Chewy Inc. (NYSE: CHWY) reported a wider loss in the third quarter of 2019 due to higher costs and expenses. The bottom line was wider than the analysts’ expectations while the top line exceeded consensus estimates. However, the online pet supplies retailer raised its 2019 sales forecast.

Net loss was $79 million or $0.20 per share compared to a loss of $78.62 million or $0.20 per share in the previous year quarter. Analysts had expected a loss of $0.16 per share.

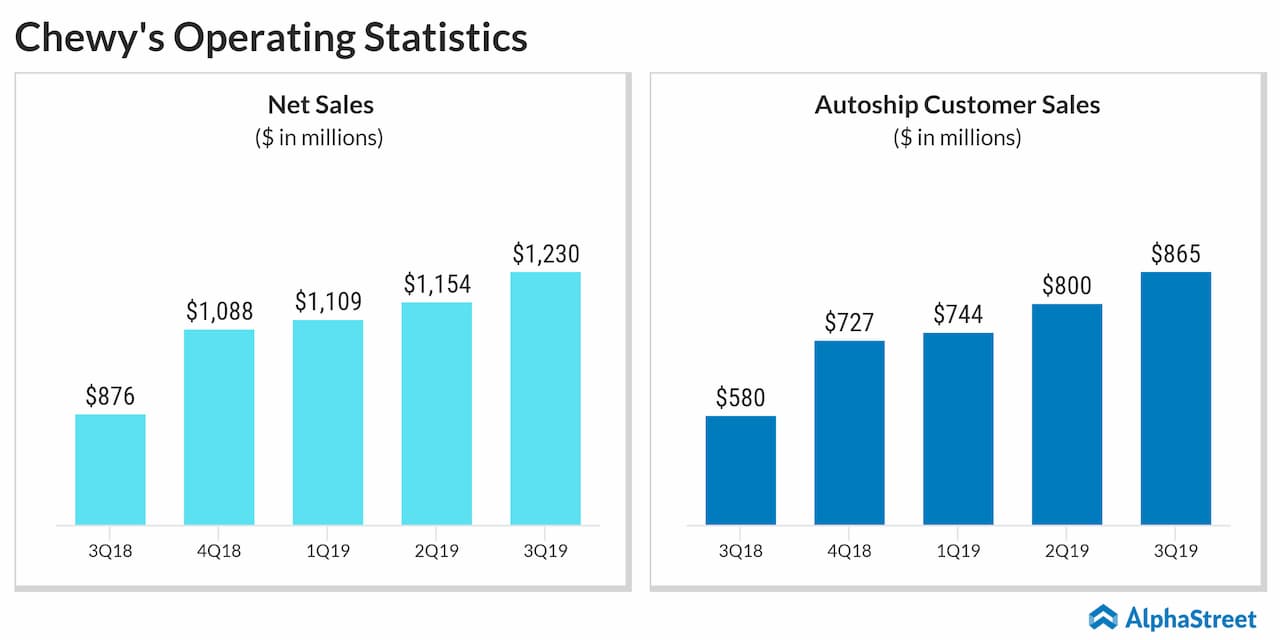

Net sales jumped by 40% to $1.23 million. The consensus estimates sales of $1.2 billion for the quarter. The company continued to see growth in the customer base as well as increased spending among its customers.

The results demonstrated continued top-line growth at scale emphasizing strength in the underlying business. The sales and margins were benefited by the recent investments in both private brands and Chewy Pharmacy, which remained the two pillars of its growth and margin strategy.

Looking ahead into the fourth quarter, Chewy expects net sales to grow 22-24% year-over-year to a range of $1.33-1.35 billion. This is much better than the consensus estimates of $1.33 billion. Excluding the 14th week in Q4 of 2018, sales growth is predicted to be 32-34%.

For the full year 2019, the company lifted its net sales growth outlook to about 37% from the previous estimates of 35-36%. The net sales forecast is raised to the range of $4.82-4.84 billion from the previous range of $4.75-4.80 billion. Excluding the 53rd week in FY18, sales growth is now expected to be 40%. The consensus estimates sales of $4.80 billion.

For the third quarter, active customers rose 33% year-over-year to 12.72 million while net sales per active customer improved 11.4% to $360. Autoship customer sales grew 49% to $865.2 million, driven by growth in the Autoship customer base. Autoship customer sales, as a percentage of net sales, was 70.4% compared to 66.2% last year.

Gross margin grew 410 basis points to 23.7%, driven by its disciplined execution to improve product margin and supply chain efficiency gains across all business verticals. This includes margin improvements in pharmacy and private brands.

Adjusted EBITDA loss was $30.2 million, an improvement of $38.4 million versus the prior-year quarter. This demonstrated the company’s ability to buy and retain customers, increase its share of wallet from those customers through catalog and category expansion while scaling its operating expenses.