The retail industry had a bit of a rough time over the past few months as inflation peaked and consumer shopping patterns shifted. As spending was pressured, the demand for essentials increased and a preference for value grew. This led to softness in certain categories and pressure on margins. Here’s a look at some of the recent trends experienced by a few leading retailers and their near-term expectations:

Rising costs and spending pressures

The hallmark of the past few months has been inflation which remains at an elevated level pressuring the spending ability of consumers. Consumers have chosen to focus more of their spending on essential items and put discretionary purchases on hold.

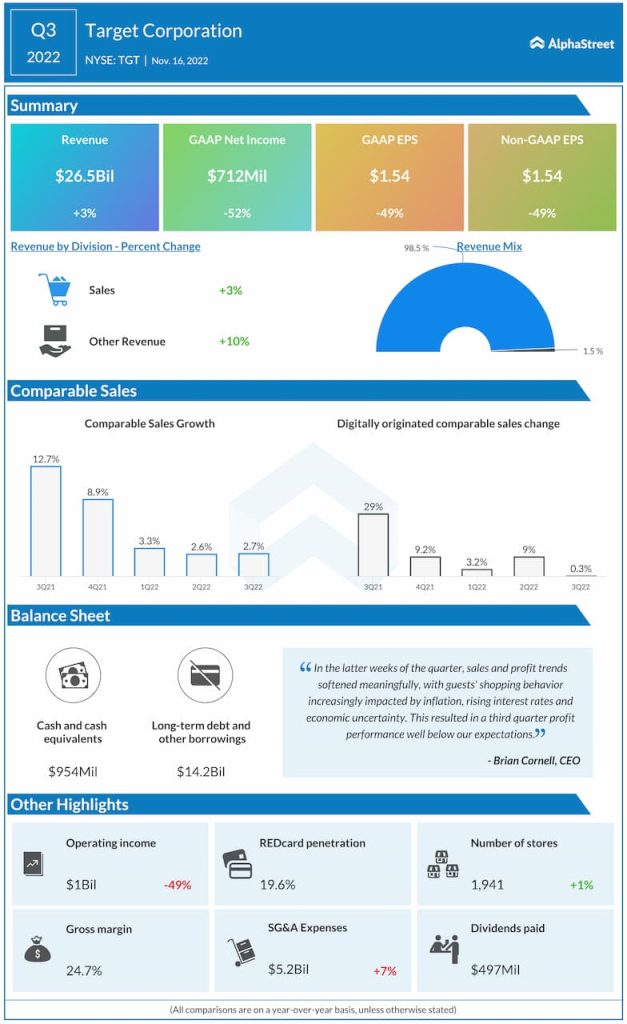

In such an environment, retailers like Target (NYSE: TGT) benefited from having a balanced multi-category portfolio as gains in categories such as food and beverage, household essentials and beauty helped offset softness in discretionary categories. This helped the retailer post a 3% growth in total revenue during the third quarter of 2022.

The inflationary environment has also led cost-conscious customers to turn to discount retailers like Dollar Tree (NASDAQ: DLTR) and Dollar General (NYSE: DG) for more value on their purchases. In Q3 2022, Dollar Tree and Dollar General saw their net sales increase 8% and 11% respectively, compared to the same period a year ago. Both discount retailers recorded same-store sales growth of over 6% during the quarter. They too saw their consumables categories outperform the discretionary categories amid the ongoing inflation.

Margins hit

Many retailers saw their margins being negatively impacted by heavy promotions and discounts as well as shifts in product mix. Target and Macy’s (NYSE: M) saw their gross margins get hurt by promotions and clearance markdowns. Target’s gross margin rate dropped to 24.7% in Q3 from 28% in the year-ago quarter as customers opted to buy at discounted prices instead of making full-price purchases.

Macy’s Q3 gross margin declined 230 basis points YoY to 38.7% due to an increase in promotional and clearance markdowns to sell lower-moving categories such as casual apparel and warmer weather seasonal goods.

Margins were also impacted by a higher portion of sales coming from the lower-margin consumables category. Dollar General’s gross margin dropped by 27 basis points in Q3 to 30.5% due to consumables making up a greater proportion of sales. Margins were also impacted by markdowns and inventory shrink. Dollar Tree’s gross margin improved 240 basis points to 29.9% in Q3 but was still impacted by a shift in product mix to consumables, higher shrink and markdowns.

Outlook

In the fourth quarter of 2022, Target expects to see softness in discretionary comps as well as pressure on margins from discounts. Weakness in the discretionary category is expected to be partly offset by strength in the frequency businesses. Macy’s expects sales of $8.1-8.4 billion in Q4.

Dollar Tree expects its net sales to range between $7.54-7.68 billion in Q4 and its same-store sales to increase in the mid to high single digits. Dollar General expects its same-store sales to grow 6-7% in the fourth quarter.