The highlight of Nvidia Corporation’s (NASDAQ: NVDA) latest earnings report was the record performance of its GPU business, which outpaced the data center segment. Being an industry-leading provider of gaming chips, the company continues to benefit from the COVID-induced spike in the demand for video games.

Read analysts/management’s comments on Nvidia’s Q3 earnings

The recent launch of new-generation gaming chips – the Ampere architecture based GeForce 30 RTX GPU series – marked a huge leap from the earlier version and the product was well-received. Analysts see the company’s stock gaining in double digits in the next twelve months. If the current uptrend and favorable demand conditions are any indication, the stock can offer handsome returns for the long term.

Stock Dips

Investors did not find the guidance for the current quarter very encouraging and the stock pulled back from the recent highs soon after the the quarterly release this week. The management has cautioned that revenues could be hit by deferment of a large order from a China-based customer, though it will add to the top-line in the next quarter.

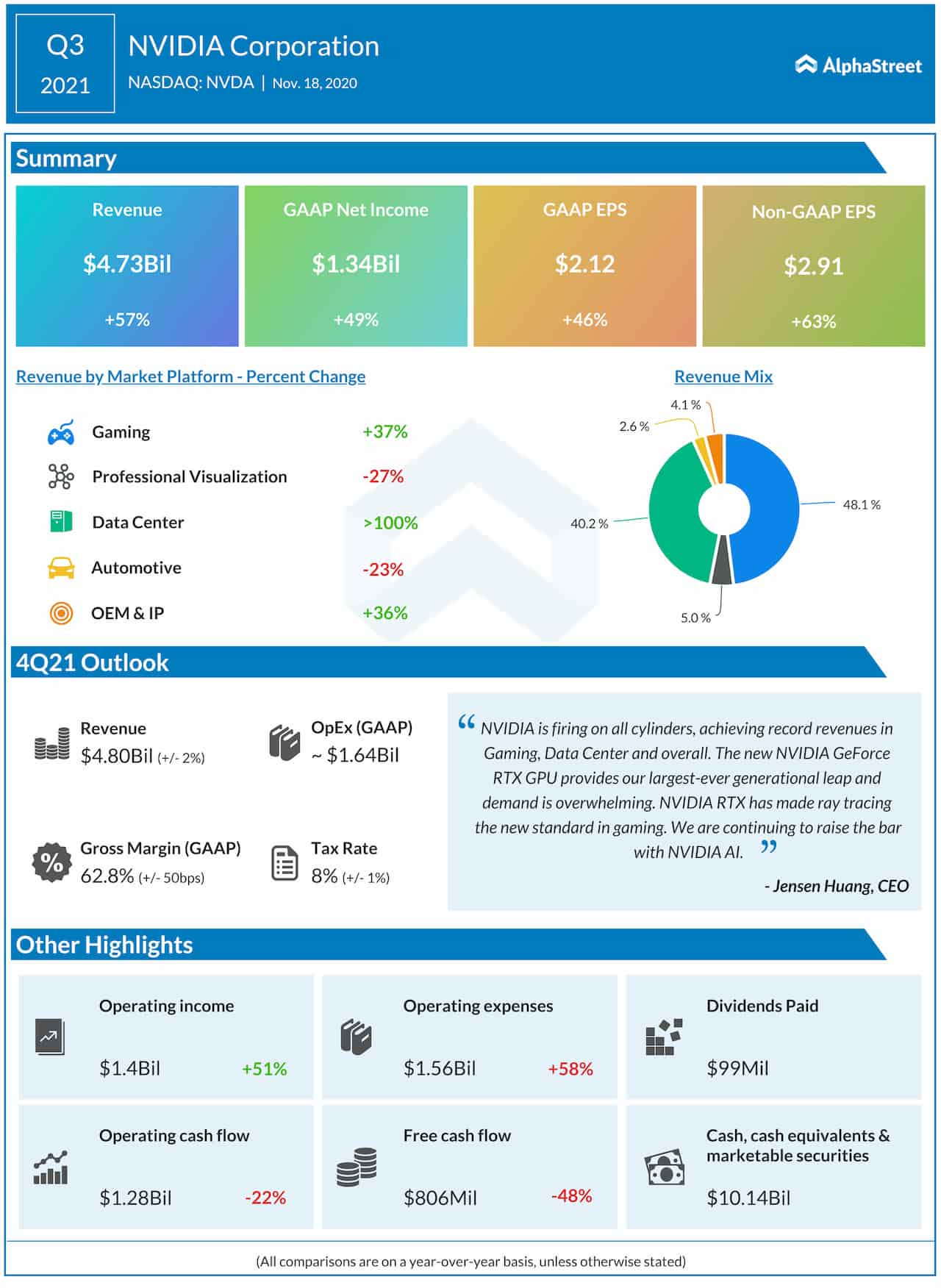

On the company’s estimated fourth-quarter performance, chief financial officer Colette Kress said, “We expect gaming to be up sequentially in what is typically a seasonally down quarter. As we continue to ramp up our new RTX 30 series products. We expect data center to be down slightly versus Q3. With that, we expect computing products to grow in the mid-single digits sequentially, more than offset by sequential decline in Mellanox. We expect continued sequential growth in auto and ProViz though not yet returning to year-on-year growth and we expect a seasonal decline in OEM. Revenue is expected to be $4.8 billion plus or minus 2%.”

Mixed Outlook

Meanwhile, there are concerns that the current capacity is not sufficient for the company to meet the unusually high demand. Also, the non-core businesses – Automotive and Professional Visualization – continue to be impacted by the ongoing disruption. Nevertheless, Nvidia’s long-term prospects look bright, thanks to the steady growth of the GPU business and the AI-powered datacenter segment, which got a major boost after the addition of Mellanox Technologies earlier this year.

The company is poised to maintain the strong momentum for the long-term, with experts predicting that the remote work/learn-from-home culture would prevail in the post-COVID era. Continuing its M&A strategy, the company is on track close the pending acquisition of chip designer Arm in early 2022. The $40-billion acquisition is expected to be immediately accretive to earnings.

Revenues Surge

The response to Nvidia’s new-generation video game chips has been encouraging, which translated into revenues in the third quarter. Adding to the top-line growth, datacenter revenues more than doubled, driving up total revenues by 57% to $4.73 billion. Earnings, adjusted for special items, climbed 63% annually to $2.91 per share. The results also topped the Street view.

“We expect our data center revenue in total to be down slightly quarter-over-quarter. The computing products, NVIDIA computing products is expected to grow in the mid-single-digit quarter-over-quarter as we continue the NVIDIA AI adoption and particularly as A100 continues to ramp,” added Kress.

All you need to know about Intel Q3 2020 earnings results

The stock surged to a record high last week, but pared a part of those gains after the earnings report. Its value more than doubled since the beginning of 2020, all along outperforming the market. The shares moved up about 50% in the past six months alone.