While the pandemic-driven shopping spree continues to boost retail sales, there is also apprehension that the momentum might wane once normalcy returns to the market. The earnings report released by discount store chain Dollar General (NYSE: DG) last week signaled the possibility of a slowdown, but the management’s bullish outlook indicates the current momentum will be mostly sustained.

Related: Dollar General Corporation Q3 2020 Earnings Transcript

That is good news for long-term investors who would prefer to shrug off the decline in the company’s market value after the earnings announcement and focus on the long-term prospects. The stock dropped slightly and underperformed the market since then, joining industry-leaders like Walmart (WMT) that witnessed a brief sell-off.

Buying Opportunity

The dip in valuation offers an opportunity for those looking to invest in Dollar General, as experts predict a rebound in the coming months. Most of the analysts following the stock recommend buying it. On the flip side, the stock has not been very popular among hedge funds in recent times, but that is just one of the many criteria for assessing stocks.

Given the continuing macroeconomic uncertainty, marked by weakness in the labor market and people’s purchasing power, the holiday season is going to be a test of Dollar General’s resilience. The positive reports on the COVID vaccine have given rise to concerns that the current uptrend is temporary. But, the optimists are of the view that customers have gotten used to their new shopping habit and the conveniences that offer. So, it is likely that the transformation is irreversible and retailers who adapt to the changing customer taste would stay on the high-growth path going forward.

