The cloud computing market witnessed accelerated growth in the last couple of years, as enterprises across the world shifted their digital assets to cloud for ensuring safety and enhancing data accessibility. But the digital transformation seems to be slowing down and cloud service providers have started feeling the pinch. Snowflake Inc. (NYSE: SNOW), a leading provider of data warehousing solutions, has been maintaining stable growth, supported by its unique multi-cluster shared data architecture.

The stock market performance of the Bozeman-headquartered tech firm was not very encouraging this year — the value more than halved since crossing $400 in November 2021 and hitting an all-time high. It has traded mostly sideways in the second half. But, the stock looks poised to take off from here, if the bullish outlook is any indication. Market watchers overwhelmingly recommend buying SNOW, citing the strong price target that represents a 40% growth, based on the last closing price.

Key Numbers

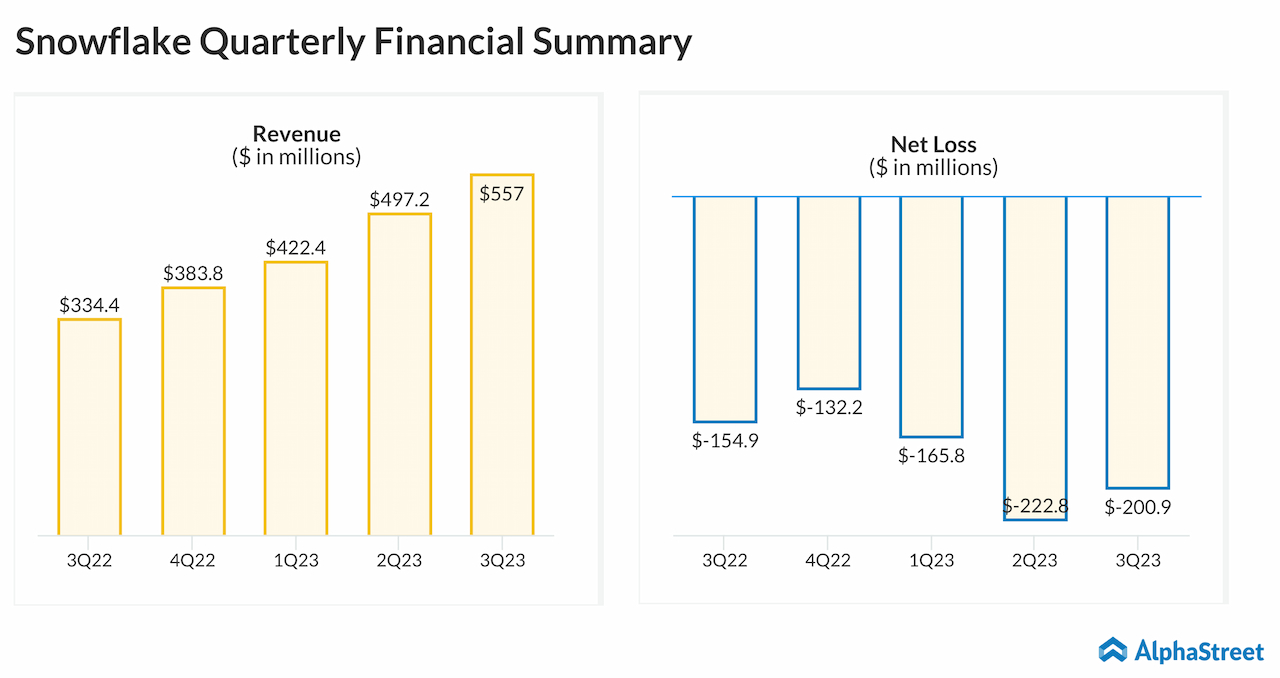

The October quarter was significant for Snowflake because it marked the company’s turnaround, after incurring back-to-back losses. Also, the bottom-line beat estimates for the first time since it started reporting quarterly results as a public entity, after a blockbuster public offering that is touted as the biggest IPO ever by a software firm. Adjusted earnings more than tripled to $0.11 per share from $0.03 per share last year. On an unadjusted basis, meanwhile, it was a net loss of $201.4 million or $0.63 per share, which is wider than the loss incurred in the prior-year quarter.

