For businesses across the world, 2021 was a special year for many reasons — a period of great uncertainty due to the COVID crisis but at the same time, it saw a record number of companies making their stock market debut. The highly unpredictable market environment was probably the biggest challenge investors faced, a trend that is likely to persist in 2022.

Making the right investment decisions became cumbersome during the crisis period. But there are some great companies that successfully adapted to the new market environment, and Medtronic plc (NYSE: MDT) and Visa Inc. (NYSE: V) are among them. The companies managed to stay on the growth path and create value for shareholders, despite the adversities.

Medtronic

Medical device maker Medtronic is a rapidly growing healthcare company that follows a pure-play model, offering advanced products in the areas of cardiovascular, medical-surgical, neuroscience, and diabetes. 2021 was a busy year for the company in terms of new product launches.

The Minneapolis-based firm has a promising business strategy with focus on enhancing its product portfolio and diversifying to new segments. The solid balance sheet, supported by steady cash flows, is its main strength when it comes to achieving growth targets.

Though the business was affected by a dip in elective procedures in the early months of the pandemic, when healthcare facilities shifted their priority to COVID-19 care, demand bounced back after the restrictions were eased. More recently, the pipeline suffered a setback after regulators took a critical stance on Medtronic’s new insulin pump over quality control issues, putting the stock under pressure.

Johnson & Johnson reports Q3 2021 earnings

The stock contracted by a third after hitting a peak a few months ago and has become cheaper. The sell-off can be seen as an opportunity to invest since the factors that triggered the pullback are temporary. Experts’ analysis indicates that the stock is on its way to recoup recent losses and reach new highs in the coming months. In short, it is the right time to buy MDT, which is probably the most affordable pick in the segment.

In the second quarter, the company generated total revenues of $7.8 billion, which is up 3% from the prior-year levels. Adjusted earnings increased 29% annually to $1.32 per share. The company’s stock traded slightly higher in the early hours of Thursday, after closing the previous session lower.

Visa

Visa and its rival Mastercard In. (NYSE: MA) have been ruling the global payment services market for the past several years, with the former enjoying an edge in terms of market cap. The acceleration in the adoption of digital payment services during the pandemic sent the companies into overdrive even as they strived to innovate and fine-tune their strategies.

In an effort to make its network interoperable and enhance the digital-first experience, Visa launched what it calls the network-of-networks strategy. It will allow the company to act as a single point of connection for all kinds of transactions, be it on its own network or external. Such innovation, combined with the company’s broad range of products, should help it expand the addressable market.

While virus-induced restrictions on air travel and dining-out impacted Visa’s revenues initially, it was soon offset by strong growth in spending volumes in other categories like retail. However, the company’s growth prospects depend heavily on a full-fledged recovery of the aviation and restaurant industries.

For Visa’s shares, it has been a roller-coaster ride since the early weeks of the COVID-19 outbreak, but they maintained a steady uptrend and reached an all-time high in mid-2021. Interestingly, its quarterly numbers mostly exceeded analysts’ expectations during the crisis period, reflecting the underlying strength of the business and healthy balance sheet.

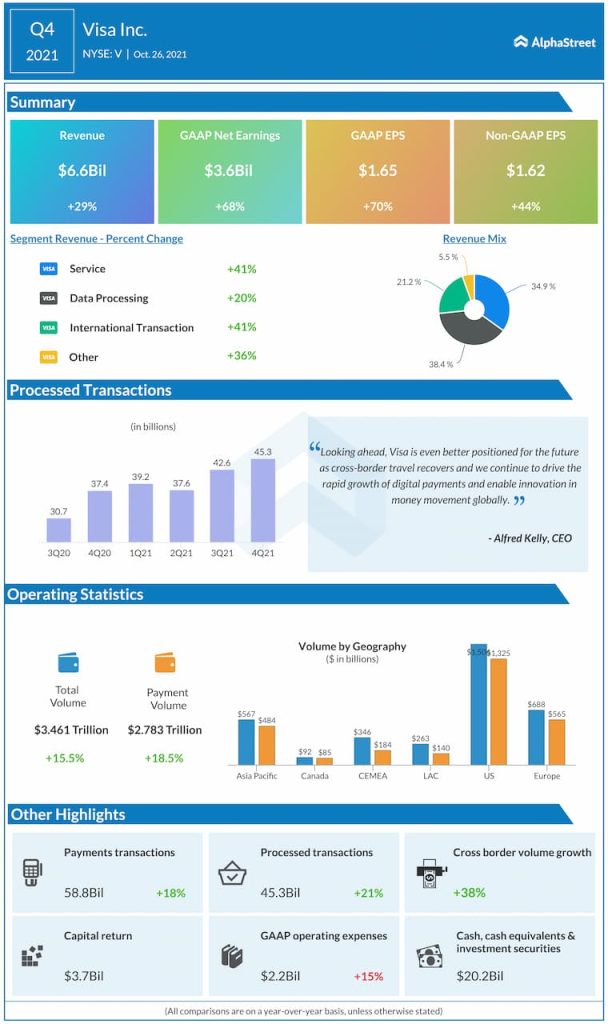

Later, the stock withdrew to the pre-peak levels but returned to growth mode last month after the company’s positive fourth-quarter report. Earnings grew in double digits to $1.62 per share in the final three months of fiscal 2021 on revenues of $6.6 billion, which is up 29% year-over-year. In an unusually bullish outlook, market watchers unanimously recommend buying the stock, which is expected to gain about 25% in the next twelve months.

American Express Company Q3 2021 Earnings Call Transcript

To put it simply, Visa has what it takes to tide over the short-term challenges, thanks to its ever-expanding network and growing market share. Moreover, the ongoing shift to digital payment is an irreversible trend that bodes well for the company in the long term. As the year comes to an end, the stock has become less expensive — currently trading about 12% below the recent peak. It is a buying opportunity that is worth considering.