Nike, Inc. (NYSE: NKE) has long been an investors’ favorite, due to the decent returns and dividend it offers, despite the relatively high stock price. Though the sneaker maker enjoys solid customer loyalty, there is concern that competition and margin pressures might weigh on its performance.

The general outlook on the company is bullish and analysts have assigned the stock buy rating. At $113, the current price target represents a 9% upside. With Nike’s long-term CEO Mark Parker stepping down this month, the market will be closely watching how things are shaping up under the new CEO and eBay (EBAY) veteran John Donahoe.

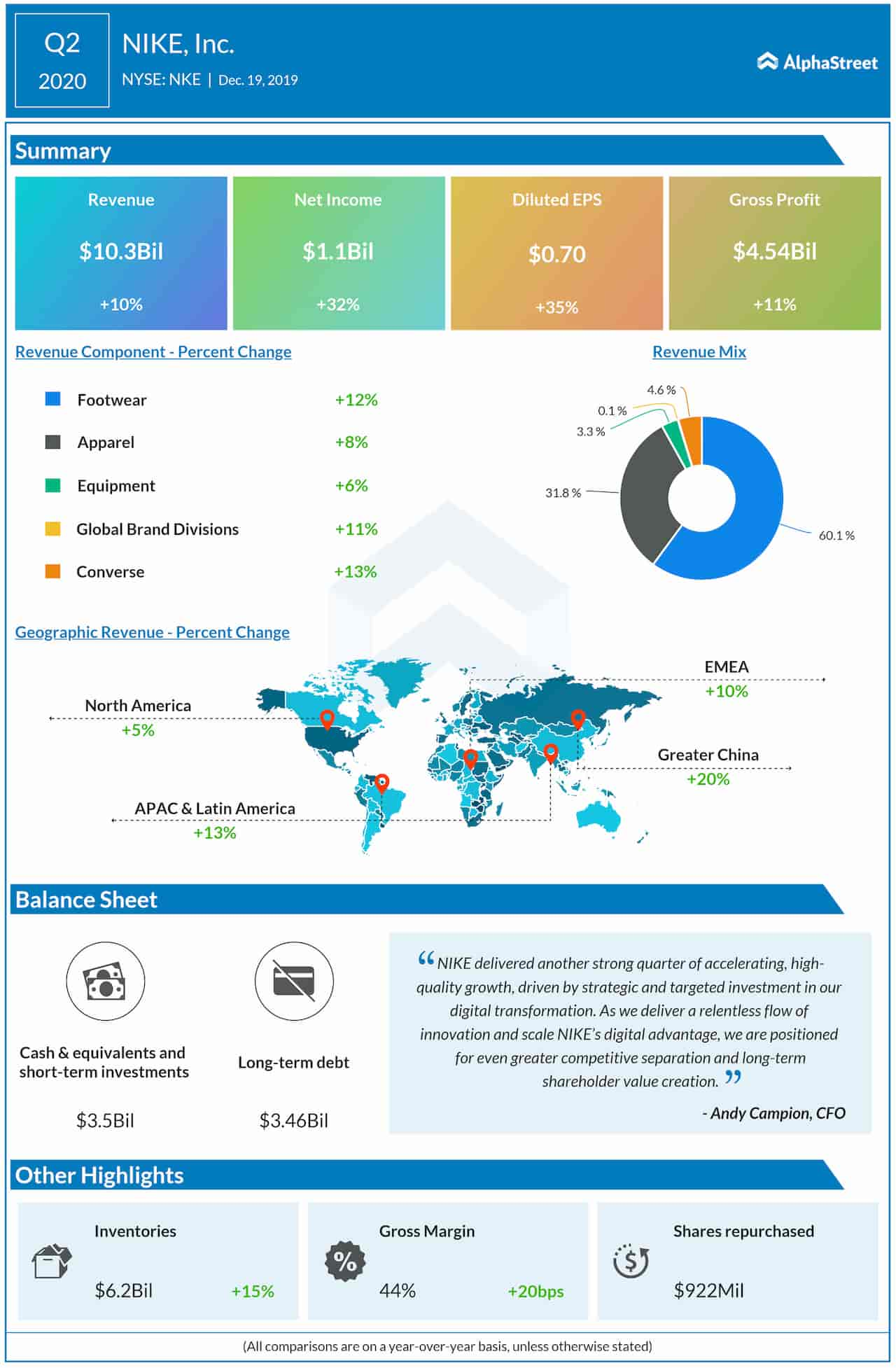

Also read: Nike’s stock stays in red territory despite strong quarter

Had the trade-related uncertainties eased, Nike would have been able to maintain the growth momentum during the remainder of the year. While the management’s initiative to reduce exposure in the Chinese market is a welcome step, it might not be sufficient if the standoff worsens.

Growth Drivers

On the positive side, the demand for sportswear is estimated to remain high in the foreseeable future and the Nike brand is prepared to tap the new opportunities. The firm bets on the strength of its digital platform, which continues to witness innovation. Adding to the company’s top-line prospects, a number of important sports events including the NBA regular season are scheduled this year.

New Peak

After setting new records consistently, shares of the sports goods powerhouse crossed the $100-mark towards the end of last year. At the current price, some investors might find the stock expensive. While maintaining stable profit growth, the main challenge facing the company is margin pressure. It reported double-digit earnings and revenue growth for the second quarter, which also exceeded the market’s expectations. However, the margin performance was not up to the mark.

Peer Performance

Among others, Skechers (SKX) seems to have emerged from a period of volatility. The stock’s value nearly doubled in the past twelve months and is currently hovering near its peak. In the third quarter, sales grew in double-digits aided by positive comparable store performance, as expected. Consequently, earnings rose and edged past the forecast.

Under Armour (UAA) had a rather dismal performance in 2019, with the stock retreating from a multi-year high a few months ago. Recently, the management trimmed its full-year guidance to reflect the weakness in sales.