While semiconductor firms serving the microprocessor and memory market remained largely unscathed by the pandemic, Analog Devices (NASDAQ: ADI) has faced challenges related to unstable demand and seasonal factors. However, things are changing for the better, and the company’s management is confident of ending fiscal 2020 on a positive note and getting back on track by next year.

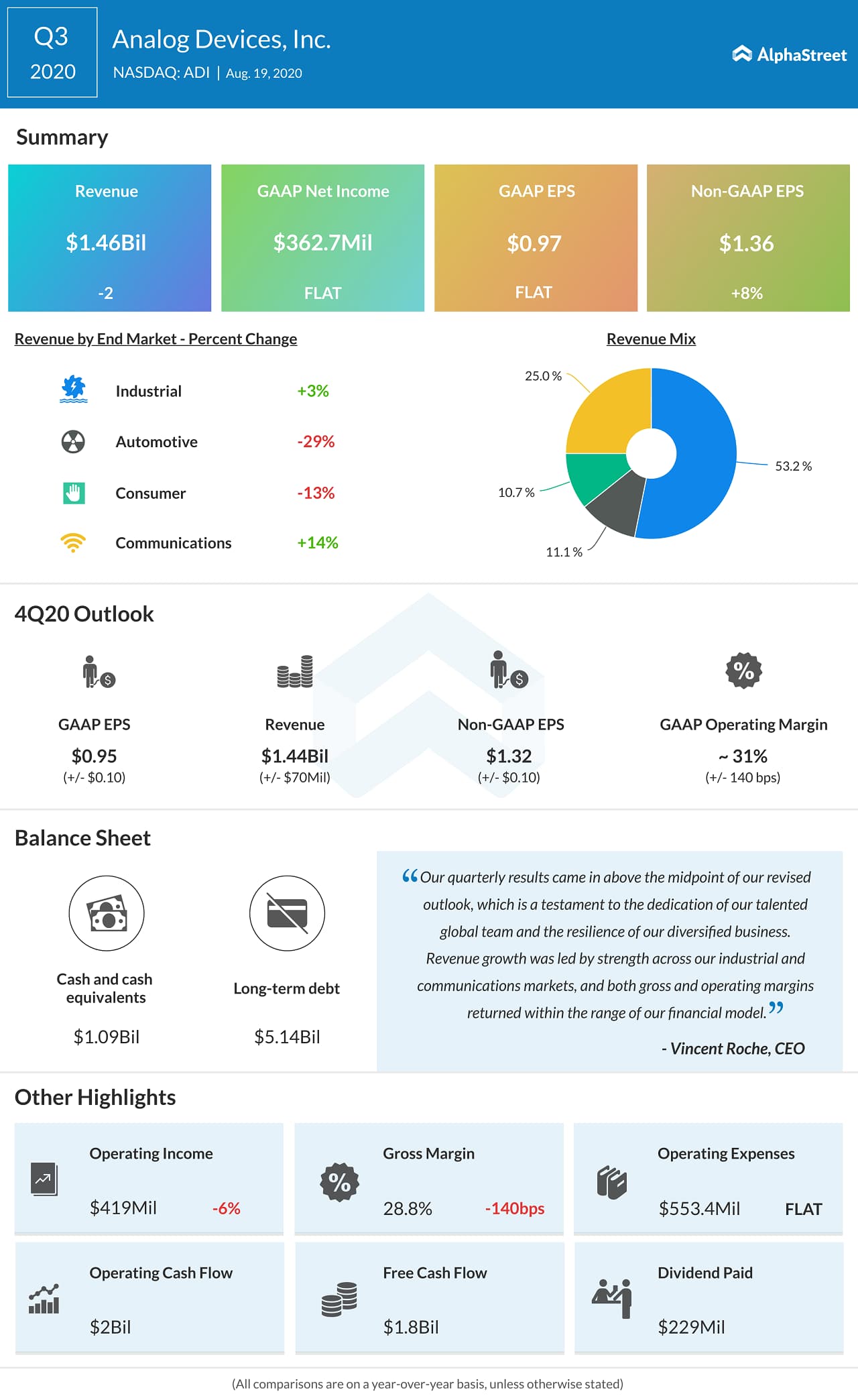

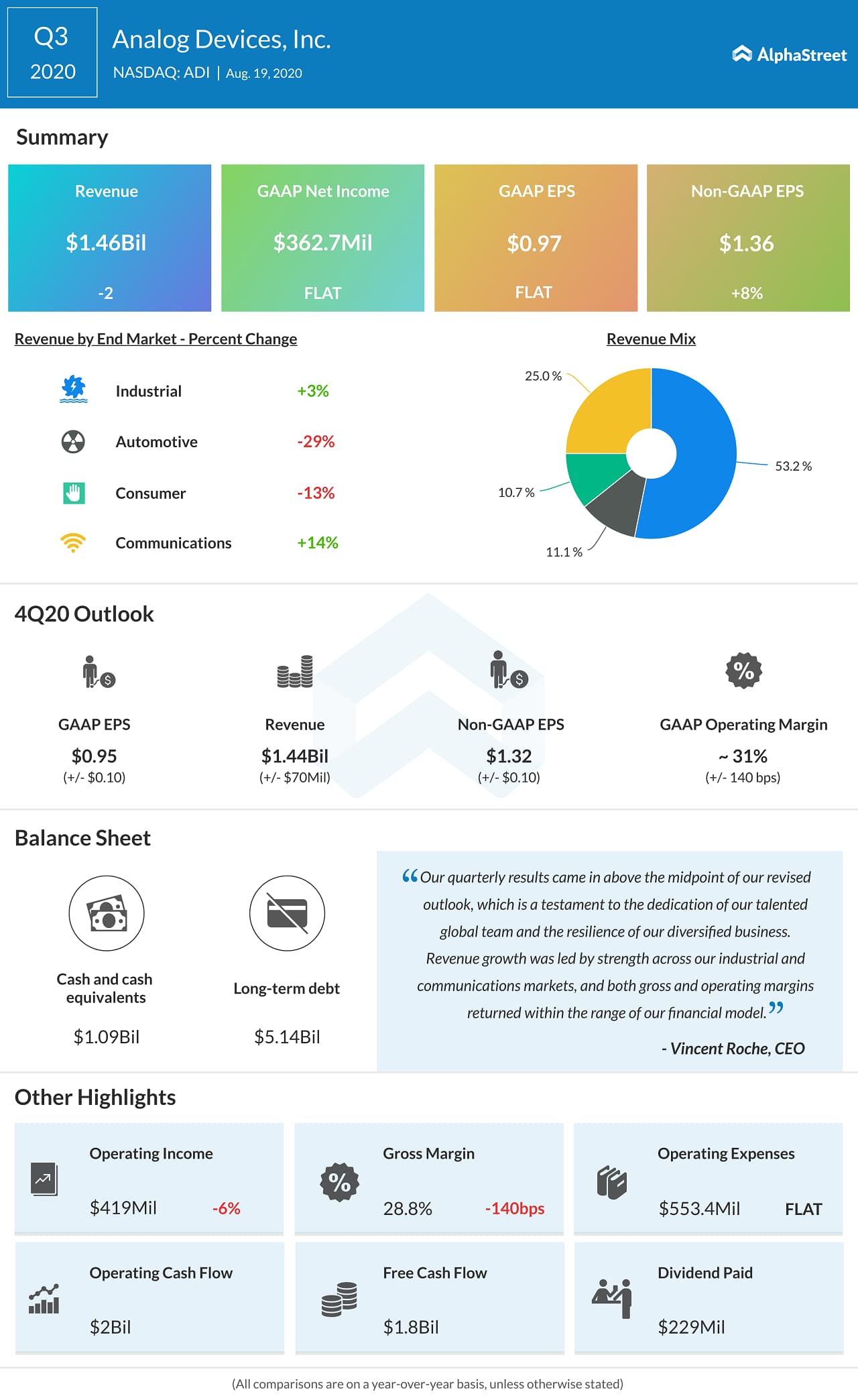

Currently, Analog Devices looks poised to take advantage of the improving demand conditions in areas like aerospace, healthcare, and factory automation. The communications business, which accounts for about 25% of its total business, is recovering from the recent slowdown supported by the 5G ramp and the growing demand for high-speed wireless networks.

Stock Peaks

From this week’s record highs, Analog Device’s stock is probably on its way to breach the $150 mark. Going by analysts’ recommendation, the stock is a strong buy and needs to be closely followed, especially in the run-up to the next earnings release. The management’s decision to reinstate the suspended share repurchase program makes this dividend stock more attractive.

When the company reports its fourth-quarter results on Tuesday, the market will be looking for an 11% rise in earnings on flat revenues. Since the tech firm has been sending out strong signals of a rebound for some time, the relatively high stock price shouldn’t be a concern for prospective investors.

COVID Woes

