Intel Corporation (NASDAQ: INTC) has adopted a multi-pronged strategy to return to high-growth mode, including the development of new-gen chips and the launch of a systems foundry designed to manufacture AI chips for customers. The company ended fiscal 2023 on a positive note, riding the solid consumer momentum and demand recovery in the PC market.

The semiconductor giant has been on the path to a major transformation, especially after Pat Gelsinger took the helm as CEO about three years ago, with the highlight of the program being the restructuring of the manufacturing business with a focus on capacity expansion and AI capabilities.

Investing in INTC

To achieve the financial flexibility needed to invest in new projects, the company last year cut the quarterly dividend and called it a move aimed at positioning itself “to create long-term value.” For Intel’s stock, 2023 was a recovery period as it bounced back from a multi-year low in the early weeks and maintained an uptrend throughout the year. However, the momentum waned as it entered 2024 and has lost about 22% since the beginning of the year.

The valuation looks favorable, and those who have an eye on INTC should add it to the watchlist as the stock is likely to regain strength this year. The company bets big on the expansion of its foundry business, though the segment suffered a loss last year. It is estimated that the new fab facilities will come online next year and achieve breakeven by 2027. The company has secured $8.5 billion in government grants for the foundry project, which requires heavy investment to scale and become profitable.

Earlier, Intel officials issued optimistic guidance for the first quarter, projecting continued revenue and earnings growth. For the long term, the firm bets on new product launches and upcoming fab facilities to drive growth. Recently, the Intel Gaudi 3 AI accelerator was introduced, a high-performance chip designed to boost artificial intelligence workloads in enterprises. The new processor will enable the company to compete effectively with market leader Nvidia.

Results Beat

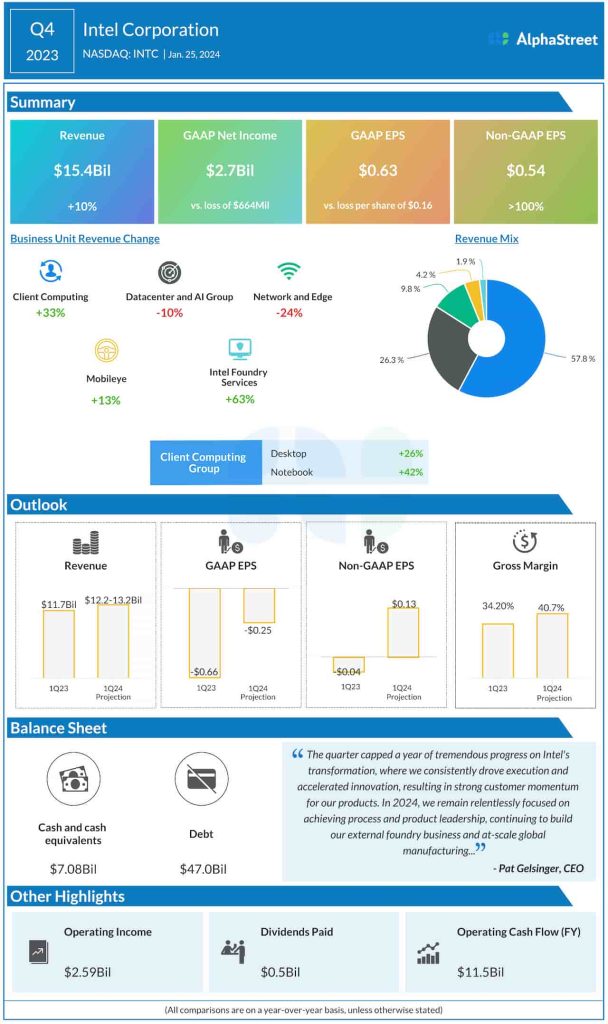

The tech firm delivered stronger-than-expected earnings and revenues in the past four quarters, even as the demand for computing products gained momentum. In the December quarter, adjusted profit more than doubled to $0.54 per share, aided by a 10% increase in revenues to $15.4 billion. The growth was driven by continued recovery in the Client Computing segment, which creates and sells computing products for consumers and businesses. That was partially offset by lower Datacenter and Network revenues.

“As we look into Q1, our core business, including client-server and edge products continues to perform well and is tracking to the lower end of seasonal. However, discrete headwinds, including Mobileye, PSG, and business exits, among others, are impacting overall revenue, leading to a lower Q1 guide. Importantly, we see this as temporary, and we expect sequential and year-on-year growth in both revenue and EPS for each quarter of fiscal year ’24,” said Gelsinger during the Q4 earnings call.

Bullish Outlook

Intel sees continued uptick in revenue performance as it enters the new fiscal year. That should translate into strong margin growth in the first quarter when the company is expected to swing to profit from a loss in the prior-year quarter. The Q1 report is scheduled for release on April 25, after the closing bell, with analysts predicting a double-digit growth in revenues to $12.8 billion. They expect the company to earn 14 cents per share in Q1, compared to a loss of four cents last year.

Intel’s stock experienced some weakness this week, extending the decline seen since the beginning of the month. It traded lower on Tuesday afternoon and stayed below the long-term average.