Shares of Home Depot Inc. (NYSE: HD) were up slightly on Wednesday. The stock has dropped 6% year-to-date. The company delivered mixed results for the fourth quarter of 2022 a day ago and provided a muted outlook for fiscal year 2023. Here are three factors that do not work in favor of the home improvement retailer:

Little growth in quarterly results

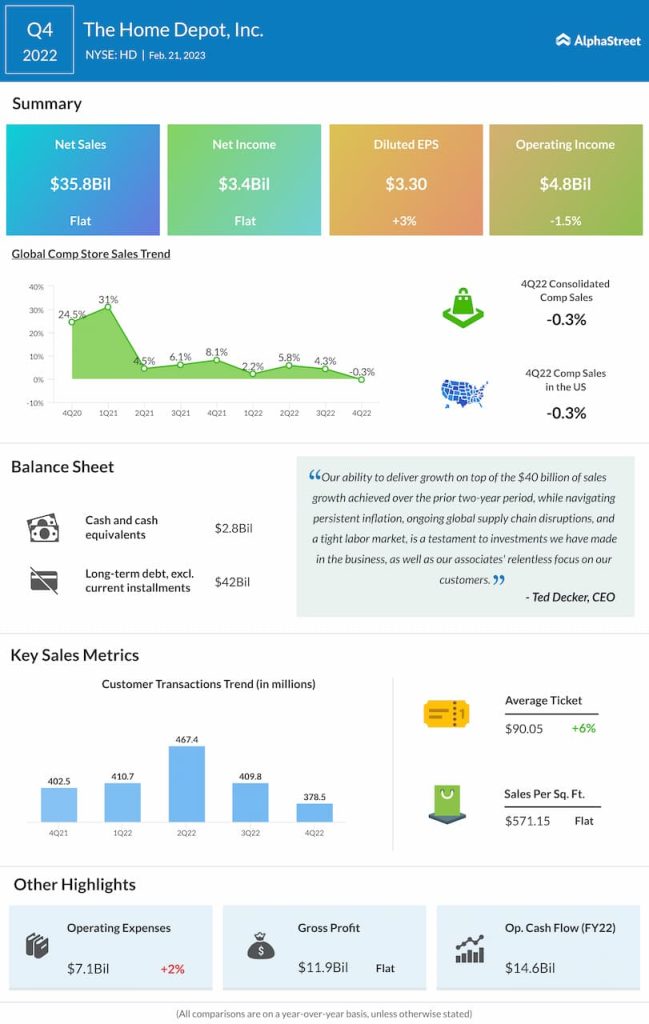

Home Depot’s net sales of $35.8 billion remained relatively flat in Q4 2022 compared to the year-ago period while its comparable sales fell 0.3%. Net earnings of $3.4 billion also saw little change from last year. EPS, however, rose nearly 3% to $3.30.

Expected slowdown in home improvement

On its quarterly conference call, Home Depot said its customers had remained relatively resilient amid high inflation through the most part of 2022 but during the third quarter, it started seeing a slowdown in some of its products and categories. This became more severe in the fourth quarter and together with lumber deflation, it led to comps coming in softer than expected.

In Q4 2022, comp transactions decreased 6%. However, inflation across product categories and demand for new products helped drive a 5.8% increase in comp average ticket. The company also recorded positive comps across half of its merchandising departments with units like building materials, plumbing and outdoor garden posting comps above the company average.

Home Depot expects demand for home improvement to moderate in 2023. Nevertheless it remains optimistic on the long-term prospects of the market and believes the company is well-positioned to take advantage of the growth opportunities in the space. In Q4, sales growth in the Pro customer category outpaced the DIY category and Pro backlogs still remain high compared to historical averages.

Bleak outlook

As mentioned on its call, Home Depot expects to see flat real economic growth and consumer spending in 2023. The company has also continued to see its transactions normalize over the past several quarters as consumers shifted their spending from goods to services. Home Depot believes that if this shift continues at the current pace, the home improvement market would see a decline in the low single digits.

For FY2023, the company expects its sales and comp sales growth to remain flat compared to last year. EPS is expected to decline by a mid-single-digit percentage. It also expects the planned employee compensation investment of $1 billion to impact its operating margin by around 60 basis points.

Click here to read the full transcript of Home Depot’s Q4 2022 earnings conference call