Workday, Inc. (NASDAQ: WDAY) has constantly strived to stay relevant in the rapidly evolving cloud market, often adapting to new trends quickly through innovation and strategic partnerships. While the COVID-related slump in the labor market weighs on near-term prospects of the company’s human capital management solutions, the thriving financial management segment and solid subscription backlog paint a bullish picture for the long term.

In general, the services offered by Workday can play a key role in making the transition to remote-working hassle-free. Recently, the California-based firm joined hands with tech majors Microsoft (MSFT) and Salesforce (CRM) to offer solutions for businesses to function effectively in the changed market scenario. The aggressive customer addition, which includes big names like Cisco (CSCO) and Airbus, complements the recent upgrade to a feature-rich new version of Workday.

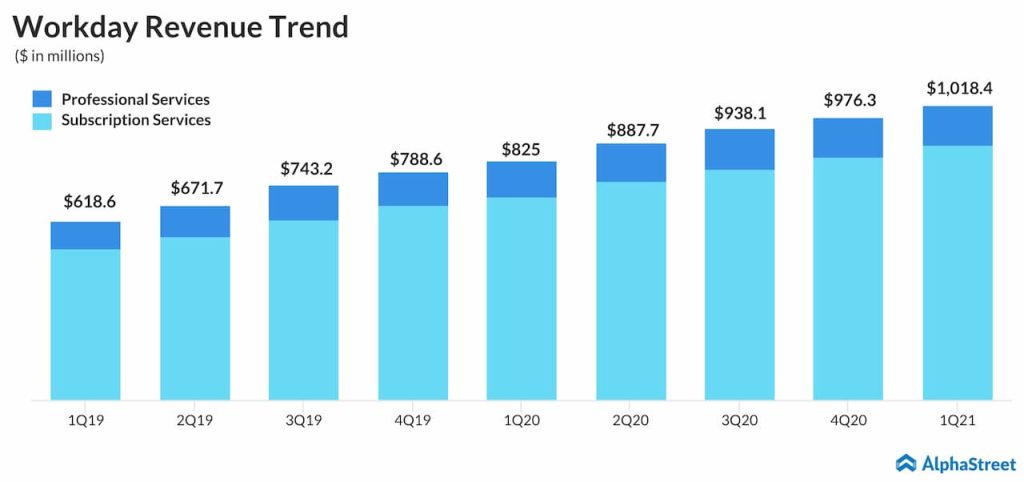

Positive Q1

In the first quarter, earnings edged up to $0.44 per share from $0.43 per share last year, though margins remained under pressure from high costs. Aided by a double-digit increase in subscription revenue, the top-line climbed to above $1 billion. The results also topped analysts’ estimate, which was trimmed in view of the adverse market conditions.

[irp posts=”62918″]

During his interaction with analysts at the earnings conference call, CEO Aneel Bhusri said, “Our focus remains centered on driving strong, durable growth, and we will continue to invest in our products and other areas of the business, to support our long-term growth aspirations. Based on our over-performance in Q1, but keeping in mind, we face a very difficult second half comps from last year, we are raising our fiscal 2020 outlook.”

Liquidity

As part of its capacity expansion program, the company continues to invest in the business, especially in real estate for expanding the data centers. Going forward, the heavy capital spending might weigh on cash flow. It needs to be noted that typically the company generates limited operating cash flow in the second quarter.

According to Workday executives, they adopt a flexible stance while dealing with customers who have been hit by the market turmoil. But if there are too many payment deferrals, it will put pressure on the balance sheet. The other possibilities are delays in contract renewals and requests for renegotiation of the financial terms.

Emerging Trend

Going by the latest trend, the uncertainty surrounding the pandemic-induced movement restrictions would encourage enterprises to shift from on-premise to cloud-based financial management systems. At the same time, Workday’s HCM solutions can be effectively used to help people who have been rendered jobless during the shutdown, by facilitating their re-employment. It assumes significance as the company has reaffirmed its commitment to help employees return to workplace safely.

“There is uncertainty in the short term in terms of what the uptick in terms of adoption of enterprise applications will be in the short term. But there is no question in the intermediate and longer terms that there will be tailwinds towards the adoption of cloud-based planning and cloud-based applications more generally.”

Tom Bogan, vice chairman of Workday

Meanwhile, the management might need to do a lot a brainstorming on the company’s pipeline, given the lack of visibility into the latter part of the current quarter and beyond, due to the emerging situation.

Buy WDAY?

Experts are divided in their outlook and nearly half of the analysts recommend buying the stock. Investors might find the relatively low valuation attractive, at a time when most tech stocks are making strong gains after the recent slump.

[irp posts=”50359″]

In early March, Workday’s shares dropped to the lowest level in nearly two years amid the widespread selloff spurred by coronavirus, but bounced back and gained steadily in the following weeks. On Thursday, the stock traded broadly at the levels seen at the beginning of the year. It has lost 10% in the past twelve months.