You probably love traveling with JetBlue

(NASDAQ: JBLU) for the ample legroom, seats with TVs and various snack options.

But is New York’s hometown airline worth your investment. Let’s dig deep.

Overview

As of December 31, 2018, JetBlue operated a fleet of 63 Airbus A321 aircraft, 130 Airbus A320 aircraft, and 60 Embraer E190 aircraft. Notably, it does not operate Boeing 737 Max airline, which was grounded earlier this month citing safety concerns. Therefore, it’s stock has remained relatively unhurt by the recent Boeing crisis.

JetBlue flies to 105 destinations in the 31

states in the United States, the District of Columbia, the Commonwealth of

Puerto Rico, the US Virgin Islands, and 21 countries in the Caribbean and Latin

America.

Competition

and market share

JetBlue Airways competes mainly with United

Airlines (NYSE:

UAL), Southwest Airlines (NYSE: LUV),

Delta Air Lines (NYSE: DAL),

American Airlines (NYSE: AAL)

and Alaska Air Group (NYSE: ALK).

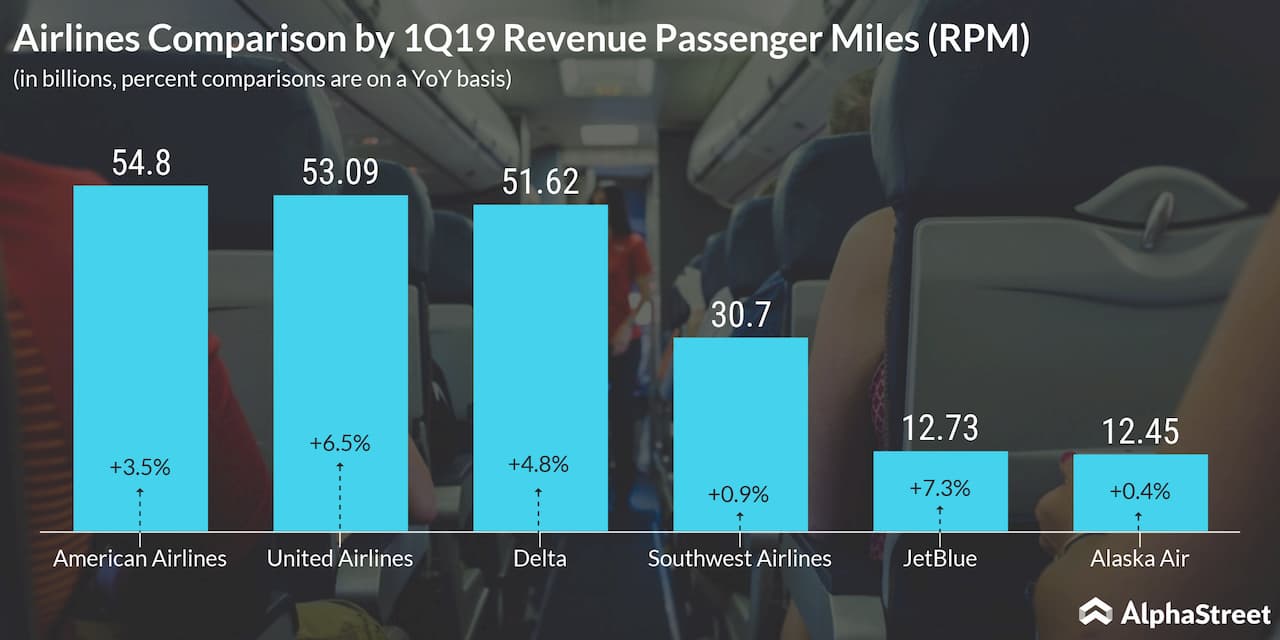

Based on data from the Bureau of Transportation,

as of March 2019, JetBlue stood at the sixth position in terms of revenue

passenger miles (RPM) with a 5.6% share, trailing behind the rest of its

aforementioned competitors. American topped the chart in this metric.

