The pharma sector has been on a stable growth trajectory lately, and the trend gathered momentum when the pandemic-related emergency made companies shift their focus to vaccine development. But, Bristol-Myers Squibb Company (NYSE: BMY) is going through a rough patch due to the expiration of some of its key patents. While the management bets on the promising pipeline to stay afloat, the uncertainties related to product development remain a concern.

The New York-based firm is at the risk of losing revenue to the generic versions of its top products like multiple myeloma drug Revlimid and Eliquis going forward. But, the impact would ease in the long run because the company has a number of new drugs getting ready for launch and it is ramping up existing products, with focus on expanding indications.

Buy BMY?

The stock got a much-needed push from the company’s strong third-quarter report and entered the new year on a positive note, but the valuation is still cheap. Experts are of the view that BMY would maintain the uptrend, gaining about 8% in the next twelve months. A section of analysts following the stock are bullish on its prospects but the high volatility calls for caution, especially if one is looking for a short-term engagement.

Pfizer stock research summary | Q3 2021

While there is enough reason to believe that BMY would enrich investors’ portfolios in the long term, the potential impact of patent-expiry on the business makes it a risky bet now. It might take a few years for the positive effects of the portfolio revamp to start reflecting in Bristol-Myers’ finances. On the positive side, the management is pursuing aggressive stock buyback and dividend programs. Also, the company enjoys strong cash flows and has remained profitable irrespective of the market environment.

New partnerships and portfolio expansion top the management’s growth strategy. It is also looking for suitable acquisitions in areas like immunology and hematology, encouraged by the success of past deals like the high-profile acquisition of Celgene, the maker of Revlimid.

Growth Strategy

There is a slew of successful products like Breyanzi — the lymphoma drug that hit the market recently — which have the potential to drive future revenue growth. Recently, the company forged a research tie-up with Century Therapeutics (NASDAQ: IPSC) to develop therapies for hematologic malignancies and solid tumors.

Meanwhile, it needs to be seen if the new launches and upcoming products would compensate for the revenue loss caused by the generic invasion. It’s a fact that the Bristol-Myers pipeline is not as strong as that of many competitors.

From Bristol-Myers Squibb’s Q3 2021 earnings conference call:

“We’ve executed several business development deals this year, bringing in differentiated early-stage assets. Business development remains a top priority as a leading innovation-based company. We have paid down $6 billion in debt year-to-date, and are committed to maintaining our strong investment-grade rating. As it relates to returning capital shareholders, we’re committed to growing our dividend subject to board approval and remain opportunistic about share repurchases.”

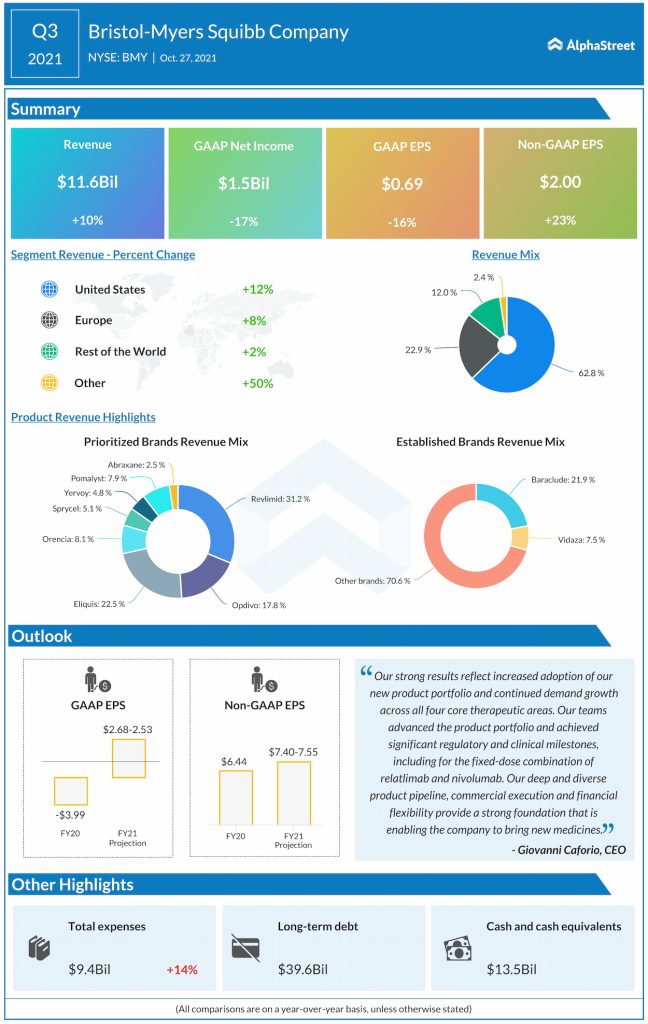

In the third quarter of 2021, sales grew across all geographic segments, and total revenues jumped 10% to $11.6 billion. At $2 per share, adjusted earnings were up 23% year-over-year. The numbers were also above the market’s projection. As per the management’s guidance, full-year revenue is seen increasing in high-single digits, while net profit is estimated to have grown at a slightly faster pace than initially estimated.

Q4 Report Due

The picture will become clearer when the company reports its fourth-quarter numbers on February 4 before regular trading starts. It is widely expected that earnings would grow sharply to $1.82 per share on revenues of $12.11 billion, which represents a 9% growth. Beyond that, the top-line is expected to grow at a slower pace in the next fiscal year, reflecting the moderation in the sales of Revlimid.

Johnson & Johnson reports Q3 2021 earnings

The stock is currently trading close to the levels seen twelve months ago, after experiencing high volatility during that period. It traded higher in the early hours of Monday, after closing the previous session higher.