Shares of the Kroger Co. (NYSE: KR) have gained over 3% year-to-date. The company managed to grow sales and profits in its most recent quarter even as it continues to operate in a challenging environment. Amid high inflation and macroeconomic uncertainty, customers are prioritizing their spending on food and are looking for various ways to save money.

Kroger’s customers are making use of loyalty discounts as well as redeeming personalized digital coupons and fuel rewards. In the first quarter of 2023, the company saw sales made on promotion increase by around 380 basis points while digital coupon redemptions rose to 180 million.

Kroger saw growth in mainstream and higher-income households, with the latter building larger baskets and buying larger pack sizes thereby generating more profit. On the other hand, budget-conscious households are buying fewer items and opting for lower-priced products and smaller pack sizes, giving more importance to price than to other factors like quality, convenience or personalized offers.

Value offerings and initiatives

The Ohio-based retailer continues to build its value offerings and invest in various initiatives to drive growth. Its Fresh initiative is an important one. Kroger’s efforts in improving its supply chain efficiency, coupled with its vast store network, have helped it gain in this area.

Its private-label product line-up Our Brands also performed well in Q1 with sales growth of nearly 5%. Many customers are turning to Our Brands seeking value amid high inflation, with high-income customers buying premium Our Brands lines, providing more profit. As stated on its quarterly conference call, Our Brands typically provides 600-800 basis points higher margin compared to national brands.

Kroger’s digital sales grew 15% in Q1 2023, with an 11% growth in pickup and 30% growth in delivery solutions. The company expects to see continued growth in digital with double-digit sales increases through the rest of 2023.

Q1 results

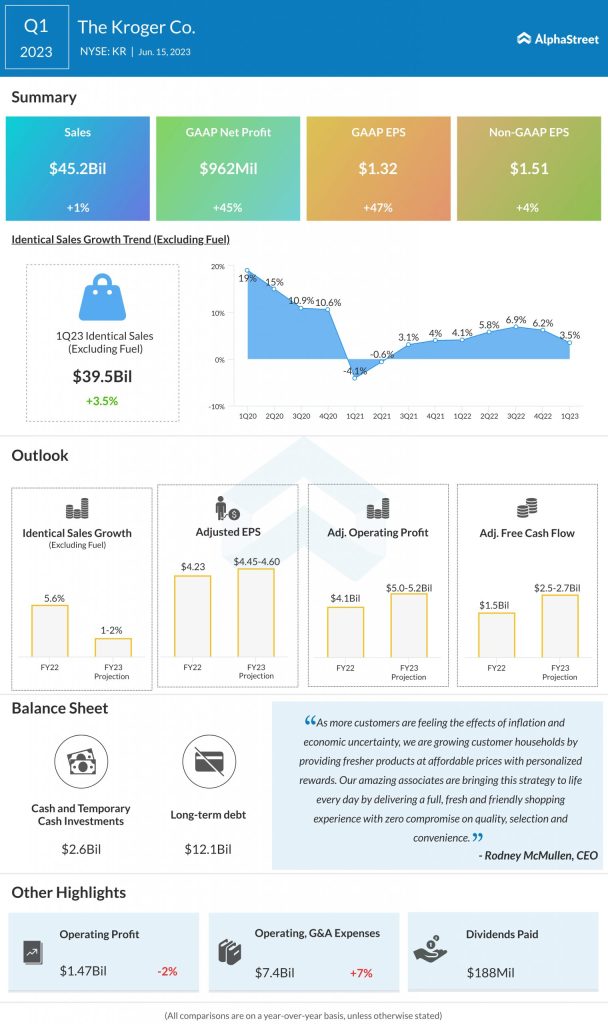

In Q1 2023, sales rose 1% year-over-year to $45.2 billion while adjusted EPS grew 4% to $1.51. Gross margin was 22.3%. The FIFO gross margin rate, excluding fuel, increased 21 basis points versus last year mainly due to the performance of Our Brands, lower supply chain costs, and sourcing benefits.

Outlook

Kroger expects inflation to decelerate through the year. The company expects identical sales, excluding fuel, to grow 1-2% in FY2023. Adjusted EPS is expected to range between $4.45-4.60 for the year.