FireEye’s (FEYE) stock dwindled 12% in February when the cyber security firm reported weaker full-year guidance despite reporting solid Q4 results. The company is moving towards subscription-based model from products-based offering and also faces intense competition from its peers.

As the transition continues, the company’s top line might be impacted from muted growth recorded from the products front since it contributed 60% to the top line last year. In addition, FireEye already alerted investors last quarter that it would not see any deals greater than $10 million in the first quarter 2019 which might make further dent sales growth compared to last year where it won few big deals.

Amidst this backdrop, FireEye is reporting its first quarter results tomorrow after the bell. The street is anticipating revenue to grow by 5.6% to $210.2 million and loss of 3 cents for the Q1 period. Last year, the cyber security firm reported sales of $199 million and 4 cents loss per share.

Key Metrics to Watch

Billings: FireEye saw double-digit growth in billings of 12% last year. Last quarter, the company added 354 clients and out of that 60 were $1 million clients. In addition, the average contract length, excluding $10 million deals, improved to 25.7 months over 24.5 months reported last year. The improvement in contract length is a good sign for investors as it would bring in stable recurring revenues and improved consumer stickiness.

Deferred Revenue: Last quarter, the company saw a growth of 2.7% in deferred revenues. FireEye has already alerted about large deal headwinds which would impact deferred revenues. Growth in deferred revenues depends on the number of new customer additions and the deal value signed by the firm.

Fiscal 2019 Outlook

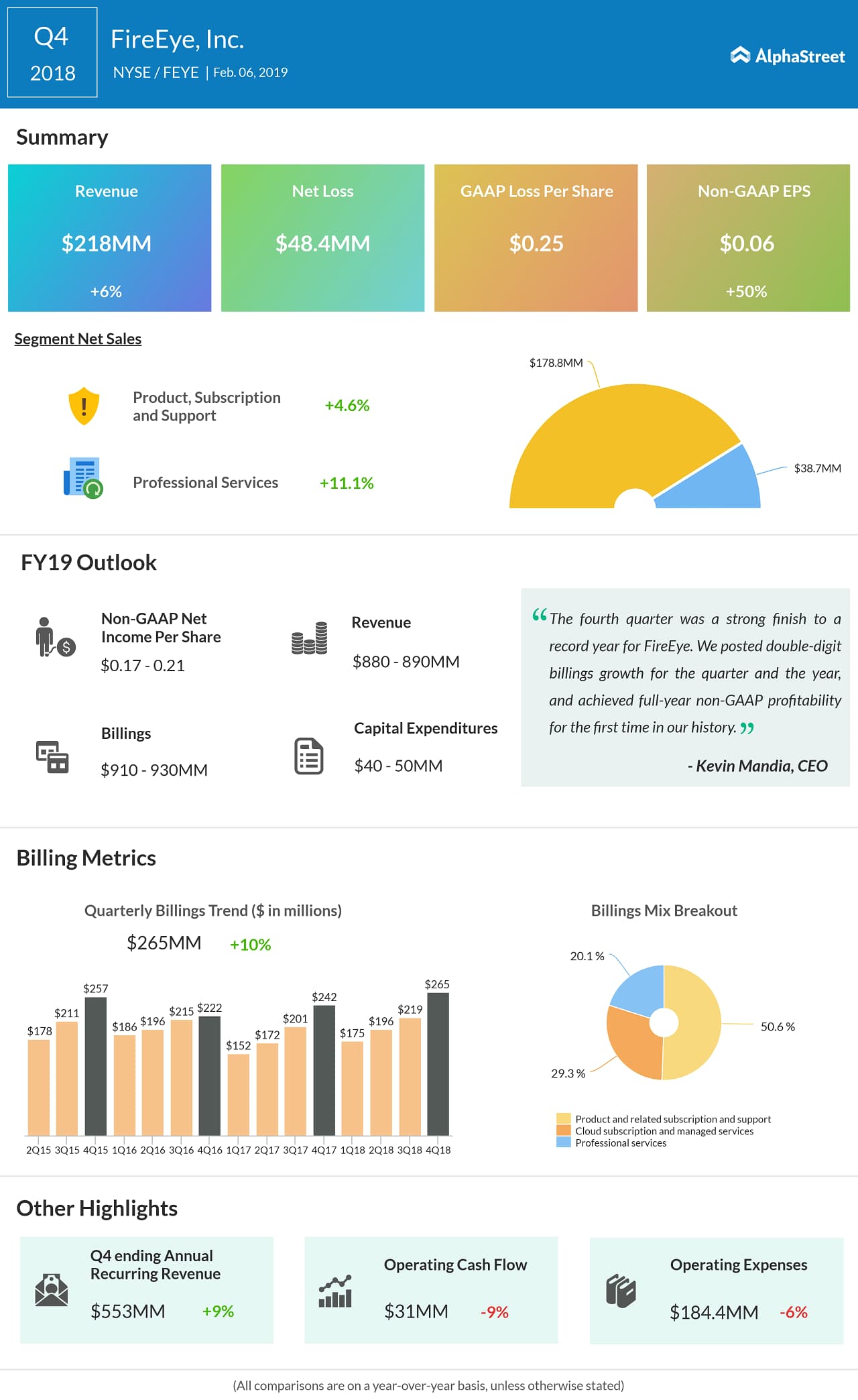

For the current fiscal year, FireEye expects top line to be between $880-890 million backed by billings of $910-930 million. Adjusted earnings is projected in the range of $0.17-0.21 per share. Street is expecting earnings of $0.19 per share on revenues of $886.25 million for the fiscal 2019 period.

Looking Back

Last quarter, sales improved 6% to $218 million backed by double-digit growth in billings and earnings surpassed estimates by a cent at $0.06 per share. Subscriptions grew 4.6% while professional services improved 11% in the quarter.