Shares of McCormick & Company Inc. (NYSE: MKC) were down over 5% on Thursday after the company missed expectations on its fourth quarter 2022 results and provided a lower-than-expected earnings outlook for the full year of 2023. The stock has dropped 10% year-to-date. Even so, the company remains optimistic about driving sales growth during the coming year.

Quarterly numbers

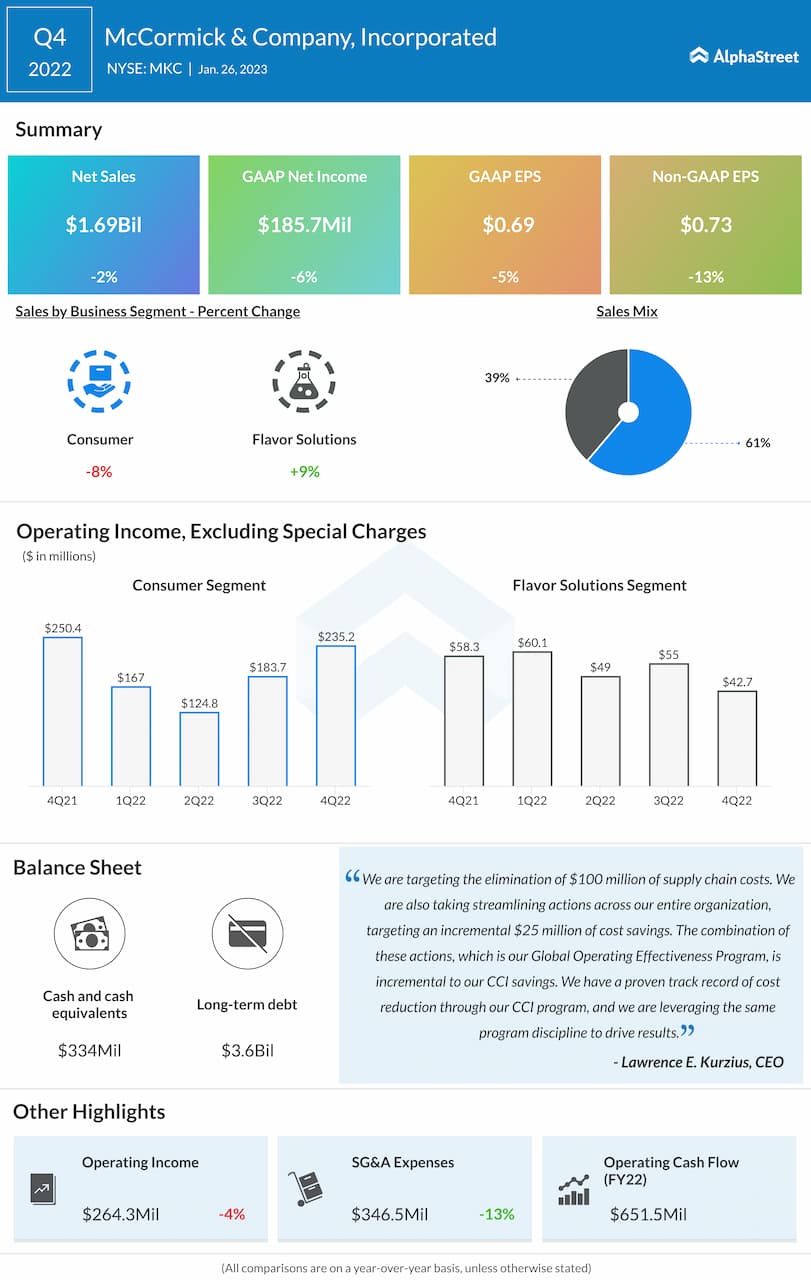

For the fourth quarter of 2022, McCormick delivered net sales of $1.69 billion, which fell 2% from the prior-year quarter and missed estimates. Sales grew 2% in constant currency, reflecting a 9% growth from pricing actions partly offset by a 3% drop in volumes. Adjusted EPS declined 13% year-over-year to $0.73, missing the consensus target.

Business performance

During the fourth quarter, reported sales growth was mainly impacted by pandemic-related disruptions in China, barring which total sales would have been flat compared to the year-ago period, or grown 4% in constant currency.

In the Consumer segment, sales declined 8% YoY on a reported basis and 4% on a constant currency basis, mainly due to lower volume and product mix. The decline was partially offset by pricing actions. Sales also declined across all geographic regions on a reported basis, mainly due to volume declines and product mix. However, the company saw strong consumption trends within this segment, with total branded consumption rising 6% in the US during the quarter.

McCormick saw strong momentum in the Flavor Solutions segment during the fourth quarter, with sales rising 9% YoY on a reported basis and 14% on a constant currency basis. The sales growth was driven by pricing actions, higher volume and product mix.

Sales in the Americas rose 13% fueled by high demand from packaged food and beverage companies as well as higher sales to branded foodservice customers. In the EMEA region, sales fell 2% while in the Asia/Pacific region, sales remained flat, on a reported basis. On a constant currency basis, both regions saw double-digit sales growth.

Outlook

Looking ahead into 2023, McCormick believes its broad portfolio will help it meet the growing demand for flavour around the world. The company is taking advantage of consumers’ growing interests in trends like healthy and flavorful cooking, digital engagement, placing more value on trusted brands and adopting practices that serve a particular purpose.

In 2023, McCormick expects to see strength in its business driven by sales growth but EPS growth is expected to be weakened by higher interest expense and effective tax rate. The company expects sales to increase 5-7% versus 2022, driven mainly by pricing actions, which along with cost savings are expected to offset the impacts of inflation. Growth is also expected to be fueled by factors like brand strength, new products, brand marketing and category management.

For 2023, McCormick expects reported EPS to be $2.42-2.47 compared to EPS of $2.52 in 2022. Adjusted EPS is expected to range between $2.56-2.61 compared to adjusted EPS of $2.53 in 2022. Analysts had predicted EPS of $2.90 for FY2023.

Click here to read more on consumer stocks