Shares of Hasbro, Inc. (NASDAQ: HAS) fell over 5% on Wednesday. The stock has gained 23% year-to-date. The toymaker saw revenues decline double-digits in the third quarter of 2024 while profits grew compared to the previous year. Despite weakness in the top line, the structural and strategic changes the company has been making have benefited the bottom line, and Hasbro appears to be banking on this strategy for growth in the medium term.

Strategy shift

As mentioned on its quarterly conference call, Hasbro has been strategically shifting its mix towards games, digital, and IP licensing, which it believes is the future of play. Games and licensing, its two most profitable categories, outperformed during the third quarter. The company benefited from strength across MAGIC: THE GATHERING and DUNGEONS & DRAGONS as well as gains in Monopoly Go! and MY LITTLE PONY.

In Q3, MAGIC: THE GATHERING recorded a 3% growth in revenue, helped by the releases of Bloomburrow and Duskmourn. It also benefited from strong growth in Arena. The acquisition of D&D Beyond continues to yield benefits.

In licensing, Monopoly Go! is generating approx. $10 million in licensing revenue per month. Hasbro continues to work with its partner Scopely to drive user acquisition and retention for this mobile game.

In Consumer Products, the company’s strategy to out-license brands in the toy space is paying off. As mentioned on the call, FURREAL FRIENDS and LITTLEST PET SHOP have seen strong Point of Sale (POS) growth. MY LITTLE PONY is gaining through successful international partnerships across multiple merchandise categories, music, and collectible cards. Hasbro is also rolling out new products in partnership with Lego.

Hasbro is combining its new products and in-store promotions to drive consumer demand, and it expects to see continued improvement in its toy business.

Q3 performance

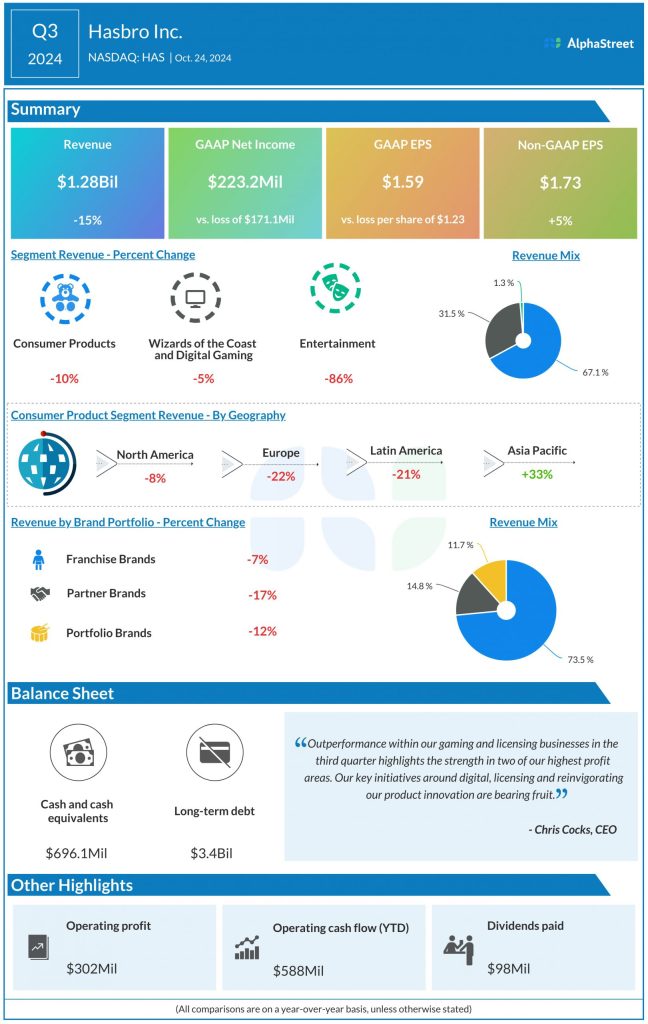

In Q3 2024, Hasbro’s total revenues decreased 15% year-over-year to $1.28 billion, with declines across all its segments. Adjusted earnings increased 5% to $1.73 per share. GAAP EPS was $1.59.

Revenues in the Consumer Products segment fell 10% while Wizards of the Coast and Digital Gaming saw revenues decrease 5%. Entertainment segment revenues were down 86% in the quarter.

Outlook

For the full year of 2024, Hasbro expects revenue for the Wizards segment to be flat to down 1%. Within licensed digital gaming, Monopoly Go! is expected to contribute around $105 million in revenue while Baldur’s Gate 3 is expected to contribute around $35 million for the full year. Consumer Products revenue is expected to be down 12-14% and Entertainment revenue is projected to be down approx. $15 million versus the prior year.