Action camera manufacturer GoPro ( NASDAQ: GPRO) reported its first quarter 2020 results on May 7, which were in line with the preliminary results announced by the company on April 14. The company announced its restructuring plan, which included reducing operating costs and optimizing its business model to address the impact of the COVID-19 pandemic. The company had already suspended its outlook for fiscal 2020 and Q1. For the struggling GoPro, which reported losses in the last three years, the chance of returning to profitability looks impossible even in 2021.

Q1 results

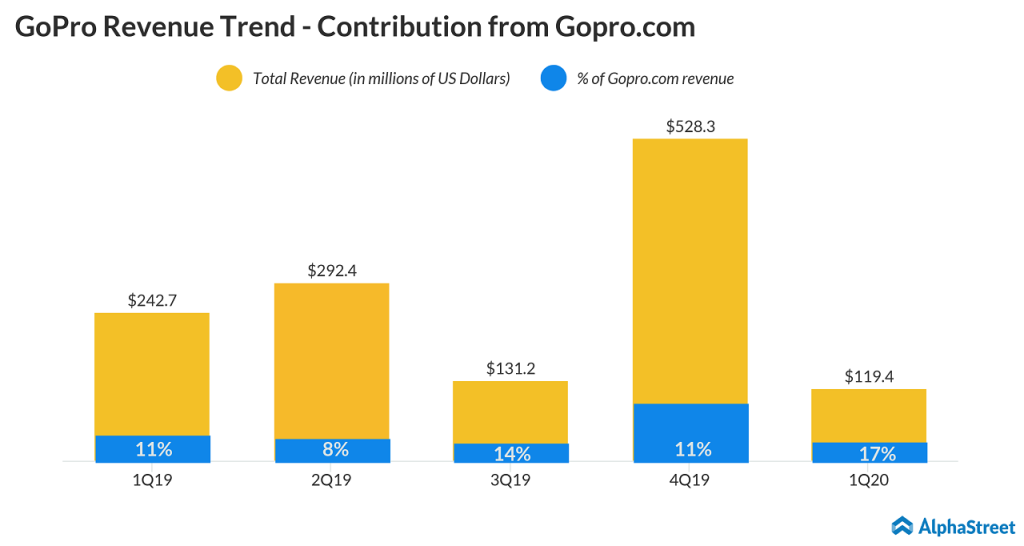

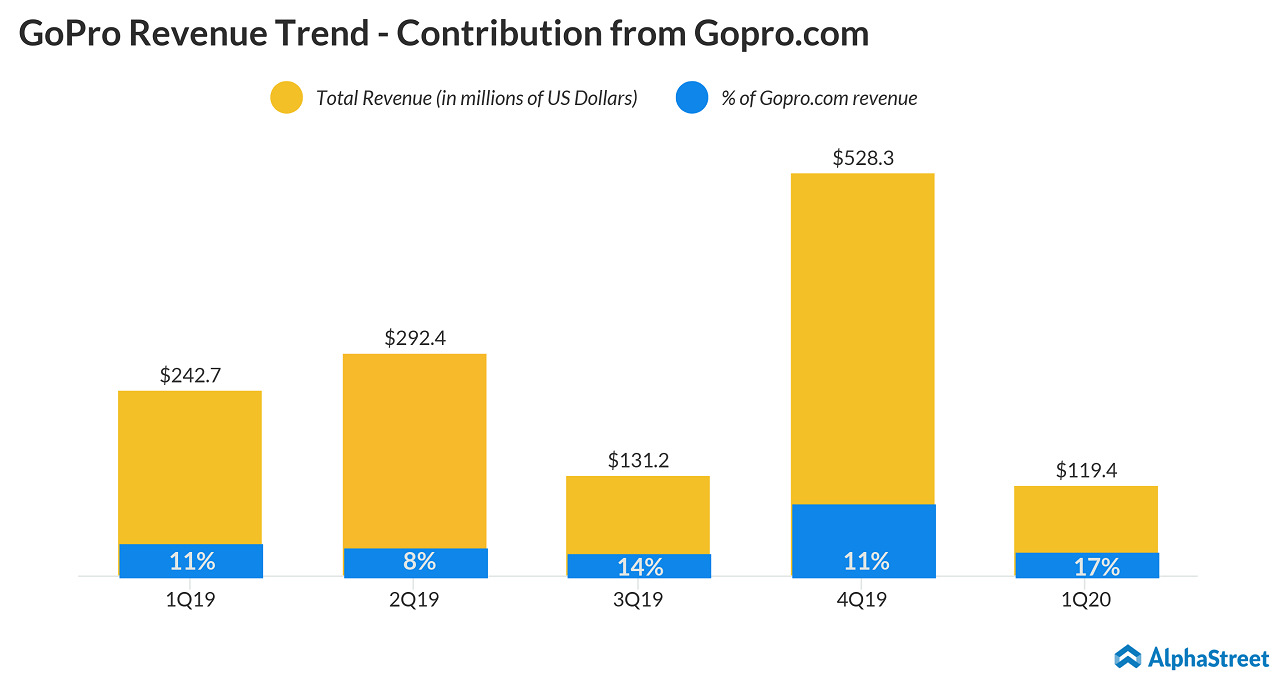

On an adjusted basis, GoPro’s loss in the first quarter expanded to $0.34 per share from a loss of 7 cents per share in the prior-year quarter. Revenue more than halved to $119 million with America and Asia and Pacific experiencing nearly 50% decline, while revenue from EMEA plunged 57%. Revenue was unfavorably impacted by the COVID-19 pandemic and higher levels of inventory in sales channels at the end of the fourth quarter of 2019. Camera shipments decreased by 60% to 341,000.

Restructuring actions

The restructuring plan announced on April 14, 2020, included axing the company’s global workforce by more than 20% or 200 employees, shifting its business strategy by focusing more on direct-to-consumer sales through gopro.com and reducing sales and marketing expenses as well as leased facilities. GoPro, which had 923 employees at the end of March 31, 2020, expects to complete the workforce reduction by the second quarter of 2020. Revenue from gopro.com, which represented 17% of total revenue in the first quarter of 2020, is expected to grow to nearly 40% for the second quarter. However, GoPro will continue to sell its products through big-box retailers like Amazon, Best Buy and Target, mid-market retailers, specialty retailers, and distributors.

