We are living in an era where electronic transactions have become mainstream, especially after the pandemic sparked a digitalization spree. Consumers and businesses that have embraced digital payments channels are unlikely to go back to the traditional method, and that is good news for payment services firms like Mastercard Inc. (NYSE: MA).

A Safe Bet?

After making steady gains over the past several months and hitting a record high in April this year, Mastercard’s shares are currently trading close to the prior-year levels. The stock, which hovered near the $400-mark at its peak, has become more affordable now. From an investment perspective, the pros far outweigh the cons of Mastercard. Having created shareholder value consistently over the past several years, it is one of the safest Wall Street stocks.

Read management/analysts’ comments on Mastercard’s Q2 2021 earnings

Since the dividend yield is relatively low, though the company hiked the dividend regularly in recent years, income investors do not have much to expect. While it is difficult to choose between Mastercard and its arch-rival Visa, Inc. (NYSE: V), the latter has a broader network and is less expensive. Considering their simple and transparent business that is scalable, the companies look poised to stay unchallenged though new players keep entering the fast-growing payments market.

With uncertainty looming over reopening, the management has embarked on a diversification plan to better align the business with the changing market scenario. The acquisition of identity verification solutions provider Ekata a few months ago was an important step in that direction.

In the Pipeline

There are more technology-focused growth initiatives in the cards, even as new trends like remote work take root across the globe. Currently, the management’s key priorities are to ramp up core products, drive digital enablement in retail stores and online, and advance the multi-rail strategy.

It needs to be noted that domestic business has mostly regained the lost momentum and volumes reached above the pandemic level in the most recent quarter. However, Mastercard will continue to feel the pinch of the slowdown in cross-border business in the near term, owing to the closure of holiday destinations and travel restrictions. While the emergence of new COVID variants remains a concern, it is widely expected that more international borders would open in the second half.

We believe that most markets are at a growth phase domestically as cross-border spending is now starting to normalize and border restrictions are being relaxed. Looking at Mastercard spending trends, switched volumes continue to improve quarter-over-quarter, with strength across all products. Debit spend remains elevated, and we are seeing further recovery in credit, driven in part by the return of travel and increased discretionary spending.

Michael Miebach, chief executive officer of Mastercard

ADVERTISEMENT

Strong Q2

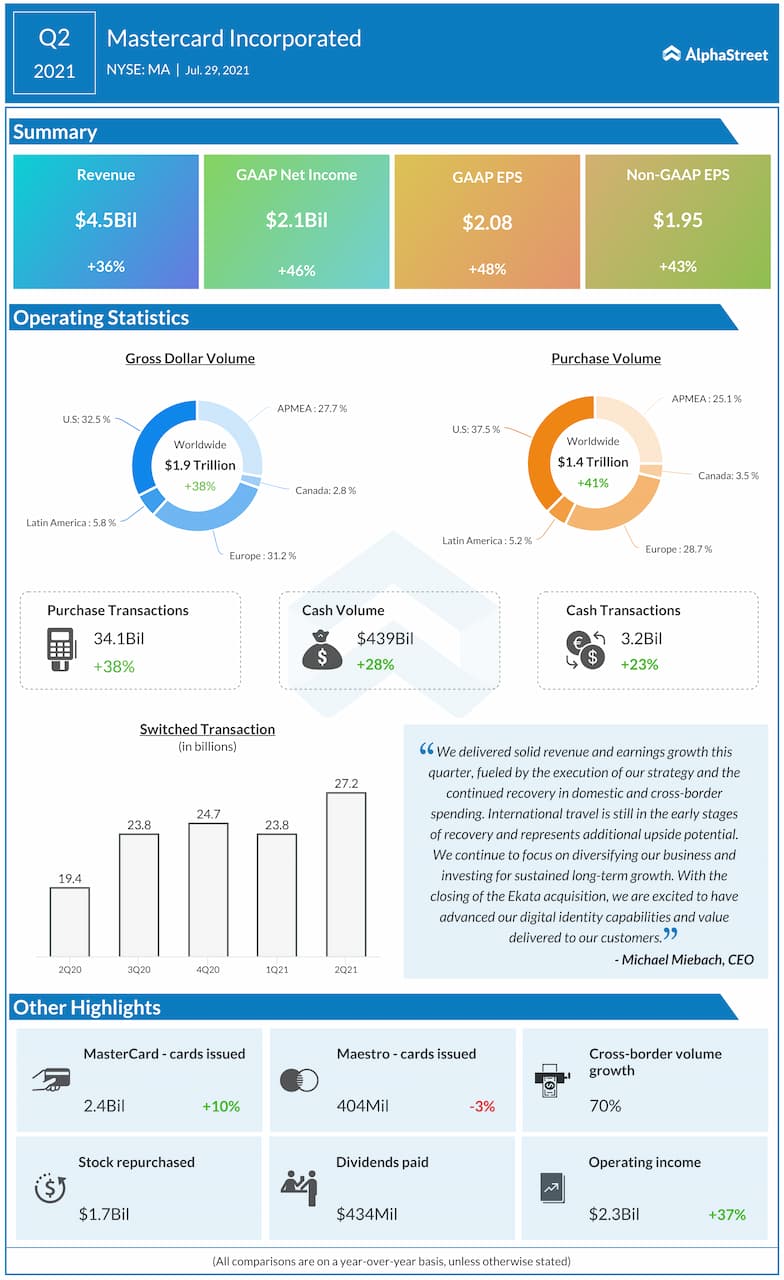

Mastercard’s earnings performance slowed down during the last fiscal year and in early 2021 while revenues remained almost flat, but the bottom-line numbers exceeded the market’s projection. In the June quarter, transaction volumes jumped supported by the ongoing recovery in domestic and international spending. Revenues rose 36% to $4.5 billion, which translated into a 43% increase in adjusted profit to $1.95 per share. The company will release its third-quarter results on October 27 before the opening bell.

After the recent pullback, the stock has once again moved above its long-term average. It opened at $353.91 on Friday and traded higher throughout the session. In the past six months, the shares declined by about 6%.