Shares of Target Corporation (NYSE: TGT) were down over 2% on Tuesday. The stock has dropped 11% over the past three months. The retailer faced a number of challenges during the first quarter of 2023 although it managed to deliver results in line with expectations. Furthermore, these headwinds are expected to persist in the near term. Here’s a look at some of the challenges faced by the company:

Flat sales and comps

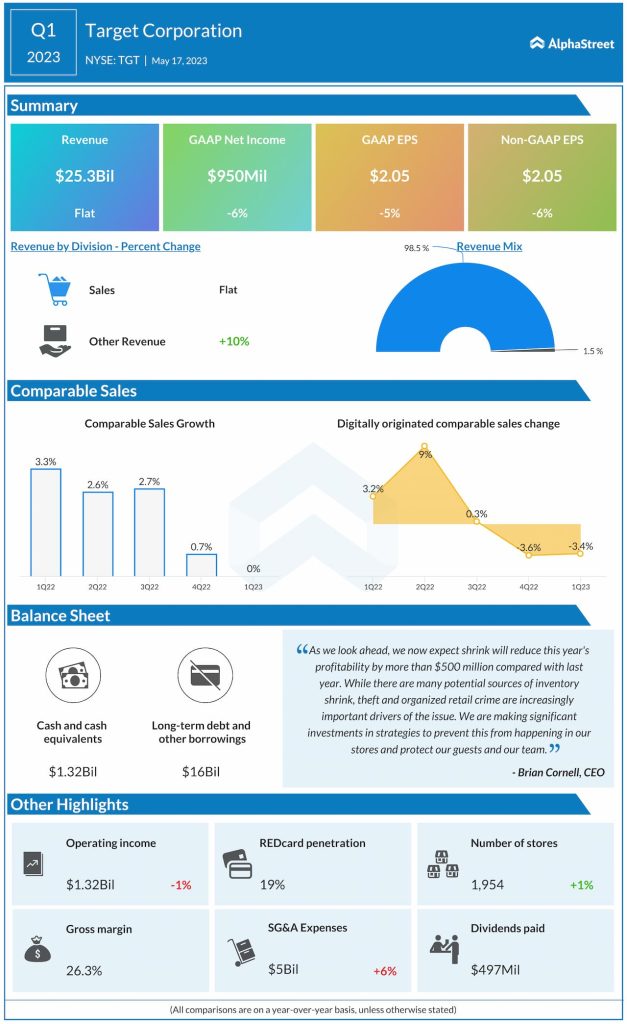

Target generated total revenue of $25.3 billion in the first quarter of 2023, which was up only 0.6% from the same period a year ago. Comparable sales were flat compared to last year while comparable store sales rose only 0.7%.

During the quarter, the company continued to see softness in its discretionary categories such as home, apparel and hardlines. After seeing strength in February, sales continued to decelerate through March and April. However, frequency categories such as food and beverage, household essentials, and beauty witnessed traffic and sales growth which helped offset the weakness in discretionary.

Target’s comp trends remained soft as it exited Q1 and moved into May. Based on this, the company is anticipating sales for the second quarter of 2023 in a wide range centered around a low single-digit decline in comps.

Decline in profits

In Q1 2023, Target’s net income decreased nearly 6% while EPS fell nearly 5% year-over-year. Operating margin was 5.2% compared to 5.3% last year. Gross margin, however, improved by 60 basis points to 26.3% compared to last year, helped by lower freight costs, lower clearance markdowns, and retail price increases.

Inventory shrink continues to pressure margins and if the current trends continue, the company expects shrink to reduce full-year profitability by more than $500 million compared to last year. Looking into the second quarter, Target expects a continuation of the trends seen in Q1, with a benefit from freight costs and challenges from inventory shrink.

Operating margin in Q2 2023 is expected to increase versus the prior-year quarter but on a sequential basis, it is expected to decrease. Both GAAP and adjusted EPS are expected to range between $1.30-1.70 in Q2.

Inflation and inventory shrink

Inflationary pressures continue to impact retail spending causing a drop in discretionary purchases. This has led to softer sales in Target’s discretionary categories. Another major headwind is inventory shrink which appears to be worsening from last year. On its quarterly conference call, Target said that violent incidents are increasing at its stores and across the entire retail industry. While the company is taking measures to tackle this issue, inventory shrink continues to take a toll on its profitability.