Tiffany & Co. (NYSE: TIF) is scheduled to report first quarter 2019 earnings results on Tuesday, June 4, before market open. Revenue is expected to dip down by 1.3% to $1.02 billion while earnings is estimated to decline over 11% to $1.01 per share. Looking at the past four quarters, Tiffany has topped earnings forecasts three times.

Tiffany is likely to face pressures on its top line during

the first half of 2019 from weak demand among local customers as well as

negative impacts on tourist spending due to strength in the US dollar. The

threat from tariffs due to the ongoing US-China trade war also looms over the

company.

Tiffany has been investing significantly in business growth initiatives

which could help improve revenues going forward but in the meantime, the higher

expenses could weigh on earnings.

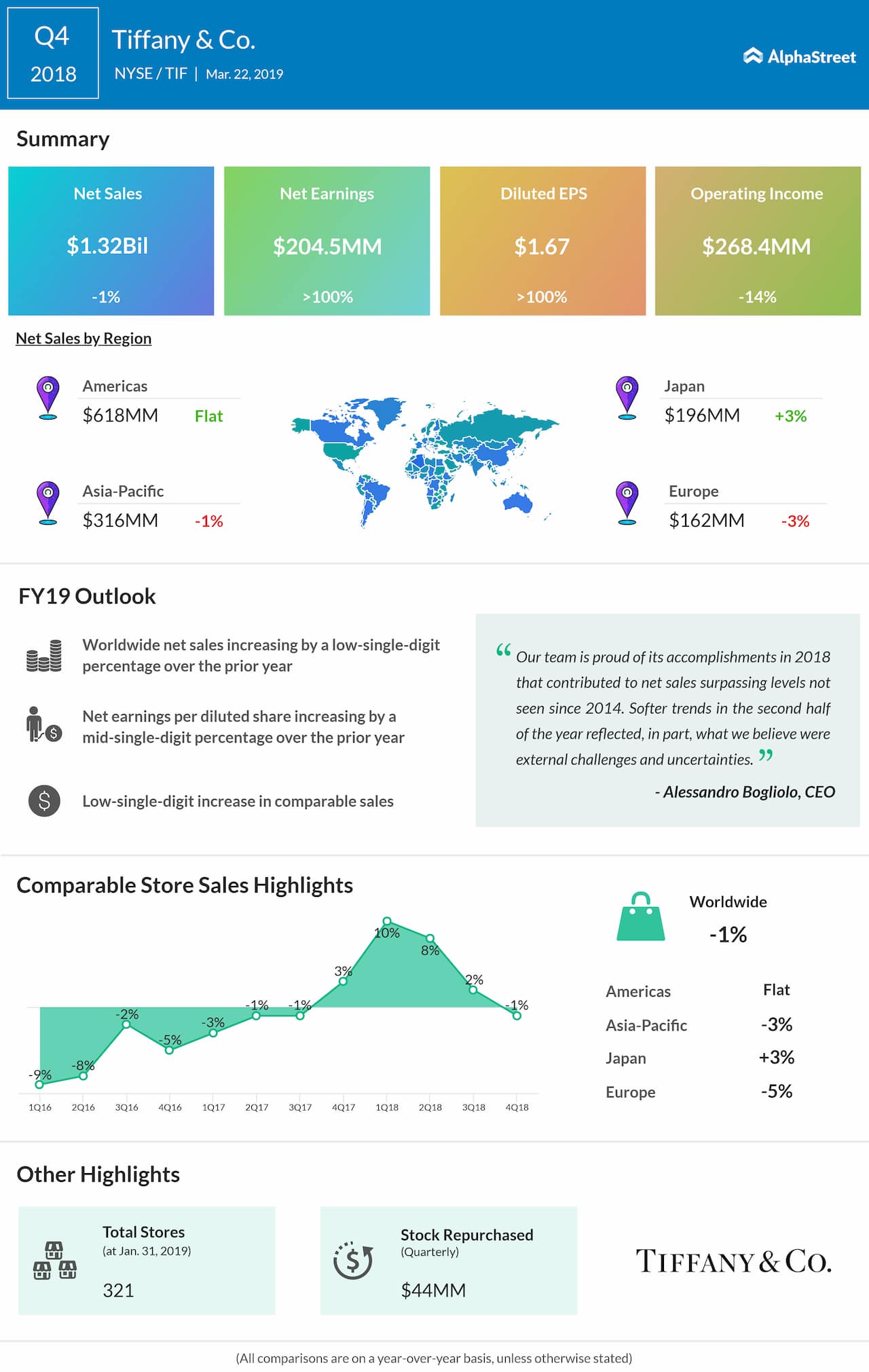

For the fourth quarter of 2018, Tiffany beat earnings expectations but missed the mark on revenues. Both net sales and comparable sales dropped 1% due to lacklustre holiday results. Earnings jumped to $1.67 per share from $0.50 per share in the prior-year period helped by a lower tax rate.

For fiscal year 2019, Tiffany expects worldwide net sales to

rise by a low-single-digit percentage over the prior year, while EPS is

expected to increase by a mid-single-digit percentage. The company also expects

a low-single-digit rise in full-year comparable sales, with eight store

openings, six closings and 15 relocations.

According to a report by Research and Markets, global diamond jewelry sales in 2018 rose 4% to $85.9 billion from a year ago. Sales in North America made up more than 50% of the share of the total sales and were up 4% year-over-year. The report suggests that the diamond market has a large development space and is estimated to grow at a rate of 5-10% over the next five years.

Tiffany’s shares have gained 12% thus far this year but looking at the past three months, the stock has dropped 7%.