The unexpected surge in memory chip demand continues to drive revenue growth for semiconductor companies, but the persistent supply-demand imbalance has put some of them in a tough spot. Micron Technology, Inc. (NASDAQ: MU) has handled the situation effectively through capacity expansion, but the memory-chip titan might need to deal with another problem in the long term – surplus production.

Buy the Dip?

After climbing to a multi-year high in April, Micron’s stock hit a rough patch and pared most of this year’s early gains. But, the softness is unlikely to last long, rather MU is probably on its way to breaching the $100-mark and setting new records. Experts’ bullish estimates and the recent dip in value should bring cheer to prospective buyers. Moreover, last month the company kicked off dividend payment, declaring its first-ever dividend that is seen as a prelude to an extensive shareholder return program.

Read management/analysts’ comments on Micron’s Q3 earnings

Having ramped up the capacity for NAND and DRAM chips, an area where Micron is a market leader, the company enjoys an edge over rivals and looks better positioned to tap into demand-driven opportunities, especially in user devices, intelligent edge, and data-center. The healthy liquidity position – the company had a cash balance of $8.4 billion as of June 3, 2021 – should facilitate the smooth execution of growth plans going forward.

Long-term Issue

Meanwhile, it is estimated that the shortage of assembly materials and capacity constraints would persist across the semiconductor ecosystem in the remainder of the year and beyond, which would demand additional measures to ensure adequate supplies. Currently, the primary hurdle is the COVID-related disruption in markets where the company operates its production and assembly facilities. Also, considering the cyclical nature of the chip market, the additional capacity might lead to surpluses in the future.

Our assembly and test success was the result of a strategic decision we made several years ago to increase our captive footprint and strengthen relationships with suppliers and partners. We successfully mitigated the impacts of the drought in Taiwan with no reduction in our production output. Taiwan’s rainy season has begun, bringing with it sufficient water supply to support our manufacturing requirements. While the drought in Taiwan is behind us, the rise in COVID-19 cases in Malaysia, India, and Taiwan are a risk to our manufacturing operations and R&D activities in these regions.

Sanjay Mehrotra, chief executive officer of Micron

During the pandemic, elevated chip demand translated into strong top-line performance, marked by stable revenue growth. Each time, there was a corresponding rise in earnings. Over the past several years, the key numbers consistently topped the market’s prediction.

