Shares of Delta Air Lines Inc. (NYSE: DAL) stayed green on Monday. The stock has gained 42% year-to-date and 35% over the past three months. Last week the company delivered strong results for the second quarter of 2023 and raised its guidance for the full year. Here’s a look at a couple of factors that work in the airline’s favor:

Strong quarterly performance

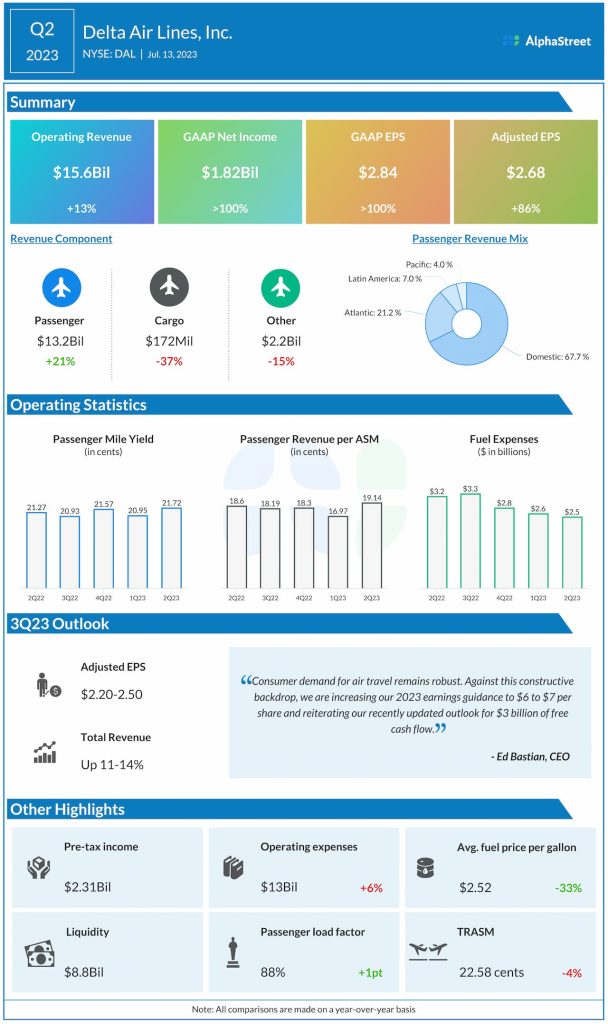

Delta generated operating revenue of $15.6 billion in the second quarter of 2023, up 13% from the same period a year ago. Adjusted operating revenue increased 19% year-over-year. On a GAAP basis, net income more than doubled to $1.82 billion, or $2.84 per share. Adjusted EPS rose 86% to $2.68. The top and bottom line numbers also surpassed market expectations.

Robust travel demand

As stated on its quarterly conference call, Delta continues to see strong demand for air travel. Domestic and international travel remain healthy with domestic passenger revenue growing by 8% and international passenger revenue increasing by 61% in the second quarter compared to last year.

The company continues to see favorable trends in leisure and business travel, mainly led by international. Corporate travel is expected to improve in the second half of the year. Delta stated that, as per its corporate surveys, 93% of companies expect their travel to increase or stay the same sequentially in the third quarter of 2023.

In addition, consumers are in good shape financially, with particular strength in the premium consumer base. Consumers are willing to spend on travel rather than spending on goods, which is a favorable trend for Delta.

Revenue diversification

Premium and Loyalty revenue continue to drive revenue diversification. Premium revenue increased 25% YoY in Q2. Loyalty revenue grew 20%, driven by co-brand acquisitions and growth in spend. American Express remuneration increased 22% YoY to $1.7 billion.

Upbeat outlook

Delta raised its outlook for the full year of 2023 based on its strong performance in the first half of the year. The company now expects total revenue to grow 17-20% YoY and EPS to range between $6-7. Operating margin is expected to be greater than 12%.

For the third quarter of 2023, total revenue is expected to increase 11-14% YoY. Capacity is expected to be up 16% while unit revenues are expected to be down 2-4%. Operating margin is expected to be in the mid-teens while EPS is estimated to range between $2.20-2.50. Non-fuel unit costs are expected to decline 1-3% YoY. Fuel price is expected to range between $2.50-2.70 per gallon.