Shares of Signet Jewelers Limited (NYSE: SIG) were over 3% on Monday. The stock has dropped 13% over the past 3 months. The jewelry retailer is set to report its first quarter 2024 earnings results on Thursday, June 8, before market open. Here’s a look at what to expect from the earnings report:

Revenue

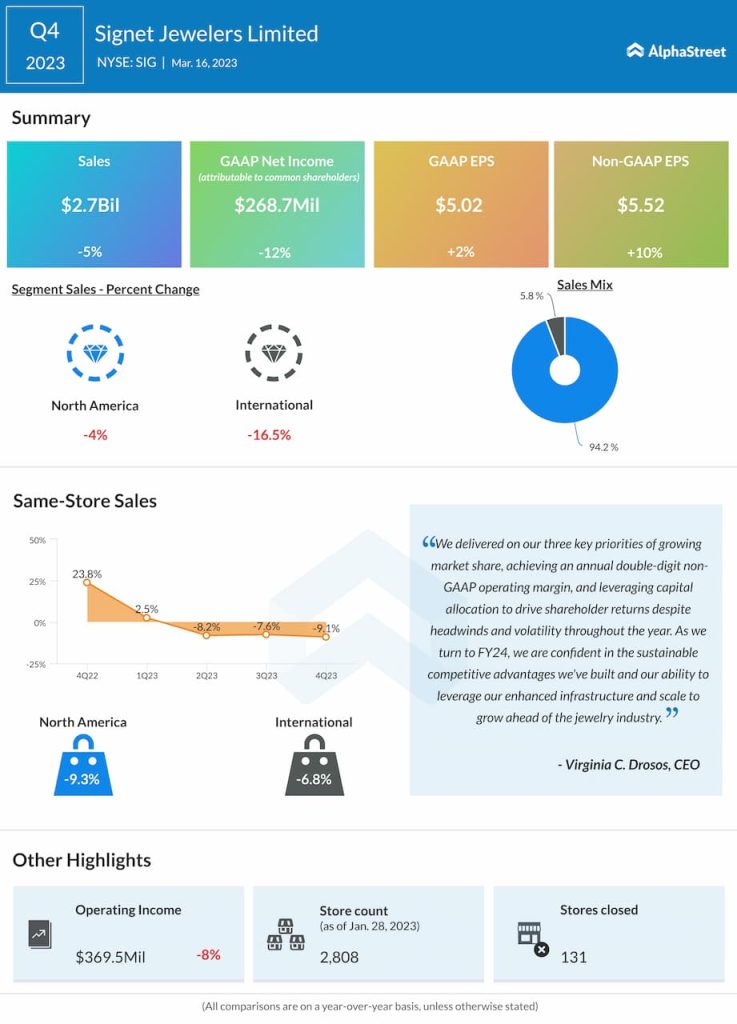

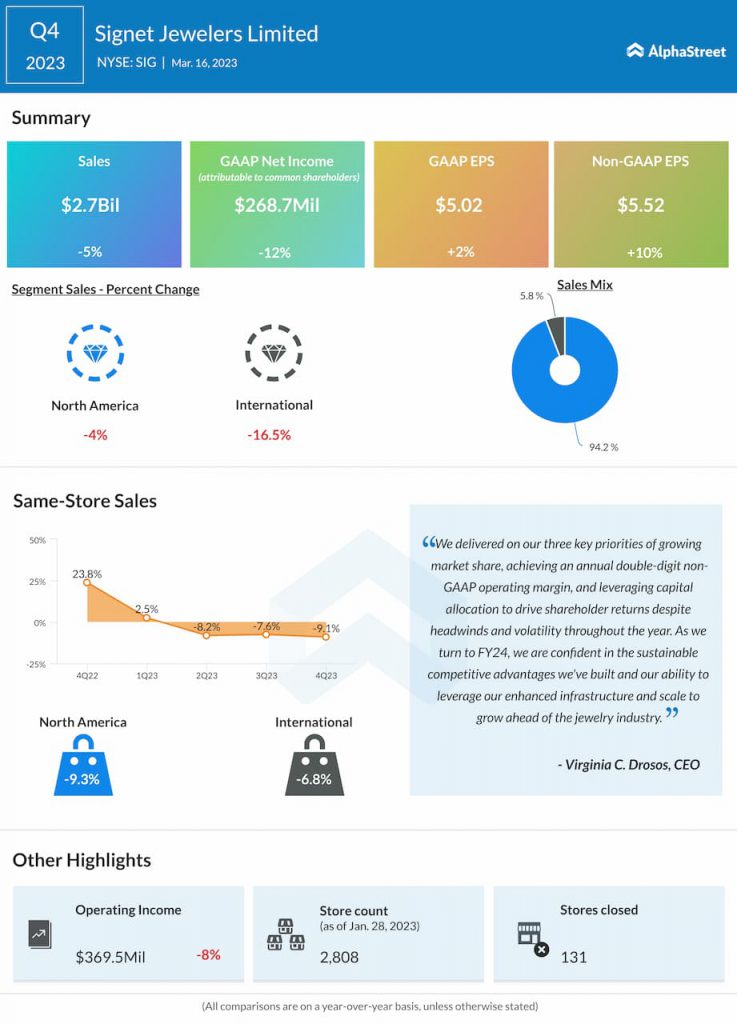

Signet has guided for sales of $1.62-1.65 billion for the first quarter of 2024. Analysts are projecting revenue of $1.65 billion, which would reflect a decline of 10% from the same period a year ago. In the fourth quarter of 2023, net sales dropped 5% year-over-year to $2.7 billion.

Earnings

The consensus estimate for EPS is $1.18, which would reflect a drop of 59% from the prior-year period. In Q4 2023, adjusted EPS grew 10% YoY to $5.52.

Points to note

Signet can be expected to benefit from its varied and distinctive portfolio as well as its connected commerce presence. Strength at its higher price points and within its fashion assortment is helping offset the softness in the bridal category.

Signet expects the jewelry industry to witness a decline in FY2024 as it goes through a challenging environment. These headwinds are expected to impact the company’s top line performance for the year as well.

The bridal segment is an important one for Signet. Bridal is divided into two key parts – engagements and weddings. The company saw strong growth in wedding bands and bridal jewelry in FY2023 whereas engagements saw a decline during the year. The jeweler expects to see a low double-digit decline in engagements during FY2024 as well. It expects engagement ring sales to start recovering toward the end of FY2024 and then continue to pick up over the next two years.

Signet’s efforts in optimizing its store footprint and its investments in digital technology can also prove beneficial to its business performance. Its connected commerce presence will continue to provide it with a competitive advantage.