The COVID-induced disruption has been a litmus test for most department stores and supermarket chains, and retailers that adapted quickly to the new trends tackled the crisis much better than others. In the case of The Kroger Co. (NYSE: KR), the main driving force behind its resilience is the successful business model.

For the Cincinnati-based company, which operates a multi-department store chain, retaining customer loyalty is a key priority, through promotional investments and initiatives like the fuel rewards program. The positive sentiment among stakeholders is evidenced by the solid performance of the company’s stock, which stayed largely unaffected by the market downturn and hit a peak a few months ago.

Stable Stock

Last week, the shares reached the $50-mark after a long gap and maintained the uptrend after the earnings announcement. Experts’ consensus target price points to modest gains in the remainder of the year. Given the relatively high valuation, it looks like the positive elements have already been factored into the price. In other words, KR seems to have peaked, leaving not much room for further growth.

Read management/analysts’ comments on quarterly reports

Those who have an eye on the stock should be looking for cues on its ability to create decent shareholder value in the near future. In that respect, it is better to hold buying/selling decisions at least until the next earnings. As far as long-term investment is concerned, meanwhile, the stock’s resilience to unfavorable market conditions is a positive factor. It is worth noting that KR has outperformed the S&P 500 by a big margin so far this year.

Gaining an Edge

Kroger’s efforts to expand its in-house portfolio and drive customers to the digital platform are paying off when it is most needed. It has helped the company compete effectively with big box retailers like Walmart Inc. (NYSE: WMT) which have been expanding their grocery footprint, lately. However, consumers’ weakening spending power amid inflationary pressures and supply chain bottlenecks remain a risk to the company’s future sales performance.

Target: A few factors to take into account if you are considering this major retailer

Kroger’s CEO Rodney McMullen said in a recent statement, “Customers continue to adjust their shopping habits in response to ongoing inflation. We are doing everything we can to help our customers stretch their dollars with high-quality fresh products at everyday low prices and industry-leading fuel rewards program and personalized savings on the items that matter most to them. Our customers are looking for ways to save, and we are there for them.”

