After a lackluster third quarter, KB Homes (NYSE: KBH) is set to end the fiscal year on a positive note as the housing sector continues to thrive on favorable market conditions and strong economy. The homebuilder is scheduled to report its fourth-quarter results on Thursday at 4:15 pm ET.

Also see: KB Home Q3 2019 Earnings Conference Call Transcript

Analysts are looking for earnings of $1.28 per share for the quarter, up 33% from last year. Revenues are seen rising 19.2% annually to $1.61 billion. A corresponding growth can be expected in financial services revenues in the to-be-reported quarter.

Strong Economy

The forecast reflects the positive trend in the housing market, aided by the current uptick in the economy. So, the chances of KB Home’s earnings once again beating the estimates are very high – as they did in the previous quarters. On the revenue front, it could be a trend-reversal this time, after missing the estimates in the previous three quarters.

The market’s bullish earnings outlook for the long term makes the stock attractive, which is moderately priced despite the recent rally. It shows the stock has room for further growth next year and beyond, which also justifies the consensus hold rating on it with a price target that represents a 7% upside.

Tailwinds

The Federal Reserve’s dovish stance has made mortgage loans more affordable. That, combined with the steady uptrend in the job market and people’s spending power, bodes well for the housing industry. Consumer confidence has been at a historic high, and new home-buyers are encouraged to take the plunge. However, the persistent supply constraints might have played spoilsport in the final months of the fiscal year, rendering the company unable to fulfill the demand.

As far as meeting the delivery targets is concerned, the solid order growth and high backlog levels might put the company under pressure. It needs to be seen to what extent the cost-cutting efforts would be effective in maintaining margin growth. The management is looking for double-digit margin growth both sequentially and on a year-over-year basis.

Looking Back

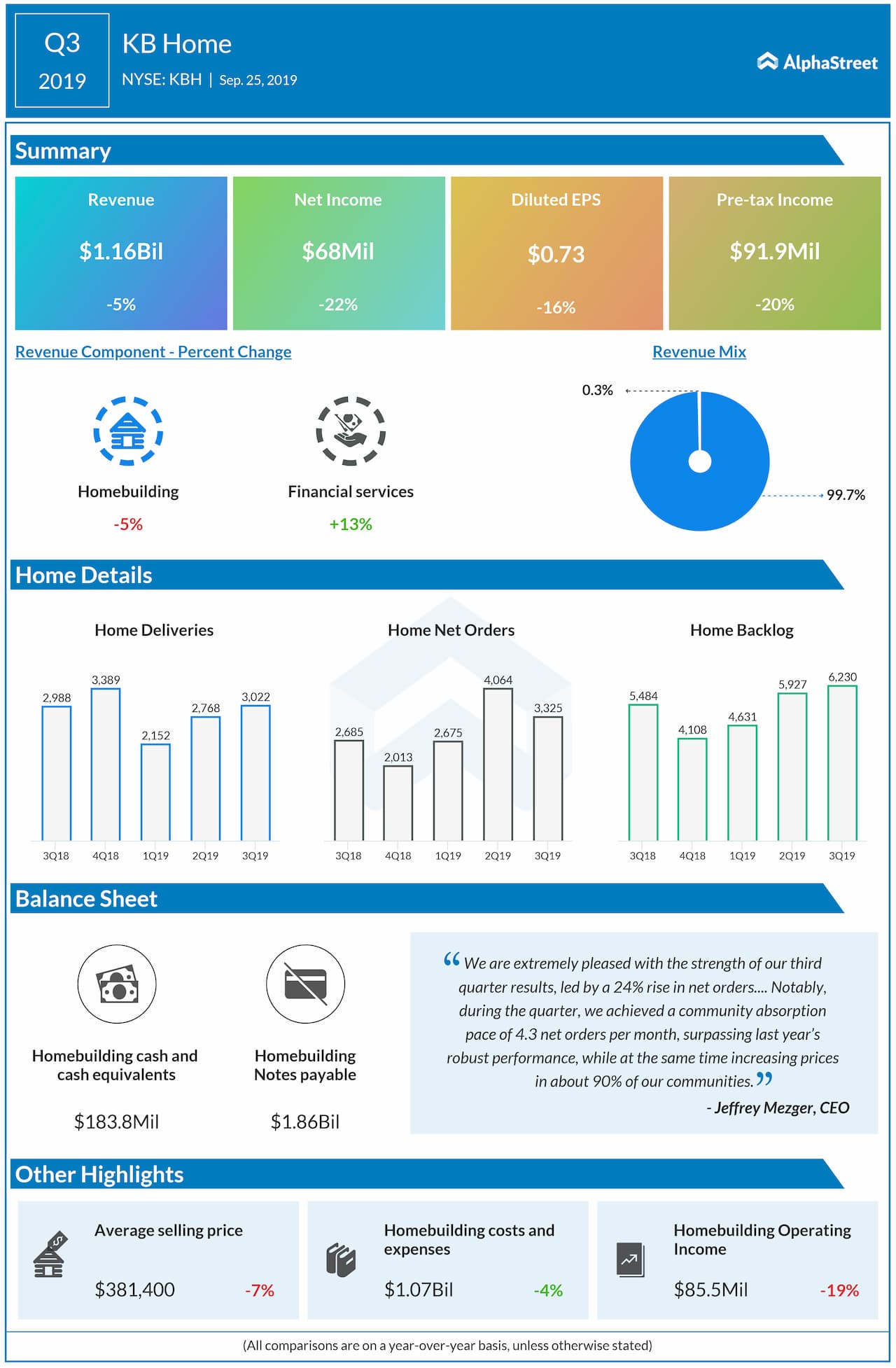

In the third quarter, earnings decreased 16% from last year to $0.73 per share on revenues of $1.16 billion, which represents a 5% year-over-year decline. While the bottom-line surpassed the estimates, sales missed.

Shares of KB Home climbed to a two-year high a few months ago but pared a part of the gains in the following weeks. The stock has gained 65% in the past twelve months, outperforming the market.