Shares of Home Depot Inc. (NYSE: HD) were up on Wednesday, a day after the company delivered better-than-expected results for its third quarter of 2022. Both the top and bottom line numbers beat expectations and the company reaffirmed its guidance for the year. Although there are broad concerns over the state of the housing market, Home Depot sees healthy demand for home improvement. Here are three points worth noting from the company’s Q3 report:

Strong quarterly results

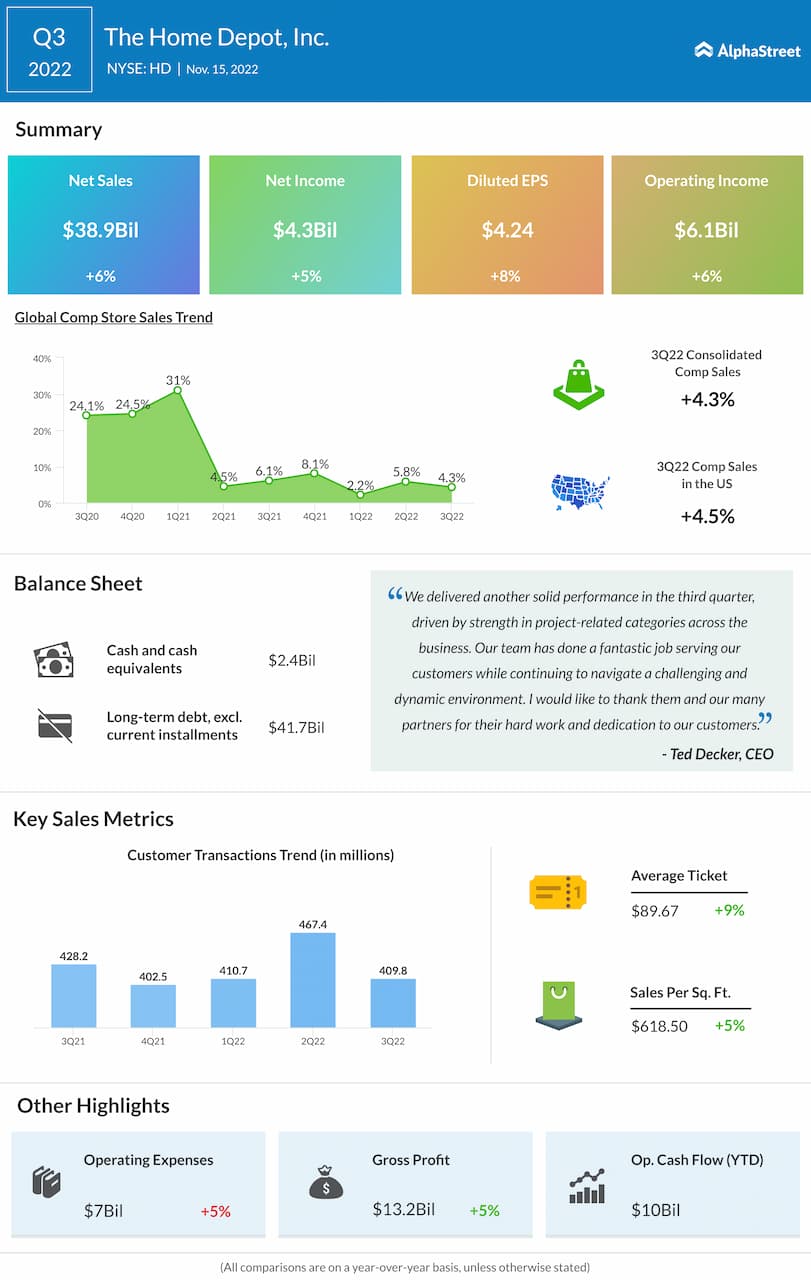

Home Depot’s revenue and earnings for Q3 2022 increased on a year-over-year basis and came ahead of expectations. Total sales grew 5.6% to $38.9 billion while EPS rose 8.2% to $4.24. Total comparable sales rose 4.3% while comp sales in the US increased 4.5%. Each of the company’s 19 US regions delivered positive comps versus last year. The strong quarterly performance was fueled by strength in project-related categories across the business.

Home improvement demand

Home Depot witnessed solid demand for home improvement projects during the third quarter. The company saw year-over-year growth with both Pro and DIY customers along with momentum in its project business during the period. In Q3, comp average ticket increased 8.8%, driven by inflation across product categories and demand for new products. Big-ticket comp transactions, or those above $1000, were up 10.1% YoY.

The company saw positive comps for categories like building materials, plumbing, lumber, paint and hardware during the quarter. Home Depot is seeing momentum with both Pro and DIY customers and it continues to work on building a unique Pro ecosystem that will help it grow share in a $450 billion addressable Pro market.

The company sees strong demand for home improvement projects as consumers still spend a lot of time at home and these homes continue to age. High home prices are also likely to drive demand for home improvement.

Outlook

Home Depot reaffirmed its guidance for fiscal year 2022. The company expects comparable sales to grow approx. 3% and EPS to grow in the mid-single digits. Operating margin is expected to be around 15.4%. Despite concerns on the housing market seeing a slowdown and inflation impacting home improvement, Home Depot remains confident about its prospects.