Shares of Dollar General Corporation (NYSE: DG) were up over 2% on Friday, a day after the company delivered mixed results for the third quarter of 2022 and lowered its outlook for the full year. The discount store has been plagued by supply chain issues that are expected to continue in the upcoming quarter as well. Here are five points worth noting from the Q3 earnings report:

Mixed results

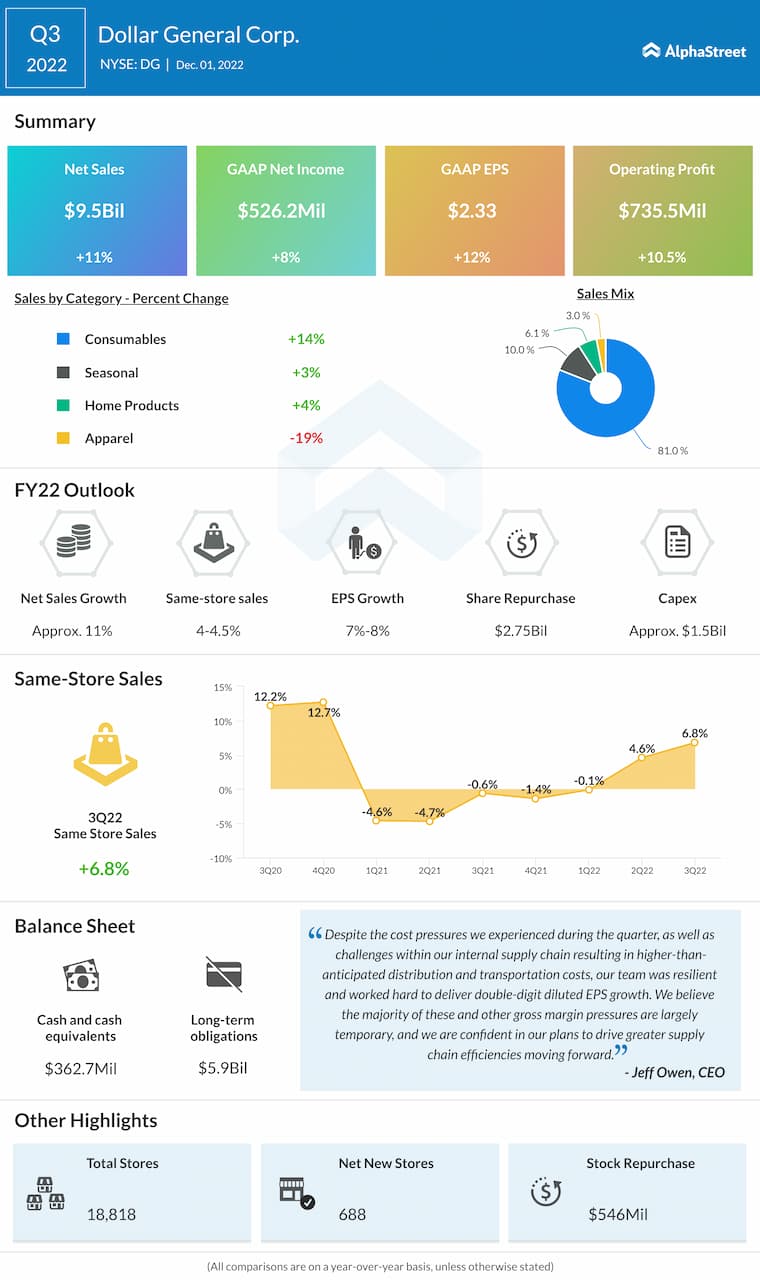

Dollar General’s net sales increased 11.1% to $9.5 billion in the third quarter of 2022 compared to the same period a year ago. The top line beat expectations and its growth was fueled by an increase in same-store sales and positive sales contributions from new stores. The company delivered EPS of $2.33, which rose 12% year-over-year but fell short of estimates.

Value during inflation

DG’s customers are feeling the pressures of inflation, reflected by reductions in the number of items purchased per basket and softer discretionary spending. In this environment, they are looking for more affordable options such as dollar price point items and private brands.

This indicates that during challenging financial times, customers are turning to discount stores like DG for more value. In Q3, Dollar General saw strong comp sales for its $1-price point products. Overall same-store sales in Q3 increased 6.8% driven by increases in average transaction amount and customer traffic.

Supply chain issues

Dollar General has designed permanent warehouse capacity solutions to support its changing distribution needs. Since these are yet to be fully functional, the company has been using temporary storage facilities. However, during the third quarter, it faced unexpected delays in opening additional storage facilities. This, along with the early arrival of seasonal goods, caused supply chain constraints which led to the company incurring additional costs of over $40 million, which in turn pressured gross margins.

However, in the past few weeks, Dollar General has managed to open extra storage and warehouse facilities along with two new permanent regional distribution hubs. These facilities are expected to alleviate some of the capacity pressures and improve the flow of goods.

Store fleet plans

Dollar General plans to open 1,025 new stores, remodel 1,795 stores and relocate 125 stores for fiscal year 2022. At the end of the third quarter, its non-consumable initiative (NCI) was available in over 16,000 stores. The company remains on track to roll out NCI across nearly its entire chain by the end of the year.

DG also opened 23 new pOpshelf locations in Q3, bringing the total number of stores to 103. It remains on track to nearly triple the pOpshelf store count this year, bringing the total to nearly 150 locations by year-end.

Lowered outlook

Dollar General lowered its earnings outlook for the full year of 2022. The company now expects EPS growth of 7-8% compared to its previous outlook of 12-14%. DG is seeing its sales mix tilt more towards lower-margin consumables due to inflationary pressures and this trend is expected to continue into the fourth quarter of 2022.

The company also expects some of the cost pressures related to its storage capacity constraints to continue into Q4. These factors are expected to have a greater impact on gross margin than previously anticipated which led to the revision of the earnings guidance. Dollar General still expects net sales to grow around 11% in FY2022.