Shares of DocuSign Inc. (NASDAQ: DOCU) were up 9% on Friday, a day after the company delivered better-than-expected results for its second quarter of 2023. Both revenue and earnings surpassed estimates and the company provided an upbeat guidance. Here’s a look at DocuSign’s plans for the near term:

Revenue

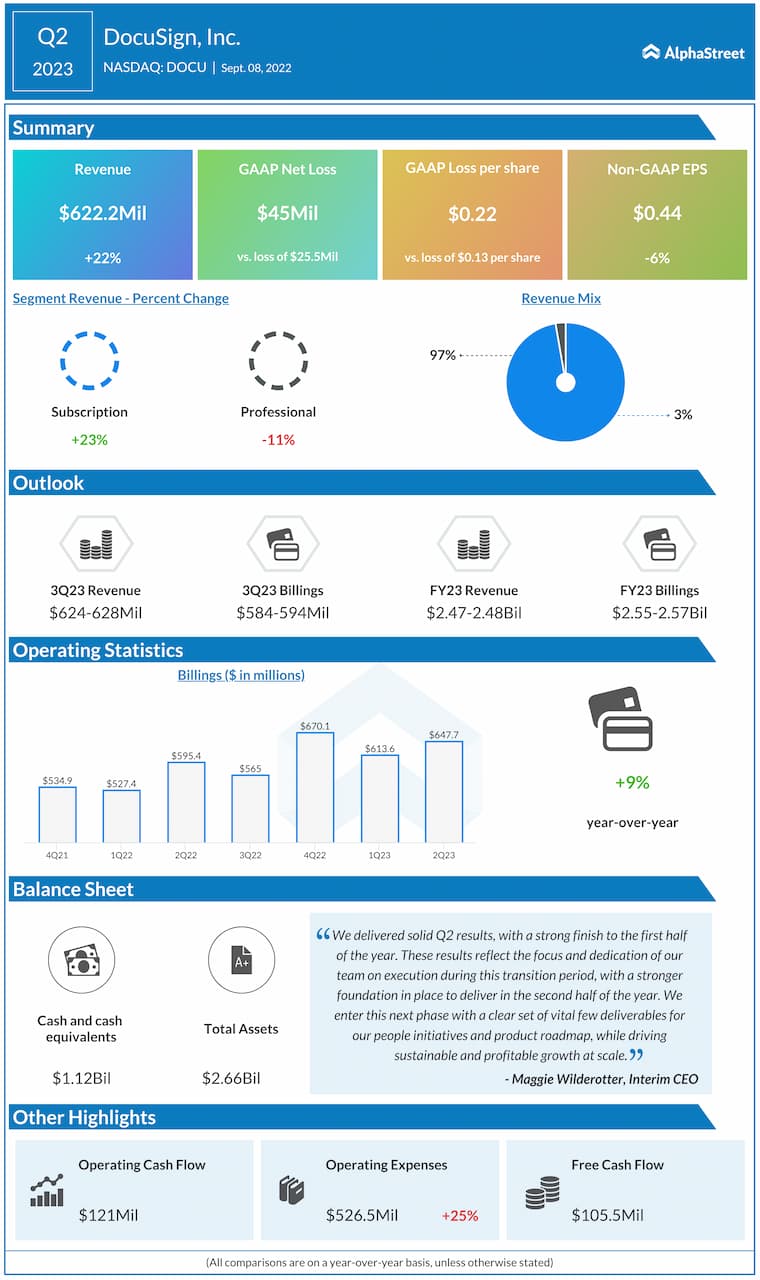

DocuSign generated revenues of $622.2 million in the second quarter of 2023, which was up 22% year-over-year. Subscription revenue rose 23% to $605.2 million while Professional services and other revenue fell 11% to $17 million. The company’s international revenue increased 35% YoY to reach $154 million and made up 25% of total revenue.

For the third quarter of 2023, DocuSign expects total revenue to grow 14-15% YoY to $624-628 million. Subscription revenue is expected to grow 15-16% YoY to $609-613 million. For the full year of 2023, total revenue is estimated to increase 17-18% to $2.47-2.48 billion and subscription revenue is projected to increase 18-19% to $2.40-2.41 billion.

Billings

In Q2 2023, DocuSign’s billings increased 9% to $648 million, with a four-quarter rolling average growth of 19%. The company saw strong customer growth during the quarter with around 44,000 new customer additions.

The total global installed base stood at 1.28 million customers at the end of Q2, up 22% YoY. This includes around 10,000 additional direct customers which leads to a total direct customer base of 191,000, which was up 29% YoY. During the quarter, customers with an annualized contract value greater than $300,000 increased 39% YoY to reach 992 in total.

For the third quarter of 2023, total billings are expected to range between $584-594 million. For the full year of 2023, billings are estimated to be $2.55-2.57 billion.

Profitability

DocuSign reported adjusted EPS of $0.44 in Q2 2023, which was down 6% YoY. Adjusted gross margin was 82%, in line with last year. Adjusted operating profit was $112 million compared to $100 million last year while adjusted operating margin dipped to 18% from 19% last year.

The company expects adjusted gross margin to range between 79-81% for both Q3 2023 and FY2023. Adjusted operating margin is expected to range between 16-18% for both the third quarter and full year of 2023.

DocuSign’s stock has dropped 58% year-to-date and 77% over the past 12 months.

Click here to access the full transcripts of the latest earnings conference calls