But this is primarily because it does not fly to all corners of the world, as United or American does, and focuses operations mostly in and around America.

Meanwhile, JetBlue has been struggling with

declining load factor, suggesting few occupied seats in its aircraft. Load

factor declined 3.7% in March, and witnessed further declines of 0.6 percentage

points in April. In May, it showed a slight improvement of 0.2 percentage

points, but it needs to be seen if this can be sustained.

Financials

Jetblue has a remarkable history of beating Wall Street estimates. The company has reported earnings above the street consensus in all four trailing quarters, with an average surprise of 14.4%, helped by lower-than-expected fuel prices and rating upgrades.

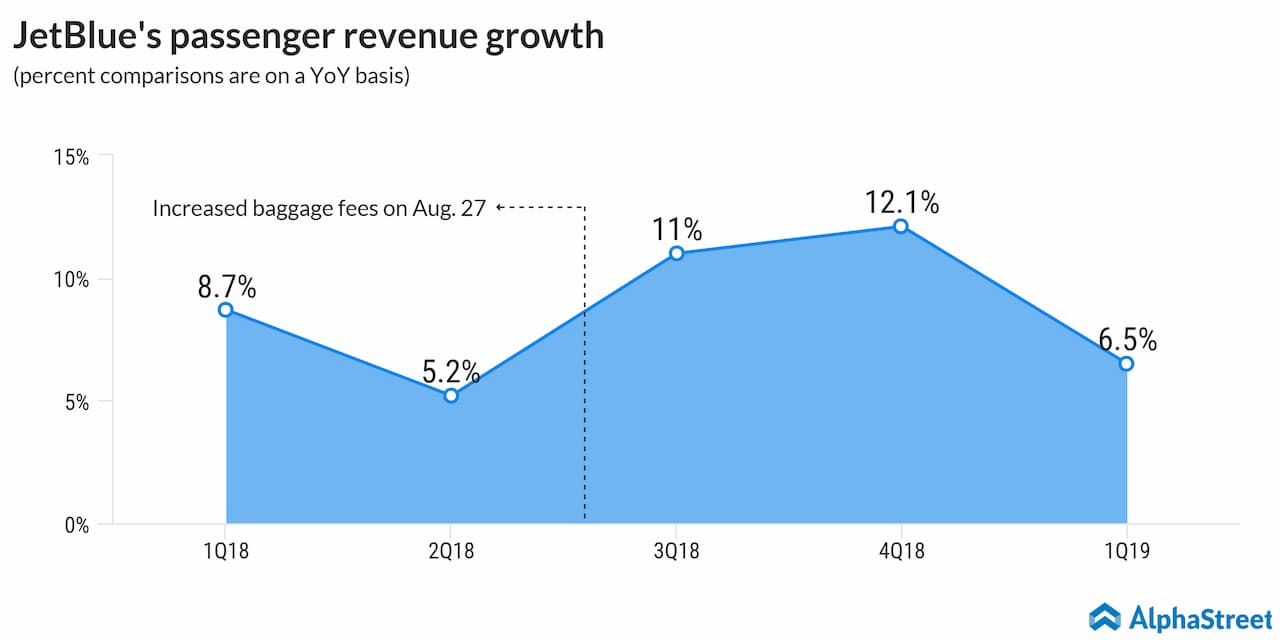

The

company had last year raised

its baggage fees in a move to moderate its rising operating expenses. The

New York-based aviation company started charging passengers $30 for the first

checked bag, which was higher than the industry standard of $25. However, this

move has hardly affected its passenger revenues (see fig).

For the current fiscal year, the company is expected to see a 6.5% growth in revenues, better than most other US airlines.

Cash position

JetBlue typically uses most of the cash

generated from operations for capital investments, resulting in relatively weak

free cash flow. Going forward, the company will likely be able to improve its

cash position aided by the growing demand for business travel and favorable

pricing, while maintaining the level of capital expenditure.

