After an unimpressive holiday quarter performance, athletics apparel retailer Foot Locker, Inc. (NYSE: FL) is on a drive to reset the brand for serving a broader customer base. It is planning to make big investments in the main brands and capabilities, while also adopting measures to streamline operations.

The New York-headquartered sneaker company bets on the strength of its core business and favorable inventory position to meet near-term growth goals. The management has launched what it calls the ‘Lace Up’ plan, with strategies and financial objectives designed for successful operations in the next 50 years.

The Stock

Over the past twelve months, Foot Locker’s stock has gained about 38% and it maintained the momentum this week amid the market’s mixed response to the fourth-quarter report. The management’s remarks on the company’s revitalized relationship with top brand partner Nike, Inc. (NYSE: NKE) had a positive effect on investor sentiment.

Read management/analysts’ comments on quarterly reports

Currently, Foot Locker is planning to close around 400 underperforming stores in malls and focus on stores for children and higher-income shoppers. It is also optimizing the international portfolio, with focus on key markets and licensed models. Another priority is the continued expansion of the company’s e-commerce channel, which accounts for about 17% of total sales. The target is to raise the share of digital sales to 25% in the next three years.

Risks

Meanwhile, weak margin performance, reflecting higher markdowns and increased promotional activity, could be a concern in the near future. While the retail market is witnessing a return to discretionary spending — after shoppers across markets cut down on non-essential items during the pandemic — elevated inflation and economic uncertainties would remain a drag on people’s spending power.

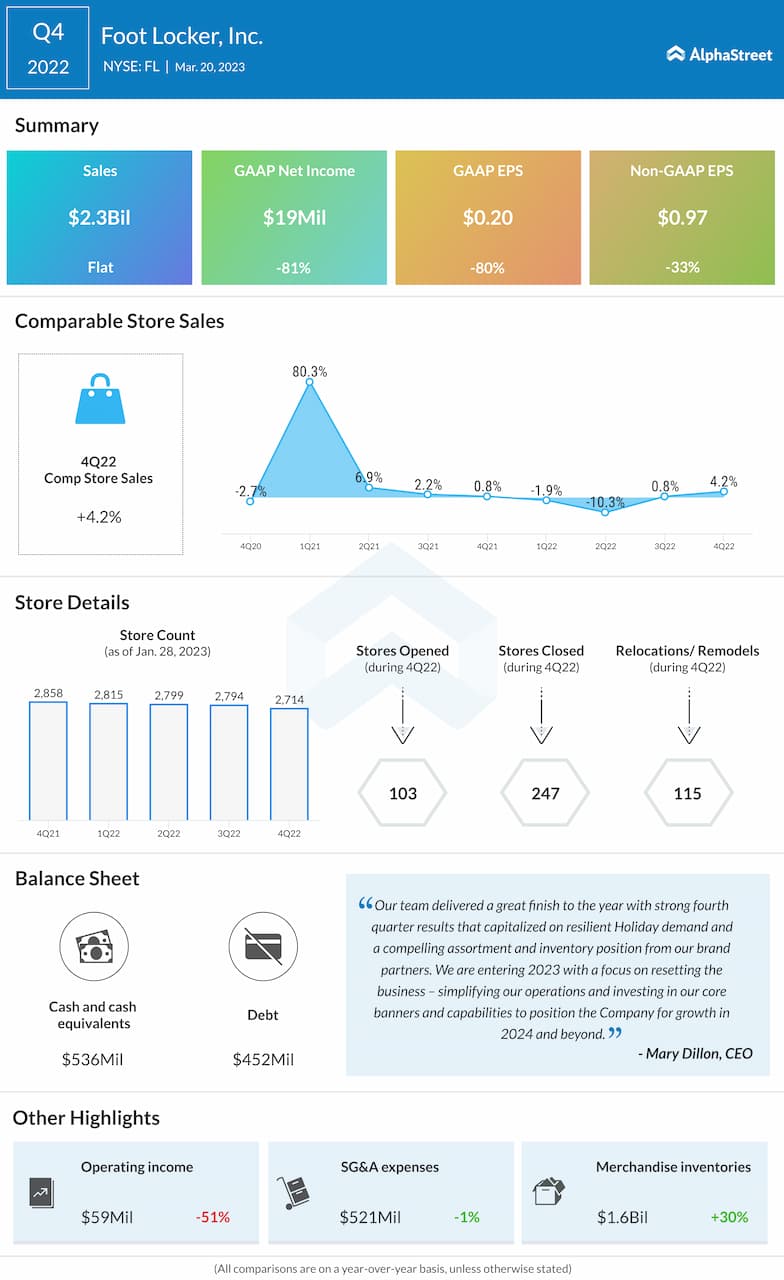

After slipping into the negative territory in the first half of 2022, comparable store sales recovered as the year progressed, with 0.8% and 4.2% growth in the third quarter and fourth quarter respectively. Net sales remained broadly unchanged at $2.3 billion in the January quarter when adjusted profit plunged 33% from last year to $0.97 per share. Earnings, however, exceeded estimates, continuing the long-term trend.

Outlook

Gross margin decreased by 290 basis points from last year. Looking ahead, Foot Locker executives predict that both net sales and comparable store sales would decline in mid-single digits in the whole of 2023. It will translate into adjusted earnings of $3.35-$3.65 per share, the mid-point of which is slightly below the FY22 level and comes in below consensus estimates.

Nike looks stable despite modest holiday quarter. Is the stock a buy?

“We are proud of Foot Locker’s role in influencing and serving the global sneaker community, and next year, we will celebrate the 50th anniversary of the iconic Foot Locker brand. We are incredibly excited to introduce our “Lace Up” plan with a new set of strategic imperatives and financial objectives that are designed to set us up for success for the next 50 years,” said Foot Locker’s CEO Mary Dillon.

Shares of Foot Locker traded up 7% on Tuesday afternoon. They have increased by about 14% so far in this year.