Cisco Systems Inc. (NASDAQ: CSCO) this week issued stronger-than-expected guidance for the current quarter, hoping an uptick in the demand for network equipment as the remote work culture gains ground across industries. The bullish outlook and the network-gear maker’s mixed third-quarter results give a sense of what awaits the tech industry in the near term.

Considering the changing environment, the management might need to see the company’s ongoing transition – to a provider of software and subscription-based services – from a different perspective. At the end of the quarter, about three-fourths of the software services were subscription-based, which is much higher compared to last year.

The Digital Shift

It is certain that a large number of enterprises will seek to upgrade their network infrastructure realizing its importance in the current situation, which is something Cisco can look to cash in on. Since the work-from-home concept is going to stay here in the foreseeable future, companies will ramp up their cloud capabilities and service providers would want to speed-up the deployment of 5G and Wi-Fi 6 – processes that require advanced network solutions like those offered by Cisco.

Growth Drivers

Also, the 8000 series router, which is in the trial stage at several locations currently, is expected to contribute to revenues once actual deployment starts after the evaluation period. The planned acquisition of wireless equipment company Fluidmesh Networks can be seen as a move aimed at empowering the infrastructure division to deal with future headwinds.

“We are going to continue to accelerate those technologies that help our customers use the cloud more effectively. We are going to — as our customers, some of our customers are going to need opex offers in the future given capex restraints. So we’re working on a balance of our portfolio to be delivered in both op capex models to give customers the flexibility that they need.”

Chuck Robbins, chief executive officer of Cisco

Need of Hour

The emerging scenario calls for increased focus on applications like WebEx and AppDynamics, which have the potential to attract customers during the shutdown period, though their contributions did not help the Applications segment much in the last quarter. The free-trial offers being extended to the crisis-stricken customers should help the services reach a wider market. With pricing pressure being a cause for worry, it needs to be seen how much will the cost-reduction initiatives help in sustaining margins.

[irp posts=”61431″]

On the flip side, payment deferrals by cash-starved clients will not bode well for Cisco’s liquidity this year, though its fundamentals and finances are strong enough to contain the impact to some extent. As of now, the goal is to pass on as much as 50% of free cash flow to shareholders annually, in the form of share buyback and dividend.

