Cisco Systems Inc. (NASDAQ: CSCO) is the undisputed leader in networking technology, but its core business has been facing challenges over the past few years. While the company faces stiff competition from others like Huawei, its applications business is affected by the pandemic-related disruption.

The stock suffered one of the worst single-day losses this week after the company’s first-quarter revenues missed estimates and the management issued a cautious outlook. CSCO closed the last trading session down a dismal 13%, continuing the post-earnings decline.

The Stock

But the downtrend is unlikely to last for long as Cisco is well-positioned to ride the recovery wave that is expected to come soon. The stock has long been an investors’ favorite, and the low valuation makes it more attractive now. The company has dominated the industry for a long time and maintained a healthy balance sheet. That, combined with strong fundamentals, makes it a safe long-term investment. In the present condition, however, it might disappoint short-term investors.

Read management/analysts’ comments on quarterly reports

While margins remain under pressure from supply chain disruptions, the tech firm looks on track to achieve its long-term growth target. The recent reshuffle of reporting segments would give a better picture in terms of individual financial performance. That will allow the management to set strategies more effectively.

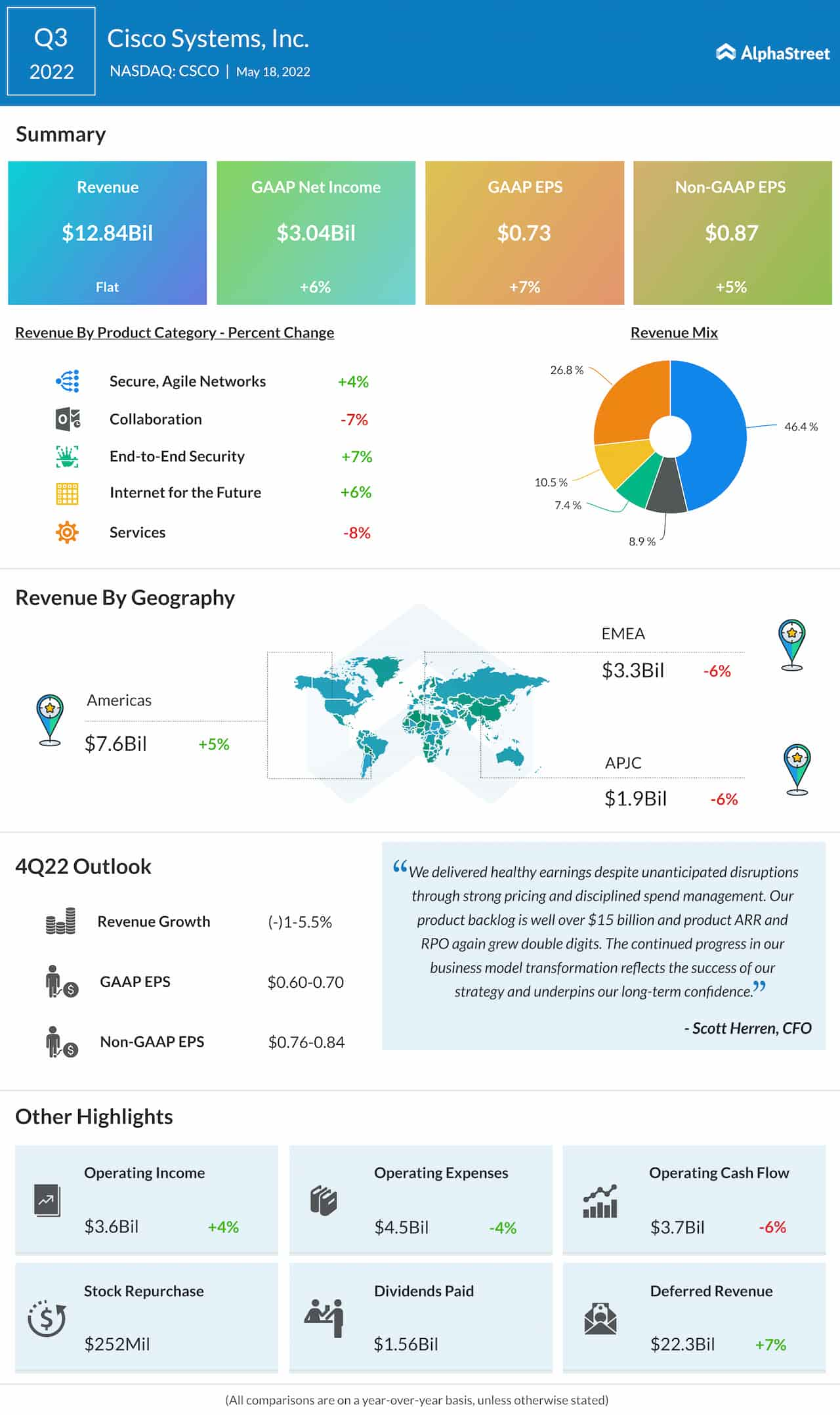

Cisco experienced an unexpected slowdown in sales in the most recent quarter, reflecting the macroeconomic headwinds and COVID-related supply chain issues. As a result, revenues remained unchanged year-over-year at $13 billion and fell short of expectations. Meanwhile, adjusted profit rose to $0.87 per share and slightly exceeded analysts’ view. It is estimated that the softness in top-line performance continued in the current quarter, and the management predicts a single-digit decline in revenues for that period.

From Cisco’s Q3 2022 earnings conference call:

“We believe that our revenue performance in the upcoming quarters is less dependent on demand and more dependent on the supply availability in this increasingly complex environment. While certain aspects of the current situation are largely out of our control, our teams have been working on several mitigation actions to help alleviate many of the component issues that we’ve been facing. We believe that we will begin to see the benefits of these actions in the first half of next fiscal year.”

Microsoft Q3 revenue up 18%, earnings beat estimates

Currently, Cisco’s stock is trading at the lowest level in nearly six months, with the unimpressive first-quarter numbers adding to the weakness. It has lost about 34% so far this year, with most of that coming after the earnings release.