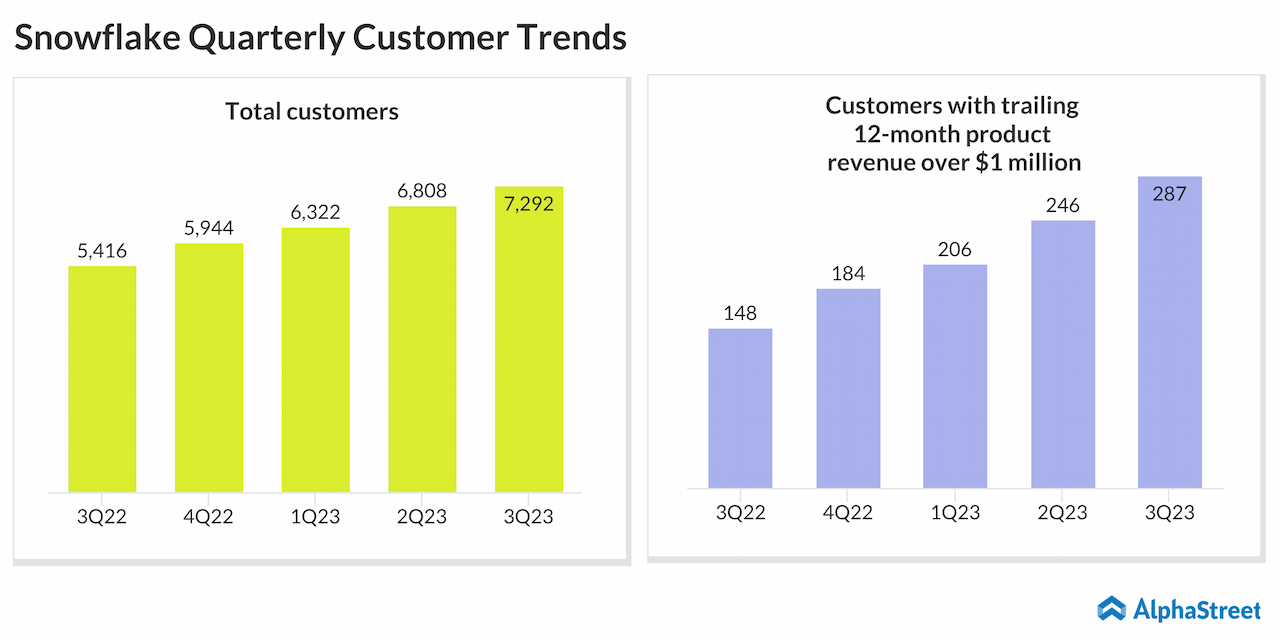

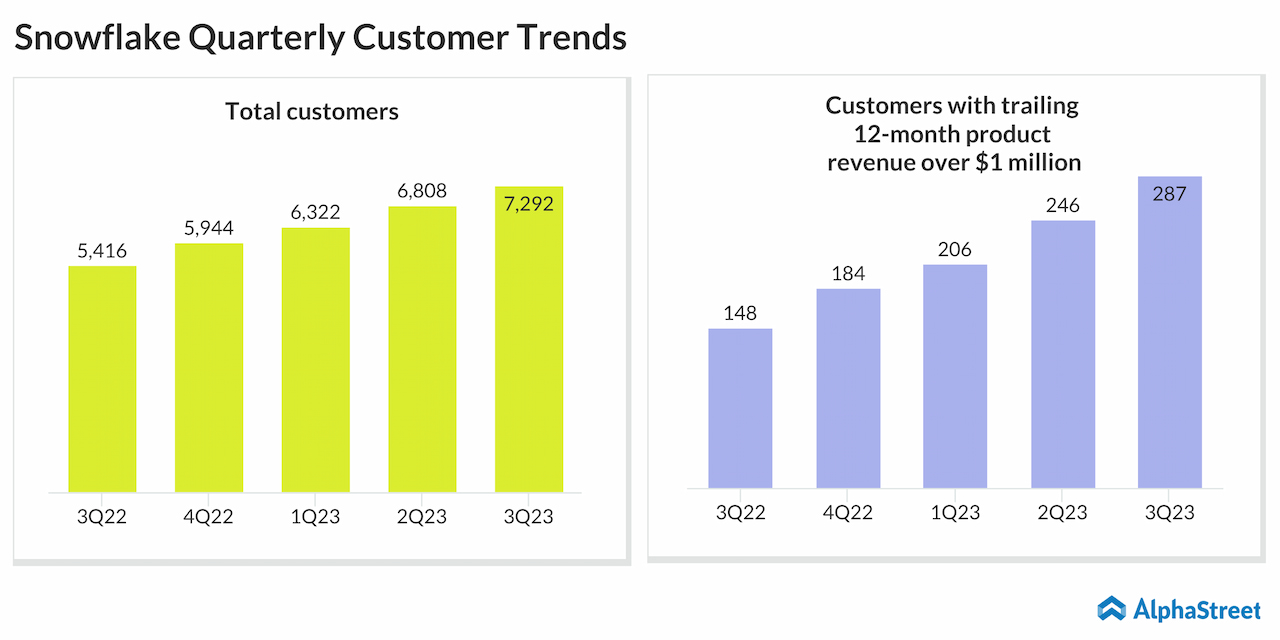

Remaining Performance Obligation, a measure of future performance obligations arising from contractual relationships — an important gauge of the company’s financial health — jumped 66% from last year to $3.0 billion in the third quarter. At $557.0 million, revenues were up 67% and above the Street view. The company had 7,292 customers at the end of the quarter.

Outlook

In an indication that the momentum would continue in the final weeks of the year, Snowflake’s executives predict that fourth-quarter product sales, which account for most of the total revenue, would grow by 50% to about $535-540 million. But the positive outlook failed to impress the market much as experts are looking for bigger growth.

CrowdStrike: Why this cybersecurity stock is a good investment for 2023

In the current economic environment, Snowflake’s consumption-based pricing — unlike others like Amazon Redshift which follows a subscription-based model — does not bode well for the company. On the other hand, the cloud market grew in double-digits in recent quarters despite the widespread slowdown. Though economic headwinds are forcing enterprises to cut down on technology spending, they wouldn’t want to compromise on their cloud capabilities due to the benefits they offer.

“For the full fiscal year 2024, we expect product revenue growth of approximately 47% and non-GAAP adjusted free cash flow margin of 23%, and continued expansion of operating margin. This outlook includes a slowdown in hiring, which we evaluate on a monthly basis, but assumes adding over 1,000 net new employees. Our long-term opportunity remains strong, and we look forward to executing. With that, operator, you can now open up the line for questions,” said Snowflake’s CFO Mike Scarpelli in a recent statement.

Investor sentiment improved since falling briefly following last week’s earnings report, and the stock recovered. After closing the last session lower, the shares experienced continued weakness during Monday’s session.