Shares of Pfizer Inc. (NYSE: PFE) gained over 5% on Wednesday following the company’s announcement of its first quarter 2024 earnings results. Although the top and bottom line numbers decreased from the prior year, they surpassed analysts’ projections. The pharma giant also raised its adjusted EPS guidance for the full year of 2024. Here are the key takeaways from the Q1 report:

Better-than-expected results

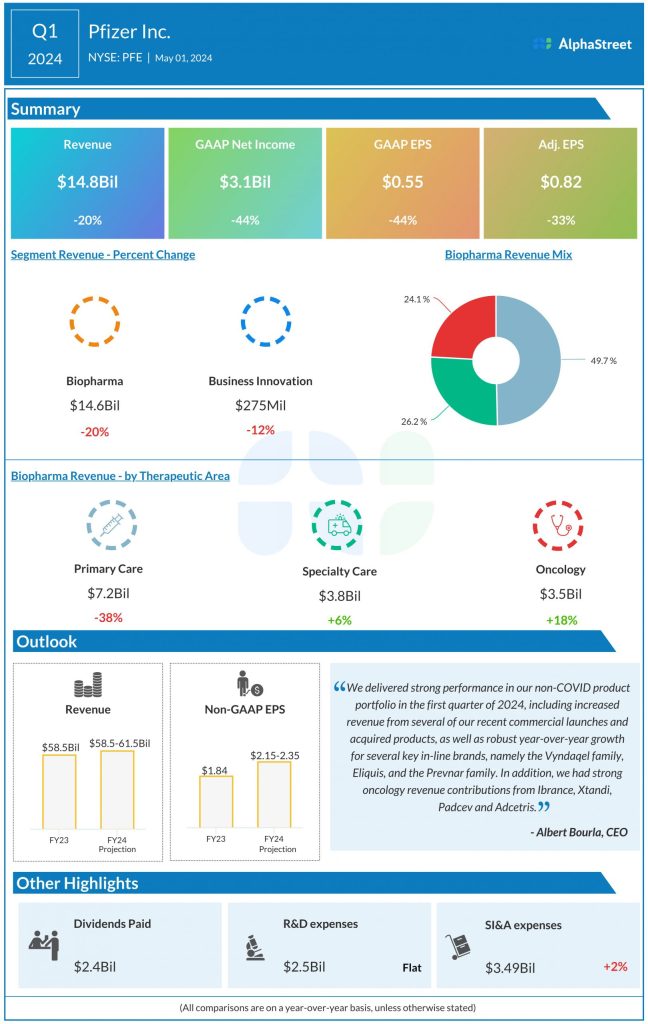

In Q1 2024, Pfizer’s net revenues decreased 20% year-over-year to $14.9 billion but came above expectations. On an operational basis, revenues declined 19%. The decrease in the top line was mainly due to a drop in global revenues of Comirnaty and Paxlovid. Excluding contributions from these two COVID products, revenues increased 11% operationally.

Reported net income decreased 44% to $3.1 billion, or $0.55 per share, compared to last year. Adjusted EPS fell 33% YoY to $0.82, but surpassed estimates.

Business performance

During Q1, Comirnaty revenues decreased 88% operationally to $354 million, mainly due to lower contractual deliveries and demand in international markets, as well as lower US volumes, reflecting the seasonality of demand for vaccinations and the transition to traditional commercial market sales in certain markets, including the US.

Paxlovid revenues declined 50% operationally to $2 billion, mainly due to lower contractual deliveries in the US and most international markets due to the transition to traditional commercial market sales, as well as lower demand in China.

During the quarter, Pfizer witnessed strength in its non-COVID product portfolio. It saw revenue growth for in-line brands such as the Vyndaqel family, Prevnar family, Eliquis, and Abrysvo. It also benefited from revenue contributions from legacy Seagen. This strength was partly offset by lower revenues for Sulperazon, Ibrance, and oncology biosimilars.

Updated outlook

Pfizer raised its adjusted EPS guidance for full year 2024 as it remains confident in achieving its cost realignment program target and in the strength of its business. The company now expects adjusted EPS of $2.15-2.35 versus its prior outlook of $2.05-2.25.

Its revenue guidance for the year remains unchanged at $58.5-61.5 billion. This includes anticipated revenues of approx. $5 billion for Comirnaty and $3 billion for Paxlovid, as well as around $3.1 billion from legacy Seagen. The company expects 90% of Comirnaty sales to occur in the back half of the year, mostly in the fourth quarter, given the seasonality of demand for COVID vaccinations.