and predicts a 550-basis point margin growth for fiscal 2024, which is higher than the earlier outlook. It also reiterated the full-year revenue forecast of $34.5 billion, up 10% from the last fiscal year. In the second quarter, revenue is expected to grow by 10% about $8.52 billion.

CRM opened Friday’s session lower and maintained the downtrend in the early hours of the session, extending the post-earnings weakness.