The San Mateo, California-based firm expects to cut down its operating expenses by $100 million to a range of $285 million to $290 million in 2020, and 2021 operating expenses are targeted to be about $250 million. The company anticipates that a substantial portion of these restructuring charges will be reflected in its second quarter results. It is worth noting that CEO Nicholas Woodman will forego the remainder of his salary through the end of 2020 and the Board of Directors also volunteered to forego their cash compensation for the same period.

Outlook

GoPro suspended its outlook for fiscal 2020 due to the uncertain macro environment related to the COVID-19. The company believes the cash, cash equivalents and marketable securities of $125 million as of March 31, 2020, will be sufficient to address its working capital needs, capital expenditures, outstanding commitments and other liquidity requirements for at least one year. GoPro sees the revenue mix from gopro.com to increase significantly over the 10% reported in 2019, to approximately 45% of revenue in 2020, and GoPro.com to represent the majority of revenue by 2021.

The company expects the shift towards higher-end cameras to continue in 2020. Cameras with retail prices above $300 represented nearly 90% of the company’s revenue in the first quarter, continuing a trend from 2018 and 2019 of consumers moving to higher-priced, and more profitable cameras. When an analyst questioned whether consumers will still continue to spend in excess of $300 for a GoPro product, CEO Nicholas Woodman said:

“As it relates to the economy and people’s purchasing power diminishing, that’s a very good question. I think that we would likely see people perhaps buying in fewer numbers, but still buying towards the high end.”

With regards to the sales in North American retail channels, the company’s flagship products will be sold primarily at gopro.com possibly with some sales at some key strategic retailers in Q4. GoPro will be primarily focusing on selling its mid and entry-level products with big-box retailers.

When asked whether there will be a certain loss of sales through the new business model, the CEO replied:

“No, I mean consumer interest and passions don’t necessarily go away. They might get put on hold for a little while as you say. And people have different priorities during a pandemic.”