Goldman Sachs Group Inc. (NYSE: GS) reported a 26% dip in earnings for the fourth quarter of 2019 due to higher operating expenses. The bottom line missed analysts’ expectations while the top line exceeded consensus estimates.

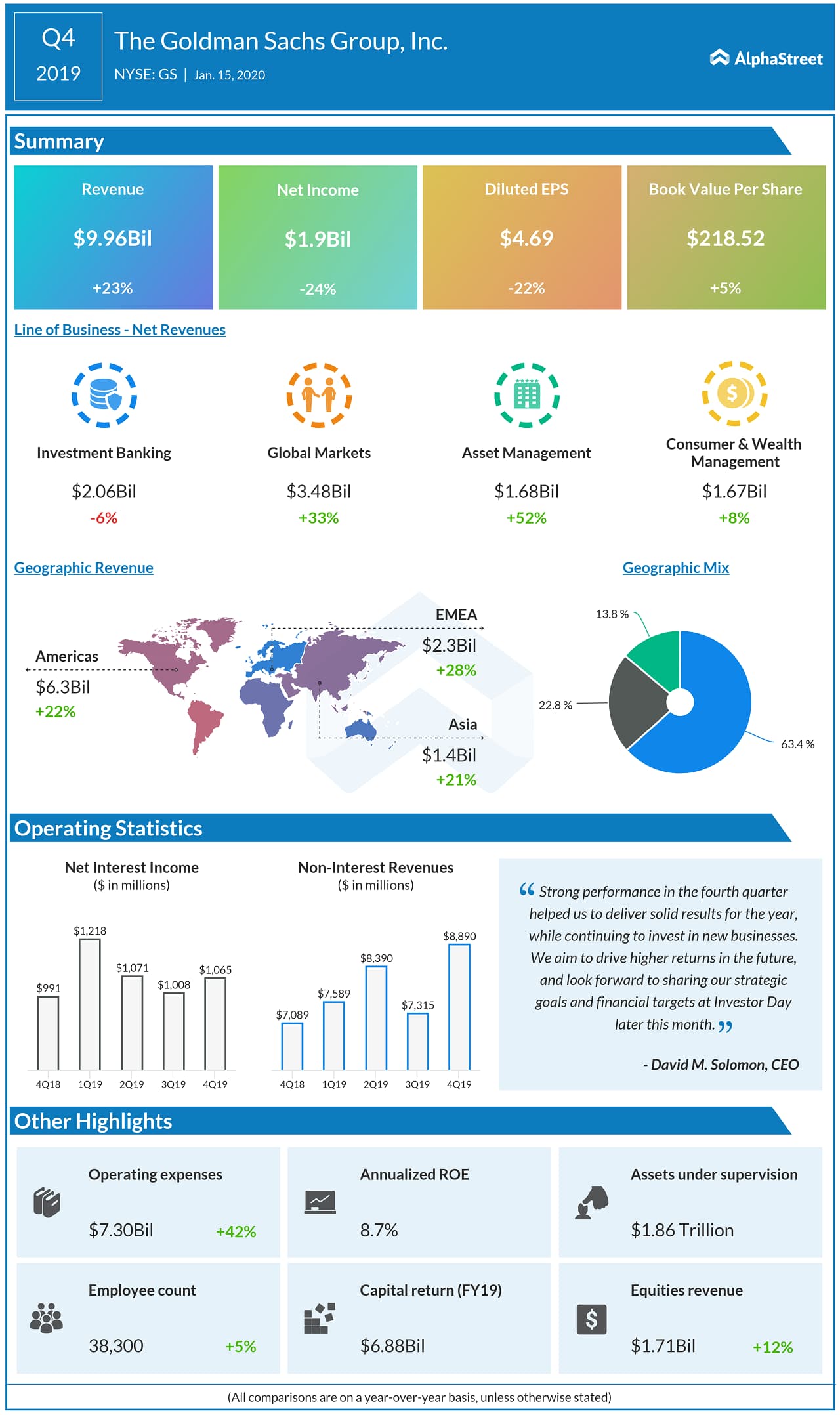

Net income applicable to common shareholders plunged by 26% to $1.72 billion or $4.69 per share. Total revenue climbed by 23% to $9.96 billion driven by significantly higher net revenues in Asset Management and Global Markets. Analysts had expected EPS of $5.46 per share on revenue of $8.51 billion for the fourth quarter.

Book value per common share was $218.52, 5% higher compared to the end of Q4 2018. Provision for credit losses rose 51% to $336 million from last year, mainly due to higher impairments.

Last week, the company announced that beginning with the fourth quarter, it will report its results in four new business segments that include Investment Banking, Global Markets, Asset Management, and Consumer & Wealth Management.

For the fourth quarter, revenue from Investment Banking declined by 6% due to lower industry-wide completed mergers and acquisitions volumes in financial advisory and a decline in revenue in corporate lending. This was partially offset by significantly higher revenue in Underwriting driven by asset-backed activity and higher revenue in equity underwriting.

Revenue in Global Markets increased by 33% driven by higher revenue in FICC intermediation, a rise in equities financing revenue, reflecting improved spreads and higher average customer balances, and equities intermediation.

Asset Management revenue jumped by 52% helped by significant net gains in public and private equities, higher gains from investments in debt instruments, and the impact of higher average assets under supervision. This was partially offset by a lower average effective fee due to shifts in the mix of client assets and strategies.

Consumer & Wealth Management revenue increased by 8% backed by higher average assets under supervision. This was partially offset by lower incentive fees, while revenue in private banking and lending was essentially unchanged.

On January 14, the board of directors declared a dividend of $1.25 per common share. This dividend will be paid on March 30, 2020, to shareholders of record on March 2, 2020. During the fourth quarter, the company returned $2.62 billion of capital to shareholders, which includes $2.16 billion of share repurchases and $453 million of common stock dividends.

Read: Western Digital stock jumps to yearly high on recovery stance

From the macro perspective, the company remains positive about the accelerating global growth in 2020 as gross domestic product growth is predicted to rise by 2.2% and 3.4% in the US and global, respectively. In 2021, the GDP growth is projected to rise by 2.4% and 3.6% in the US and worldwide.

The GDP growth expectations are backed by strong consumer sentiment, low global inflation, and low US unemployment. However, a few macro concerns are likely to impact the markets during this year that includes US-China trade, Brexit, and low global rates.