Store Expansion

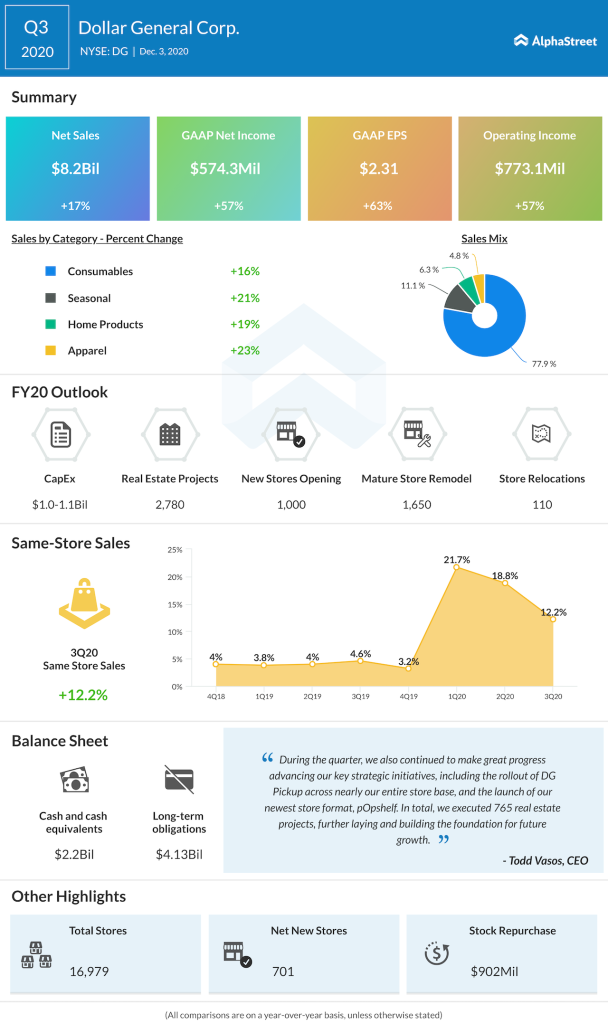

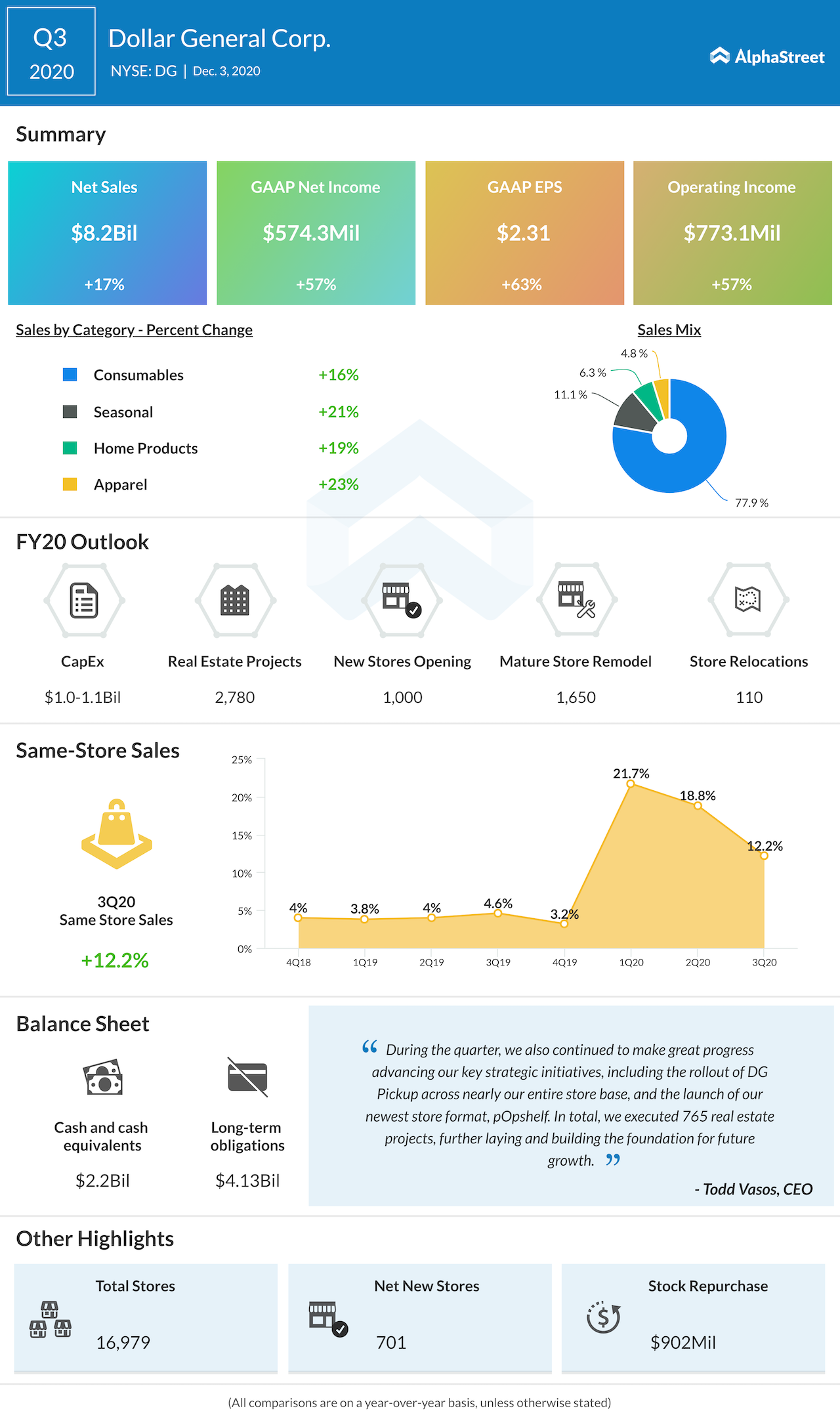

Meanwhile, the market was more impressed by Dollar General’s ambitious growth plans than its earnings performance, since the projection gives an insight into the prospects of the broad sector. The company is looking to add more than 1,000 new units to its store network next year, raising the total number of stores to about 18,000 while also remodeling as many as 1,750 outlets.

That will be complemented by the improved assortment and initiatives like DG Fresh for self-distribution of food. The increased focus on the food category shows the company wants to give tough competition to some of the leading food retailers. But benefits from the drop in promotional costs during the pandemic and other cost-savings might not be there in the post-COVID era, resulting in lower margins.

Comps Surge

Continuing the recent trend, comparable-store sales grew in double-digits in the third quarter, but at a slower pace than in the previous two quarters. Total sales climbed 17% to $8.2 billion, led by the core Consumables category. The momentum was widespread across all business segments, supported by the expanded e-commerce capabilities and pickup facilities introduced in view of the virus-related safety concerns. As a result, earnings moved up 17% annually to $8.2 billion during the three-month period.

Competitive Edge

The company continues to outperform fellow store operator Dollar Tree (DLTR), in terms of stock price and financial performance. While Dollar Tree lags behind its bigger rival in comparable sales and revenue generation, it has embarked on a drive to expand the store network after reporting impressive earnings last month. The stock has been trading higher, after getting a big boost from the strong earnings, and is probably poised to catch up with Dollar General.

The recent performance of Dollar General’s stock shows the stronger-than-expected third-quarter results did not impress the market. The shares pared most of their recent gains soon after the earnings report and maintained the downtrend since then. The stock, which climbed to an all-time high of $213.43 in mid-October, gained 28% in 2020.