Shares of the JM Smucker Co. (NYSE: SJM) were up 5.3% on Tuesday after the company delivered better-than-expected results for the fourth quarter of 2022. However, the consumer foods manufacturer expects its performance in the upcoming year to be impacted by the product recall of its Jif peanut butter as well as likely headwinds from inflation and supply chain volatility.

Quarterly performance

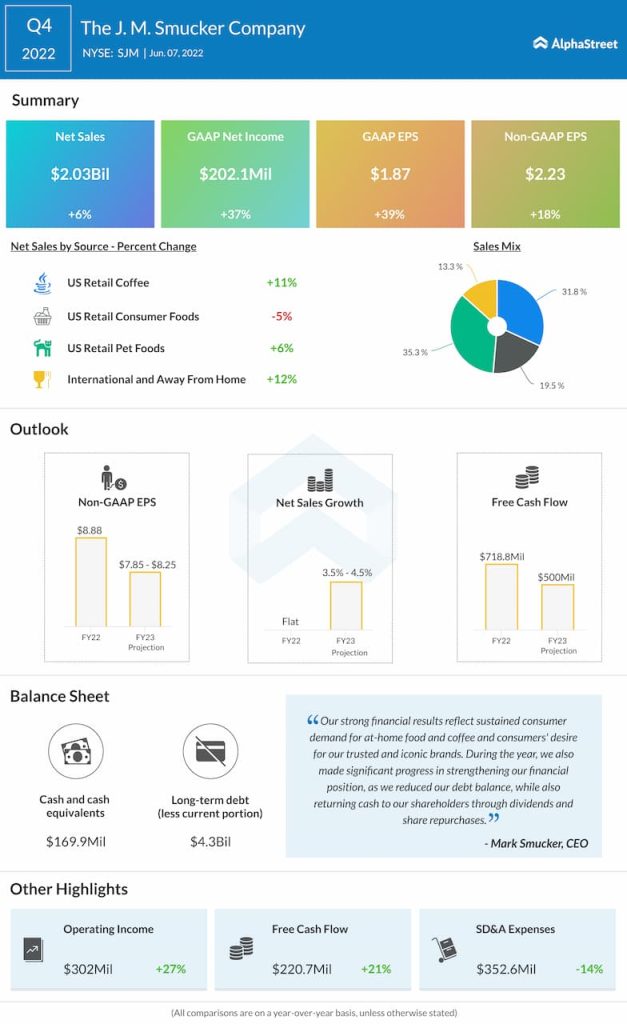

In Q4, net sales increased 6% year-over-year to $2.03 billion, beating consensus estimates. Net sales, excluding divestitures and foreign currency exchange, grew 9%. Adjusted EPS increased 18% to $2.23 also surpassing projections. Gross profit declined 9% in Q4 due to the impact of the estimated customer returns and inventory write-off related to the Jif peanut butter recall. Gross margin dropped to 32.8% from 38.3% in the prior-year quarter.

Product performance

JM Smucker posted sales growth across all its segments, on a reported basis, except for US Retail Consumer Foods where sales fell 5% due to the Jif peanut butter recall.

On its quarterly call, the company stated that strong demand for its brands supported overall market share gains during the quarter. Brands that are growing or maintaining dollar share accounted for 86% of its US Retail business in Q4, up from 57% in the prior-year period.

The US Retail Pet Foods segment benefited from double-digit growth in cat food and single-digit growth in both dog food and dog snacks. Within Pet Food, the Meow Mix brand gained nearly 3 points of share in Q4, growing over two times the category rate. In dog food, sales for the Nutrish brand grew 14%.

SJM is seeing strong momentum in its coffee portfolio as pandemic-fueled coffee habits continue and at-home coffee consumption remains high. In Q4, the company saw sales growth for its Café Bustelo, Dunkin and Folgers brands.

Sales growth in the Consumer Foods business was driven by gains in Smuckers fruit spreads, Uncrustables frozen sandwiches and Sahale snacks. Total net sales for Uncrustables was approx. $130 million in Q4 for the combined US Retail and Away From Home businesses and SJM believes it can grow to a $1 billion brand in annual net sales over the next five years. The International and Away From Home segment recorded 12% sales growth in the quarter.

Outlook

Looking ahead to FY2023, SJM believes headwinds from supply chain disruptions and cost inflation could take a toll on its performance. It also expects the Jif peanut butter product recall to impact its results for the year. Reported net sales are expected to grow 3.5-4.5% while comparable net sales are expected to grow 6% in FY2023. This includes a 2% impact related to the Jif peanut butter recall. Adjusted EPS is estimated to range between $7.85-8.25, including a $0.90 impact from the Jif product recall. In Q1 2023, net sales are expected to be flat while earnings are expected to decline around 35%, mainly due to negative impacts from the Jif recall.

Click here to access the full transcripts of the latest earnings conference calls