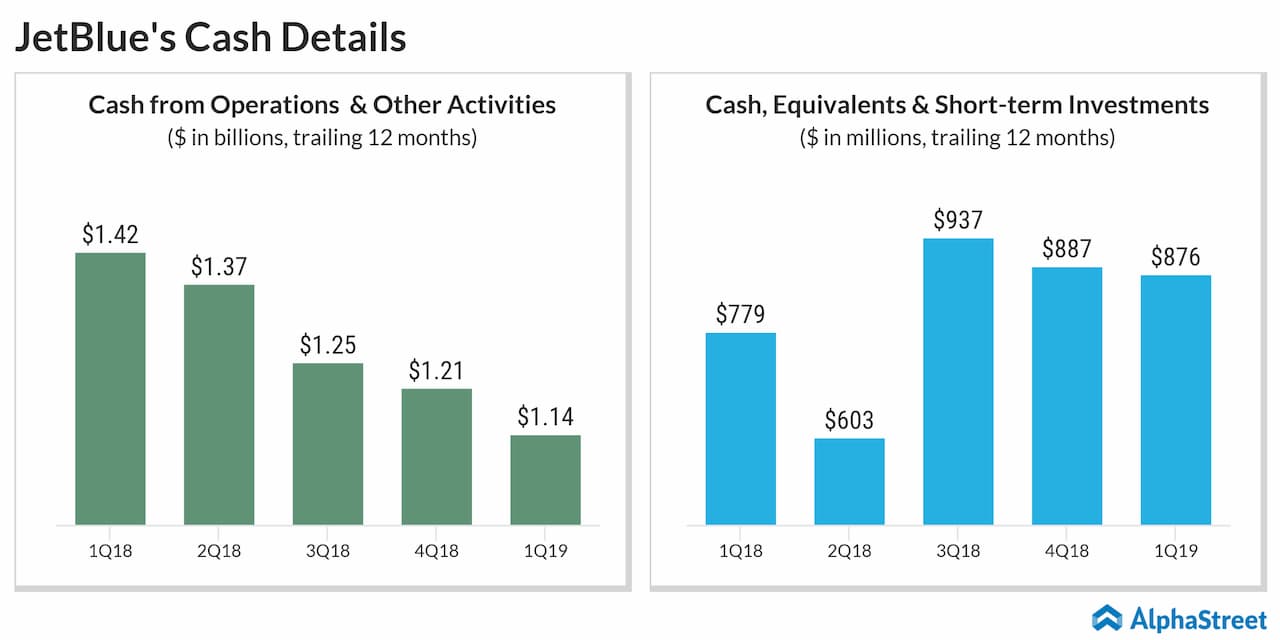

In fiscal 2018, the airline recorded

operating cash flow of $1.2 billion, which is less than the previous year’s

$1.4 billion. High capital spending restricted free cash flow to just above

$100 million last year. Since 2014, operating cash flow increased by around 33%.

At the end of March 2019, the company had $1.14 billion in cash from operations and other activities. Cash, equivalents and short term investments came in at $876 million.

Though total debt and capital lease

obligations increased 39% year-over year to $1.68 billion at the end of 2018, it

is deemed sustainable as the company has sufficient cash to cover long-term

liabilities. However, the ongoing growth initiatives require additional external

funding and the repayment obligations are bound to put pressure on liquidity.

Wall

Street view

Out of the 6 analysts tracked by TipRanks, three have awarded JBLU Buy rating, and the rest recommend Hold. The analysts expect the airline’s stock to touch $22.42 in the next 1 year, which is an increase of 24% from today’s trading level.

JetBlue is benefiting from falling aviation

fuel costs and ongoing cost-cutting measures, which is going to be accretive to

earnings in the latter half of the year. However, the company has set itself an

ambitious earnings target of $2.50 to $3.00 for 2020 period. On the flip side,

analysts are expecting EPS of $2.35 for the fiscal 2020 period.

Earlier this month, Citi analyst Kevin Crissey in his research note stated, “With fuel prices now well below levels when guidance was provided, [revenue per available seat mile] can be weak or even negative, and JetBlue can still exceed consensus.”