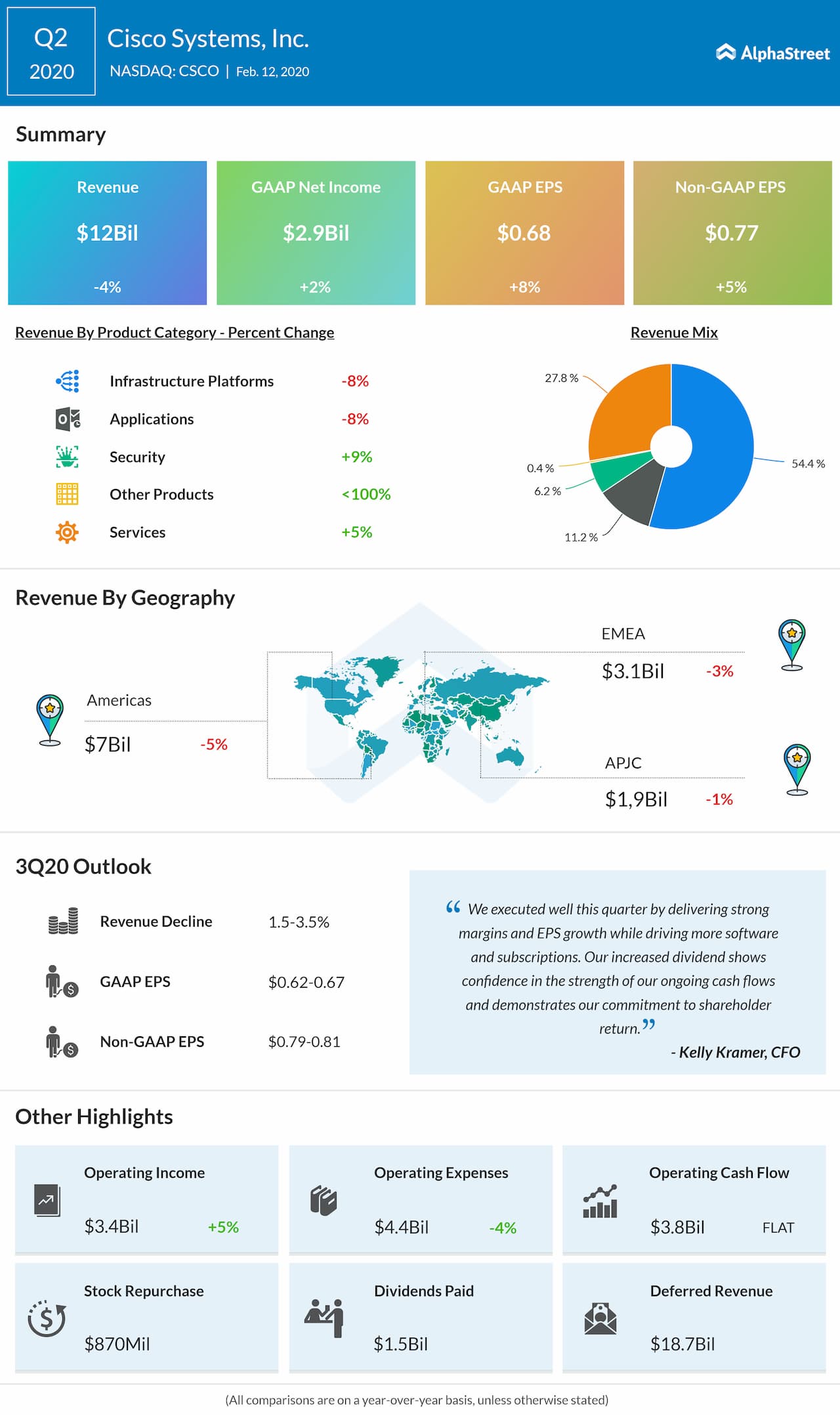

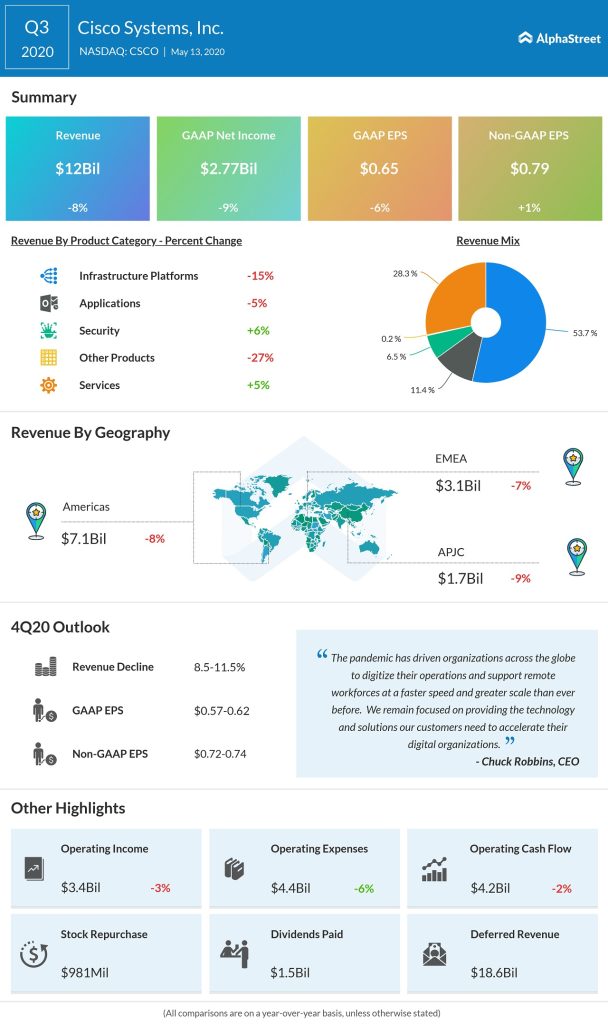

Q3 Revenue Dips

The main business segment, which involves production of routers and networking switches, might witness a slowdown due to supply chain disruptions and production issues in the coming months, after a dismal show in the third quarter. The double-digit fall in Infrastructure Platforms revenue weighed on the top-line and total revenues dropped 8% year-over-year to $12 billion during the quarter. Earnings, on an adjusted basis, moved up 1% to $0.79 per share and exceeded Wall Street’s prediction.

Looking Ahead

Despite the mixed outcome and widespread volatility in the market, the management issued fourth-quarter guidance above expectations. But, revenues are seen declining year-over-year. Among competitors, Juniper Networks (JNPR) last month reported weaker-than-expected earnings and revenues for its most recent quarter.

To an analyst’s question of whether parallels could be drawn between the 2000s recession and the Covid crisis, Robbins replied, “Well, I don’t think you can compare it to the bubble because we were at the epicenter of that one. So that one felt a lot different. In this one, we’re secondary collateral damage I would say, but I think the difference here is the broad-based challenges that this thing has presented to customers around the world, but we all know that the response from the Fed, the response from Congress on.”

[irp posts=”61193″]

After hitting a multi-year high, Cisco’s shares pulled back early last year and continued the downtrend since then. They dropped further during the recent tech selloff and the pandemic-strike. However, the stock is slowly getting back on track and made strong gains this week following the earnings announcement.