Shares of PepsiCo, Inc. (NASDAQ: PEP) were down over 2% on Friday, following the announcement of the company’s fourth quarter 2023 earnings results. The beverage giant delivered mixed results for the quarter as earnings beat estimates but revenue fell short. Here are the main takeaways from the quarterly report:

Quarterly numbers

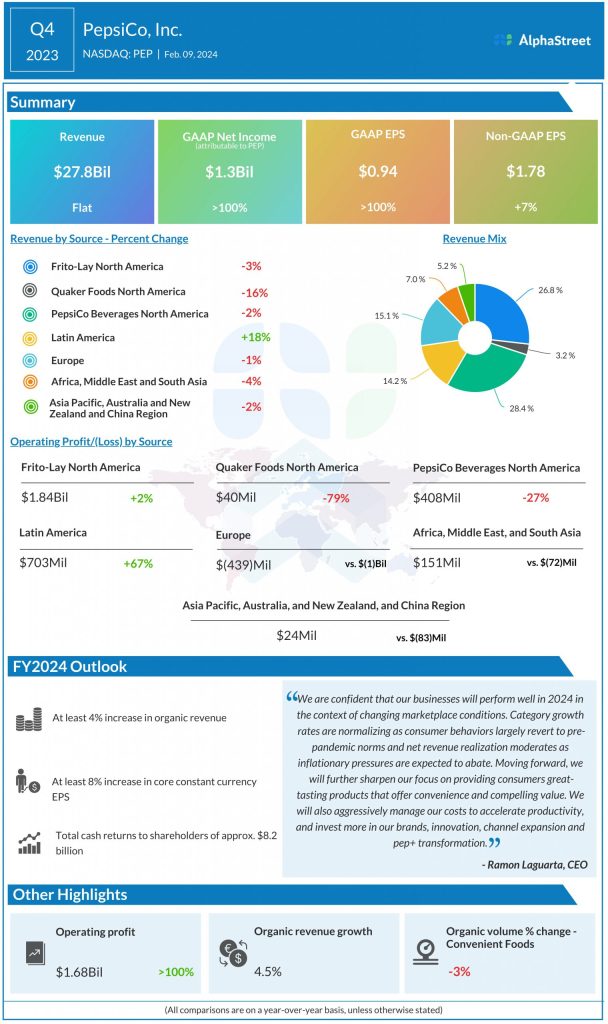

PepsiCo’s net revenues dipped 0.5% year-over-year to $27.8 billion in Q4 2023, missing estimates of $28.4 billion. Organic revenue growth was 4.5%. GAAP EPS more than doubled to $0.94 from last year. Core EPS rose 7% YoY to $1.78, beating projections of $1.72.

Business performance

In the fourth quarter, on an organic basis, global convenient foods revenue increased 5% and global beverage revenue increased 4%. The company saw organic volume for its businesses decline due to a moderation in category growth rates as consumers chose smaller pack sizes for the sake of convenience and affordability. Business disruptions due to geopolitical tensions, and a product recall at Quaker Foods North America also took a toll on organic volumes.

On a reported basis, PepsiCo saw revenues fall across all its segments except Latin America. However, on an organic basis, revenues grew across all segments, barring Quaker Foods North America, and Asia Pacific, Australia and New Zealand and China Region. Quaker Foods saw organic revenue decrease 10% due to product recalls and soft category growth.

Outlook

On its quarterly call, PepsiCo said it expects its global beverage and convenient foods categories to remain resilient in 2024, but category growth rates are expected to normalize and moderate compared to the last couple of years. The company also said that consumers are likely to remain watchful with their budgets and choiceful with their purchases.

Even though geopolitical tensions and macroeconomic volatility are likely to remain high in some regions, the Lays owner expects its international organic revenue growth to exceed organic revenue growth in North America. PepsiCo also expects its business to be impacted by the effects of the Quaker Foods product recalls and international conflicts in certain markets during the first half of 2024.

The company expects organic revenue growth of at least 4% and core constant currency EPS growth of at least 8% in FY2024. Core EPS for the year is expected to be at least $8.15, up 7% YoY.