Blockbuster Q3

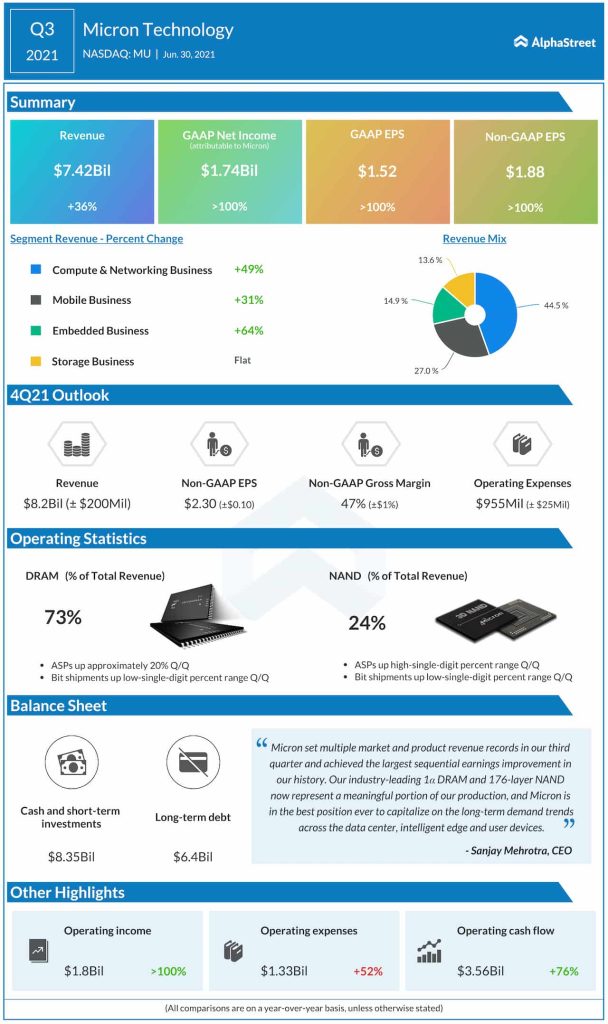

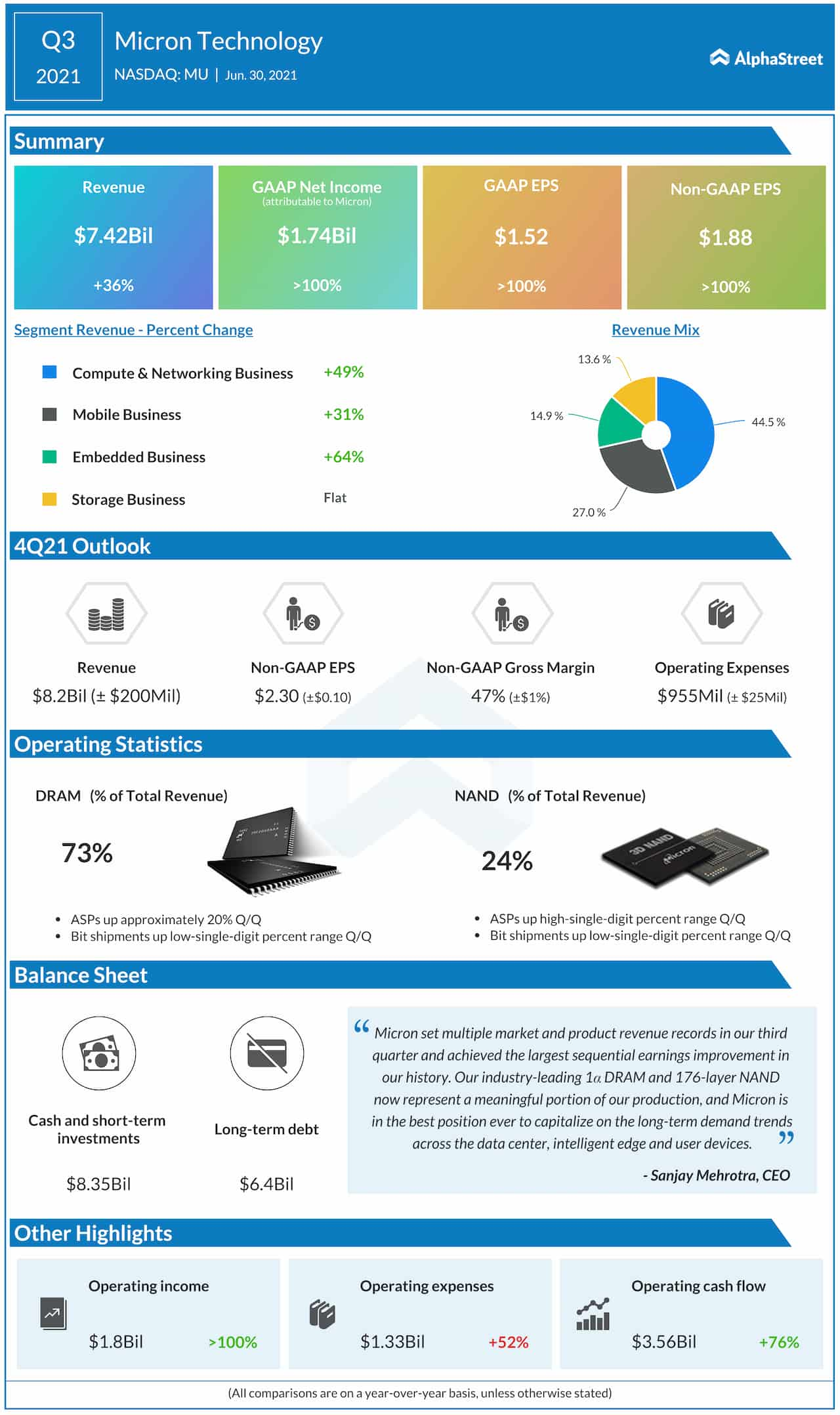

In the third quarter, earnings jumped to $1.88 per share from $0.82 per share a year earlier. Driving the profit growth, revenues advanced 39% annually to $7.42 billion. Market watchers had predicted slower growth for both profit and the top line. The embedded business exceeded $1 billion for the first time.

When the tech firm reports its fourth-quarter earnings on September 28 after regular trading hours, the market will be looking for a 36% jump in revenues to $8.2 billion. Adjusted profit is seen more than doubling year-over-year to $2.32 per share.

Why this thriving chipmaker remains an investors’ favorite

Last month, shares of Micron slipped below their long-term average and maintained a downtrend since then. This week, the stock traded close to the levels seen at the beginning of the year. It opened Monday’s session at $73.50 and traded higher during the early hours.