Nvidia Corporation (NASDAQ: NVDA) has once again delivered blockbuster quarterly results, in one of the most closely watched earnings events this season. While the GPU giant beat analysts’ revenue and earnings estimates for the July quarter, continuing the recent trend, the market was focused more on the management’s cautious guidance. As a result, the stock dropped soon after the announcement, before regaining a part of the momentum later.

NVDA has lost more than 10% since peaking in mid-June this year, but it remains one of the best-performing Wall Street stocks. The shares have consistently outperformed the market in the recent past, with the value more than doubling since the beginning of 2024. It is estimated that the stock is on track to cross the $150 mark in the twelve months. Despite the relatively high valuation, Nvidia continues to be a compelling long-term investment.

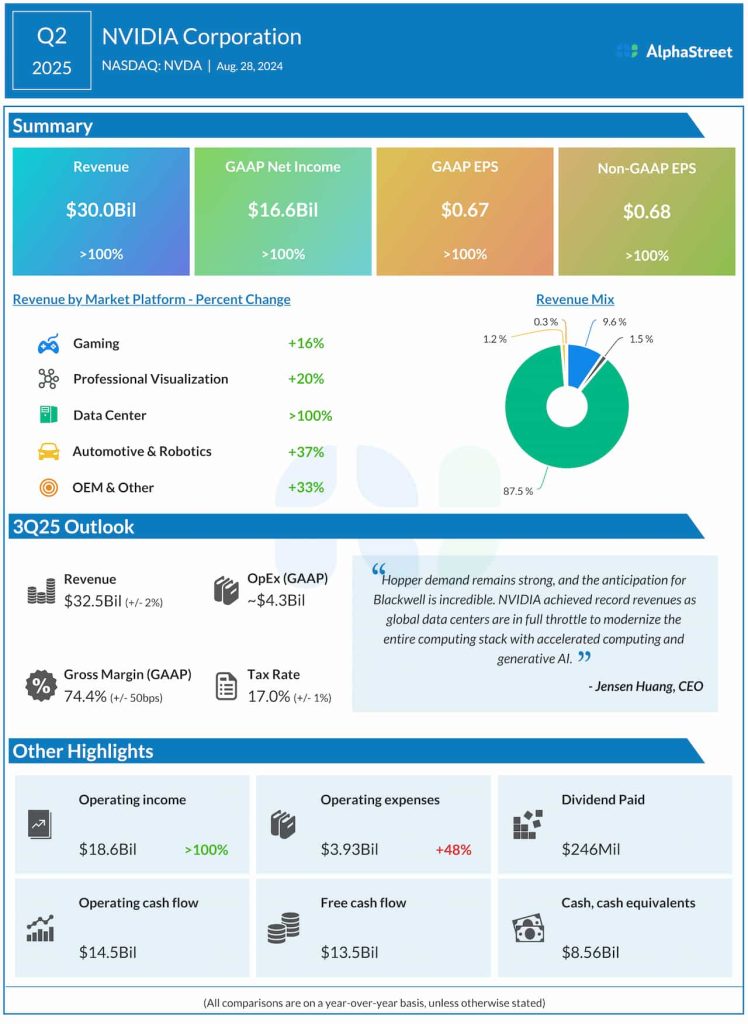

Another Strong Quarter

Second-quarter revenues surged to $30.0 billion from $13.5 billion a year earlier, and topped expectations, reflecting strong performance by the Data Center and Gaming segments. Earnings, excluding one-off items, jumped to $0.68 per share in Q2 from $0.27 per share a year earlier. Nvidia has posted seven consecutive earnings beats. Unadjusted net income was $16.6 billion or $0.67 per share in the July quarter, compared to $6.19 billion or $0.25 per share in the year-ago quarter. The company ended the quarter with an impressive free cash flow of $13.5 billion.

Nvidia is the undisputed king of AI chips, reaping the fruit of continued research and development in that area and aggressive M&A strategy – closed four acquisitions this year alone. Meanwhile, there are reports that the leadership is in talks with Apple to invest in ChatGTP as part of OpenAI’s fundraising initiative. The company is bullish on the prospects of Blackwell, its futuristic chip architecture designed to accelerate the development and deployment of real-time generative AI, while ensuring a high level of security.

Blackwell in Focus

The tech firm is ramping up the production of Blackwell, which is scheduled to hit the market later this year. Considering the high demand, this innovative chip family is expected to bolster revenues starting in the fourth quarter. While the delivery of Blackwell is delayed, it is likely to give the stock a major boost once the company begins volume shipment. Meanwhile, the high costs associated with portfolio expansion and production ramp could put pressure on margins.

Nvidia’s CFO Colette Kress said at the Q2 earnings call, “Demand for Nvidia is coming from frontier model makers, consumer Internet services, and tens of thousands of companies and start-ups building generative AI applications for consumers, advertising, education, enterprise and healthcare, and robotics. Developers desire Nvidia’s rich ecosystem and availability in every cloud. CSPs appreciate the broad adoption of Nvidia and are growing their Nvidia capacity given the high demand.”

Outlook

The company expects revenues to be around $32.5 billion for the third quarter of 2025, which is slightly below the consensus estimate of $32.75 billion. It is looking for a gross margin of approximately 74.4% for the October quarter and sees full-year gross margin in the mid-70%.

On Friday, shares of Nvidia traded a whopping 50% above their 52-week average value of $79.07. The stock maintained an uptrend through the latter half of the session.