Shares of Campbell Soup Company (NYSE: CPB) were up 1% on Thursday. The stock has gained 30% year-to-date and 34% over the past 12 months. The food company started the fiscal year on a strong note, delivering impressive results for the first quarter of 2023 and raising guidance for the full year. Here are three factors that bode well for Campbell in the current environment:

Strong quarterly performance

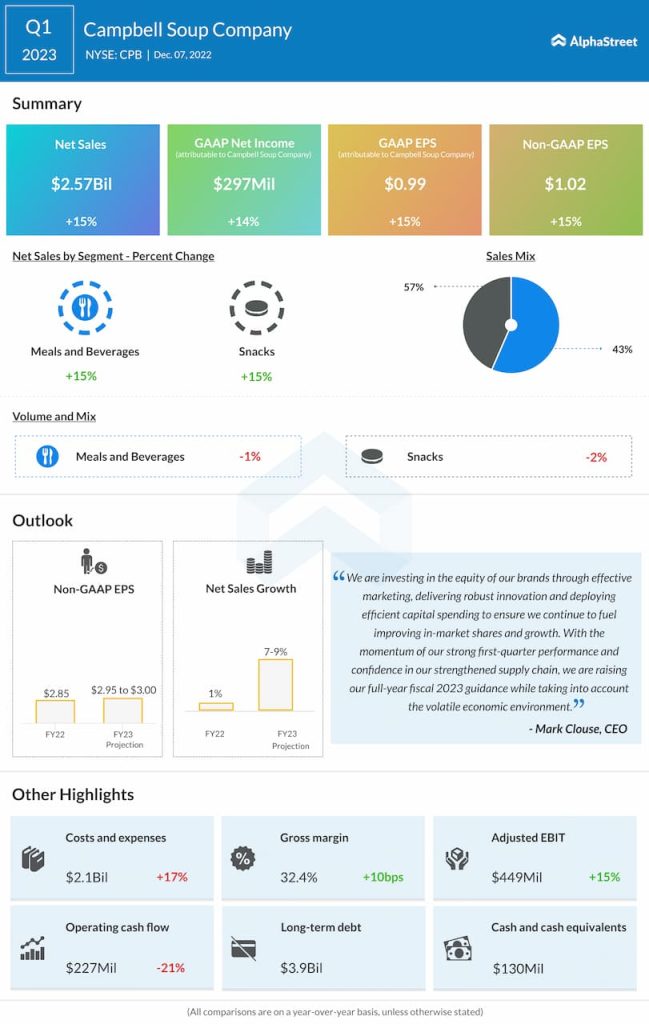

Campbell beat market expectations on revenue and earnings, both of which saw double-digit growth. Net sales in Q1 2023 rose 15% year-over-year, both on a reported and organic basis, to $2.6 billion, driven by pricing and strong consumer demand. Adjusted EPS also grew 15% to $1.02.

Demand and portfolio strength

On its quarterly conference call, Campbell mentioned that in the current inflationary environment, consumers are cutting back on out-of-home eating and are also moving away from more expensive grocery categories. They are making changes to stretch their budgets and are preparing about 80% of meals from home. This preference for simple at-home meals and quick-scratch cooking is driving demand for Campbell’s brands within its Meals & Beverages business.

In Q1 2023, net sales in the Meals & Beverages segment increased 15%, both on a reported and organic basis, to $1.45 billion compared to last year. The growth was driven mainly by increases in US retail products, including US soup and Prego pasta sauces, as well as gains in foodservice.

Net sales in US soup grew 11% year-over-year helped by gains in ready-to-serve, condensed and broth. Campbell also saw strength in its sauce business with encouraging performances from the Prego and Pace brands.

In the Snacks division, net sales rose 15%, on both a reported and organic basis, to $1.12 billion. The growth was driven by a 21% increase in sales of power brands. The company benefited from gains in cookies and crackers and salty snacks. During the quarter, brands such as Goldfish, Cape Cod and Kettle delivered strong growth outperforming their categories.

During the quarter, in both segments, inflation-driven pricing and sales allowances were partly offset by volume declines. Campbell expects cost inflation to continue throughout FY2023. The company is implementing additional pricing in both its divisions and this is expected to become effective in the second half of the fiscal year.

Raised outlook

Campbell raised its guidance for the full year of 2023 based on strong Q1 results and brand demand. The company now expects net sales, both reported and organic, to grow 7-9% from FY2022. This compares to the previous outlook of 4-6% sales growth. Adjusted EPS is now expected to be $2.90-3.00 versus the previous range of $2.85-2.95.

Click here to read the full transcript of Campbell Soup’s Q1 2023 earnings conference call