Key Numbers

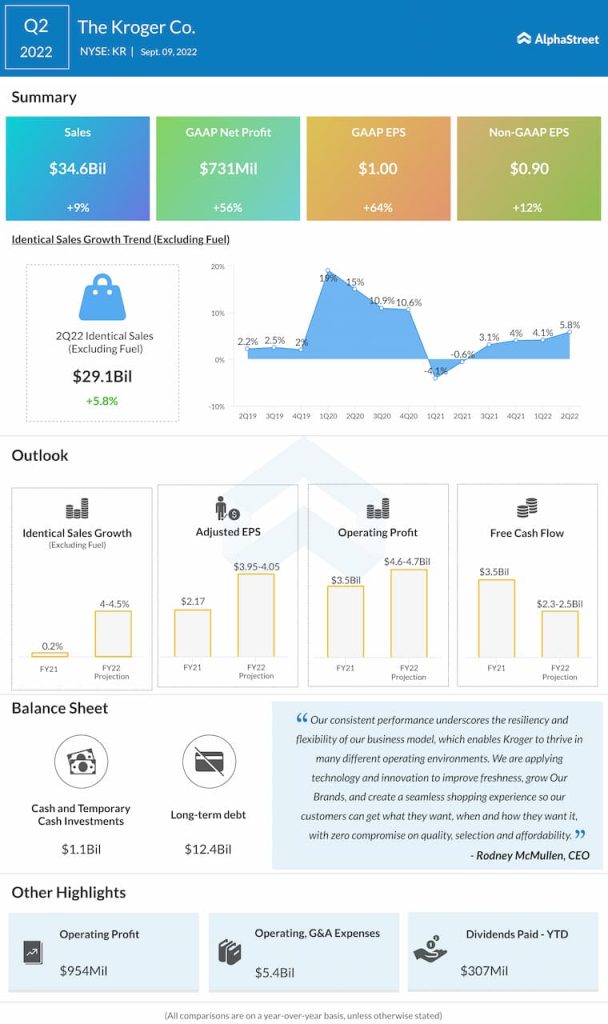

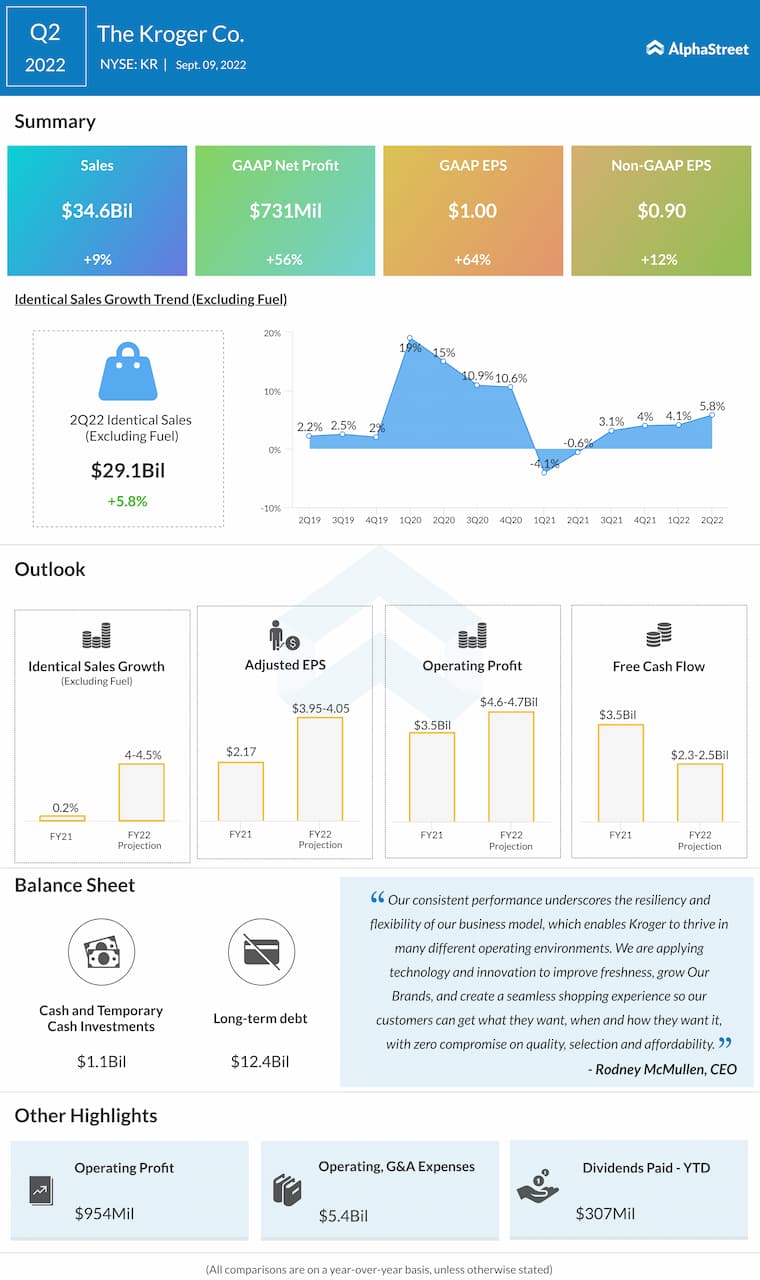

Kroger’s margin performance has been impressive in recent years, despite the challenging operating conditions, and earnings topped expectations in every quarter since 2020. After slipping into the negative territory more than a year ago, identical sales – excluding fuel as sales to customers — bounced back and recovered at a steady pace. In the second quarter, a 5.8% increase in identical sales translated into a 9% growth in net sales to $34.6 billion. Consequently, earnings moved up 12% to $0.90 per share.

After paring most of the earnings-driven gains, the stock traded lower in the early hours of Monday’s session. It has gained 7% in the past 30 days.