In the early weeks of the virus outbreak, the Norwood, Massachusetts-based firm came at the receiving end of the widespread disruption caused by it. The company was particularly impacted by the slowdown in the automotive industry, which accounts for more than 10% of its revenues. However, most auto firms have resumed production now, even as the market limps back to normalcy. Another area of weakness is the consumer business, where end products like smartphones and digital cameras fall under the discretionary category.

From Analog Device’s Q3 2020 earnings conference call:

“We saw continued strength in communications across both wireless and wireline applications. Healthcare saw record demand, and other parts of our industrial portfolio such as instrumentation test also performed well. Unsurprisingly, the main area of weakness was automotive, driven by global factory shutdowns and lower vehicle sales.”

Gaming, datacenter help Nvidia stay on the fast track

To complement the recovery process, the company has streamlined capital spending with a focus on new product development, aiming to tap the lucrative B2B segment. The management expects the top-line to benefit from contributions from Maxim Integrated, which joined the Analog Devices fold earlier this year.

Mixed Results

In the third quarter, modest growth in the core industrial business was more than offset by weakness in the automotive and consumer businesses, resulting in a 2% drop in revenues to about $1.5 billion. However, adjusted earnings moved up 8% to $1.36 per share and topped expectations.

Read analysts/managements’ comments on Analog Devices Q3 results

For the shares of Analog Devices, it has been a roller-coaster ride so far this year, but they maintained an upward momentum all along. The stock climbed to a record high this week ahead of the fourth-quarter earnings report. The stock has gained 23% since last year and 19% in the past six months, outperforming the market.