Shares of Pinterest, Inc. (NYSE: PINS) dropped this week after the image-sharing platform reported weaker-than-expected Q4 revenues and issued cautious guidance for the first quarter. After turning profitable a few years ago, the company has maintained positive earnings in almost every quarter, despite the disruptions caused by the pandemic.

While its unique business model gives the company an advantage over other social media platforms, the current weakness in the advertising market is putting pressure on revenues. The stock made strong gains ahead of Monday’s earnings, reflecting the market’s optimism about the company’s finances. But the short-lived momentum waned soon after the announcement and the shares have dropped about 8% since then.

Valuation

PINS maintained an uptrend throughout last year, though it experienced high volatility, and entered 2013 on a high note. The question is whether it would create reasonably good shareholder value this year. Right now, the valuation is cheap, but softening revenue growth and the management’s weak guidance show that Pinterest is not immune to the headwinds the technology sector is currently facing. So, it doesn’t seem to be the right time to either buy or sell the stock. Prospective investors can consider adding it to the watchlist.

Check this space to read management/analysts’ comments on quarterly reports

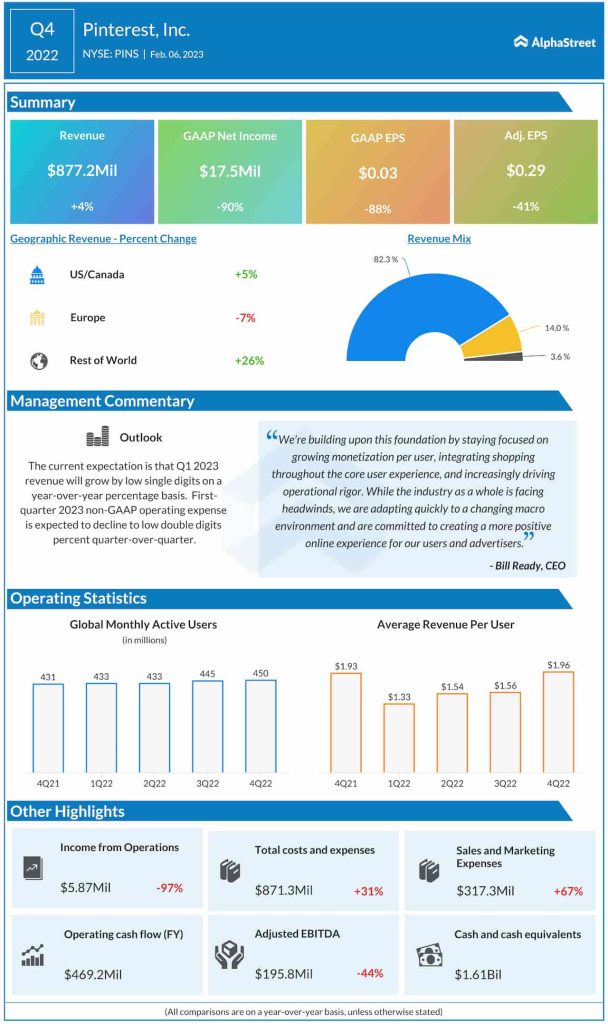

Currently, the company’s growth strategy is focused on integrating the online shopping feature at all levels and further increasing monetization, leveraging the continued increase in revenue per user. The company has expanded its user base at a slow but steady pace in recent quarters and ended the fiscal year with around 450 million users, which is up 4% from 2021.

Financials

It is estimated that advertisement income would recover in the long term as the present challenges ease – such as the choppy macro environment and reduced ad spending due to high inflation. In the fourth quarter, adjusted earnings beat estimates for the second time in a row, though the latest number dropped 41% from last year to $0.29 per share. An increase in revenues in the US/Canada markets more than counterbalanced the contraction in Europe, and the top line moved up 4% annually to $877.2 million.

Commenting on the results, Pinterest’s CEO Bill Ready said, “we built and shipped new ad tech and measurement solutions that resulted in improved returns for our advertisers. And we’re just getting started. I have a strong conviction that we will continue to innovate and deliver value to our users and business partners. We grew global MAUs in Q4 to 450 million, up both sequentially and year over year. Our global mobile app users, which account for over 80% of our impressions and revenue, grew 14%. And our U.S. and Canada mobile app users grew 5%, accelerating from last quarter.”

Outlook

The management currently expects first-quarter revenues to grow by low single digits, which is sharply below the consensus estimates. The weak guidance mainly reflects the weakness in enterprise spending, and it echoes the concerns raised by ad-supported social media peers like Meta Platforms, Inc. (NASDAQ: META) and Alphabet, Inc. (NASDAQ: GOOGL, GOOG), which reported unimpressive operating results recently.

AMZN Earnings: All you need to know about Amazon’s Q4 2022 earnings results

Pinterest also announced the departure of Todd Morgenfeld, its chief financial officer and head of business operations He will be stepping down in July this year. Earlier, the company had laid off around 150 employees as part of streamlining the business.

Pinterest’s stock remained in the red after the post-earnings sell-off and traded lower throughout Wednesday’s session. However, all along it stayed above the 52-week average.