Uber (NYSE: UBER) and Lyft (NASDAQ: LYFT) may be birds of the same feather, but both the ride-hailing firms are poles apart. While both companies are losing money at a rapid rate, they are still poised to transform the transportation industry in the years to come, and in turn, reward loyal investors. The rewards are, however, likely to come at different points of time.

At present, both the stocks hardly present any solid reason to keep under the radar: Uber is down 24.4% from its offer price, while Lyft is down 28.6%. Despite these declines, the stocks are still considered overvalued by market watchers.

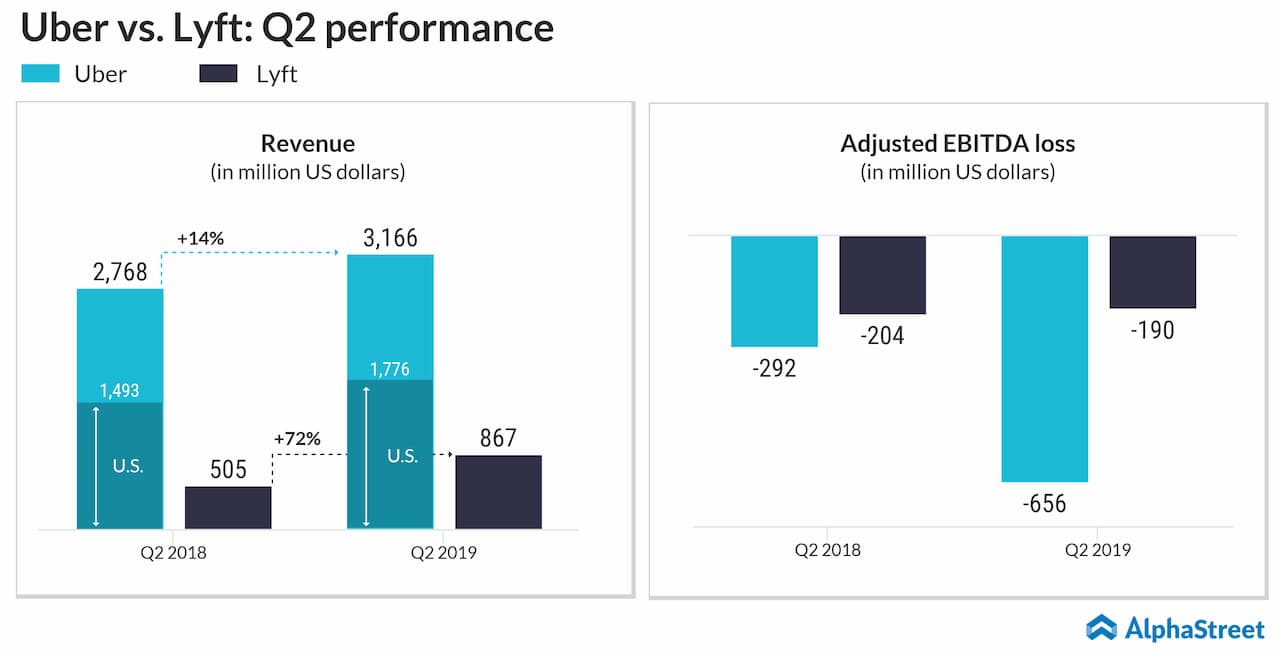

Lyft in the shorter term

However, on a closer watch, Lyft appears to have an edge in the shorter term. Look at the most recent earnings figures. Revenues climbed by 72% to $867.3 million, while adjusted EBITDA loss shrunk to $190 million from $204 million a year ago. These numbers lend more credibility to the company’s plan of action towards profitability.

Uber, meanwhile reported adjusted EBITDA loss that more-than-doubled to $656 million during the same period.

Lyft also has a stable management that keeps driving top-line

growth through innovative strategies, besides offering a ride-hailing service

that is more friendly to users. Even when it comes to autonomous driving

technology, which is seen as the key to profitability in the automobile industry,

Lyft scores above Uber, thanks to the numerous partnerships it has inked with

firms such as Alphabet (NASDAQ:

GOOGL), Ford Motor (NYSE: F)

and Irish autonomous technology company Aptiv (NYSE: APTV).

On the other hand, Uber’s self-driving ambitions have been marred by controversies including a fatal accident in Arizona and a tiff with Alphabet’s Waymo. It does have a partnership with Toyota and its self-driving cars are back on the road, but the controversies have wasted away a lot of time that could have been used productively.

Uber in the longer term

While these factors give Lyft an upper hand in the short term, if you are willing to widen your waiting period to a couple of years, it is likely to be Uber that delivers. Uber CEO Dara Khosrowshahi insists that his company is the Amazon (NASDAQ: AMZN) of cars. Well, that’s of course for time to decide, but the diversification of business outside ride-hailing should cushion the stock, in the event of an unprecedented breakdown in the auto industry.

Separately, the food delivery business is still in its nascent stages, suggesting it has a much higher scope of growth, even when its ride-hailing business slows down. According to Second Measure, UberEats is currently the third biggest food delivery app in the US in terms of sales with a market share of 12.8%. It trails DoorDash, with a market share of 36.5% and Grubhub (NYSE: GRUB) with a share of 33.3%.

The expansion into other areas such as Uber Copter and Uber Freight should also make it attractive to investors who are looking at stocks with growth potential. The logistical advantages of primarily being a ride-hailing business should help boost growth in these sister units.

In the core ride-hailing business, Uber continues to hold a dominant status, with almost 71% market share. Despite all the growth Lyft has showcased over the past two years, it has hardly translated into market share growth, which continues to be at around 27%. Unless there occurs some drastic change of equations brought about by the introduction of driverless tech, Uber is likely to continue to maintain the dominant status.

Under Khosrowshahi, Uber is a more stable firm and confidence in the stock has improved. This is evident from the action of numerous hedge funds, which are buying more shares of Uber, but cutting down their stake on Lyft.

Undoing and repairing the damages done by his predecessor could take some time, but with the slow and steady approach that Khosrowshahi has adopted, things could turn for the better faster than expected.