Meta Platforms, Inc. (NASDAQ: META) is bringing a new era to social media by transforming user experience through the use of technologies like artificial intelligence and virtual reality. Currently, the tech firm is ahead of its peers in digital advertising and user engagement. In the most recent quarter, ad impressions increased by a fifth, and price-per-ad rose by 6% year-over-year across the company’s social networks known as the Family of Apps.

Last week, the Menlo Park-based firm’s stock set a new record after growing steadily since the beginning of the year, but it pulled back later and pared a part of the gains. Interestingly, the stock price has almost doubled since mid-2023. It has outperformed the broad market quite often in recent years. Earlier this year, Meta announced its first-ever cash dividend of $0.50 per share amid continued efforts to achieve better capital discipline. Despite the recent gains, the stock still looks reasonably priced.

Positive Shift

Recent trends on the platform indicate that AI-generated content is increasing — with the potential to replace traditional feeds in a big way going forward — attracting advertisers and enhancing user engagement. Capital spending is expected to keep growing this year and beyond, due to aggressive investments to support AI research and product development. Meta is likely to maintain its social media dominance in the foreseeable future aided by the strong network effect, diversified revenue streams, and advanced advertising tools. Moreover, the company has invested billions of dollars in its futuristic multi-dimensional virtual space called Metaverse, a concept that is expected to revolutionize social networking.

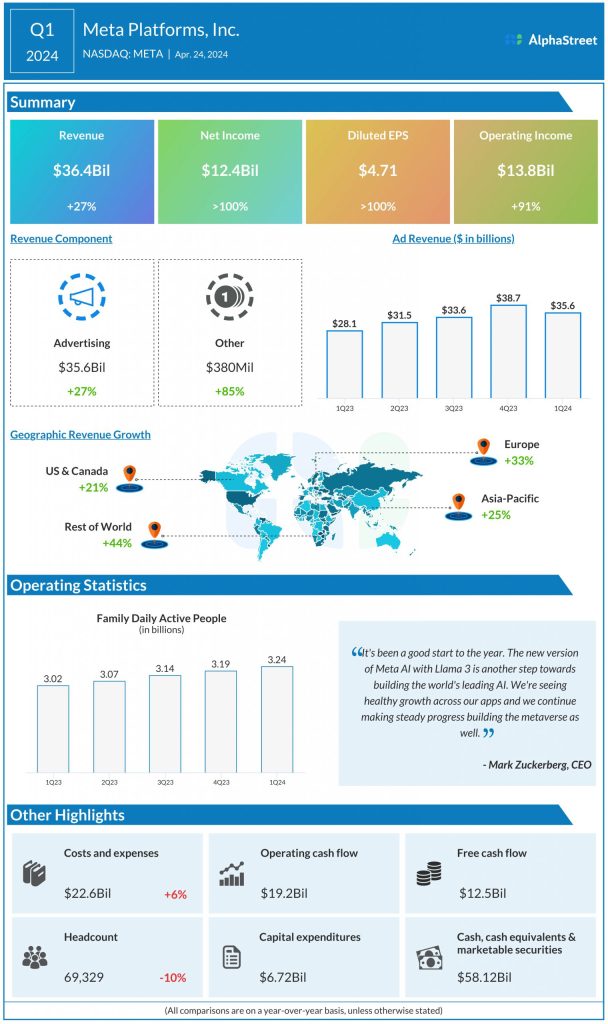

In the first quarter of 2024, revenue increased 27% year-over-year to $36.4 billion. Revenue grew in double digits across all geographical regions. Driven by the strong top-line growth, net income more than doubled year-over-year to $12.4 billion or $4.71 per share in Q1. The company ended the quarter with an impressive free cash flow of $12.5 billion. Earnings exceeded expectations, marking the fifth beat in a row.

Growing User Base

The number of family daily active people, which refers to registered and logged-in users of one or more of the family of apps who visited at least one of the sites on a given day, increased 7% during the three months. For the second quarter, the management expects total revenue to be in the range of $36.5 billion to 39.0 billion. Full-year 2024 capital expenditures target has been raised to $35 billion to $40 billion from the prior range of $30-37 billion, mainly to reflect higher spending on AI research.

From Meta’s Q1 2024 earnings call:

“Our investments in developing increasingly advanced recommendation systems continue to drive incremental engagement on our platforms, demonstrating that people are finding added value by discovering content from accounts they’re not connected to. The level of recommended content in our apps has scaled as we’ve improved these systems, and we see further opportunity to increase the relevance and personalization of recommendations as we advance our models. Video also continues to grow across our platform, and it now represents more than 60% of time on both Facebook and Instagram.”

After withdrawing from last week’s all-time high, Meta’s shares traded higher in the early hours of Tuesday. The price has stayed above its 52-week average in the past four months.