The chip shortage that threw supply chains out of gear across the globe is far from over, and semiconductor companies are busy exploring ways to increase production to deal with the crisis. Broadcom, Inc. (NASDAQ: AVGO) has been riding the upheaval in the chip market, especially after the COVID-driven digital transformation gathered pace.

A Long-term Bet

Broadcom’s stock rallied after this week’s positive earnings report and is currently hovering near its recent peak. It is estimated that the shares would make further gains and go well past the $500-mark in the coming months. The company’s finances will continue to benefit from favourable demand conditions and the digital shift. For those who can afford AVGO, it is an investment option with good long-term prospects. Currently, the consensus rating on the stock is strong buy.

Read management/analysts’ comments on Broadcom’s Q3 results

The company is becoming popular among income investors also, thanks to the dividend hikes. With an impressive annual payout of $14.40, it is probably emerging as a dividend aristocrat, supported by healthy cash flows. It needs to be noted that the payout has increased consistently since the first distribution more than a decade ago. This week, the board approved a dividend of $3.60 per share, which represents a much bigger yield than the average of S&P 500.

Focus on Cloud, 5G

Currently, the major growth drivers are widespread adoption of wireless technology — bolstered by the 5G ramp – and cloud migration, which is expected to continue in the foreseeable future. The demand for the company’s innovative processors made for high-speed communication is expected to be strong because the fast-growing 5G market remains largely untapped. Overall, the ongoing pickup in enterprise spending is translating into sales growth for Broadcom.

From Broadcom’s Q3 2021 earnings conference call:

“The end users just go to our distributors and wipe out our inventory, multi-inventory there. So we show a resale growth of 55% and we all know that’s not real demand, people are building up the buffer, there’s a certain level of panic buying. Take that across all segments of semiconductor markets today, you see that kind of behavior unless you — as call key suppliers, we put in careful discipline to manage supply to where demand is really needed as opposed to where OEMs or even end-users are just building up buffers, bucket of buffers everywhere.“

Capacity Woes

The diversification into the infrastructure software business a few years ago, which was further supported by a couple of acquisitions, proved to be fruitful. But in the long run, Broadcom’s increasing reliance on external fabs like Taiwan Semiconductor Manufacturing Company Limited (NYSE: TSM) — which is expected to add to costs — can be a disadvantage as far as pricing is concerned.

Intel Q2 2021 profit, revenue beat estimates

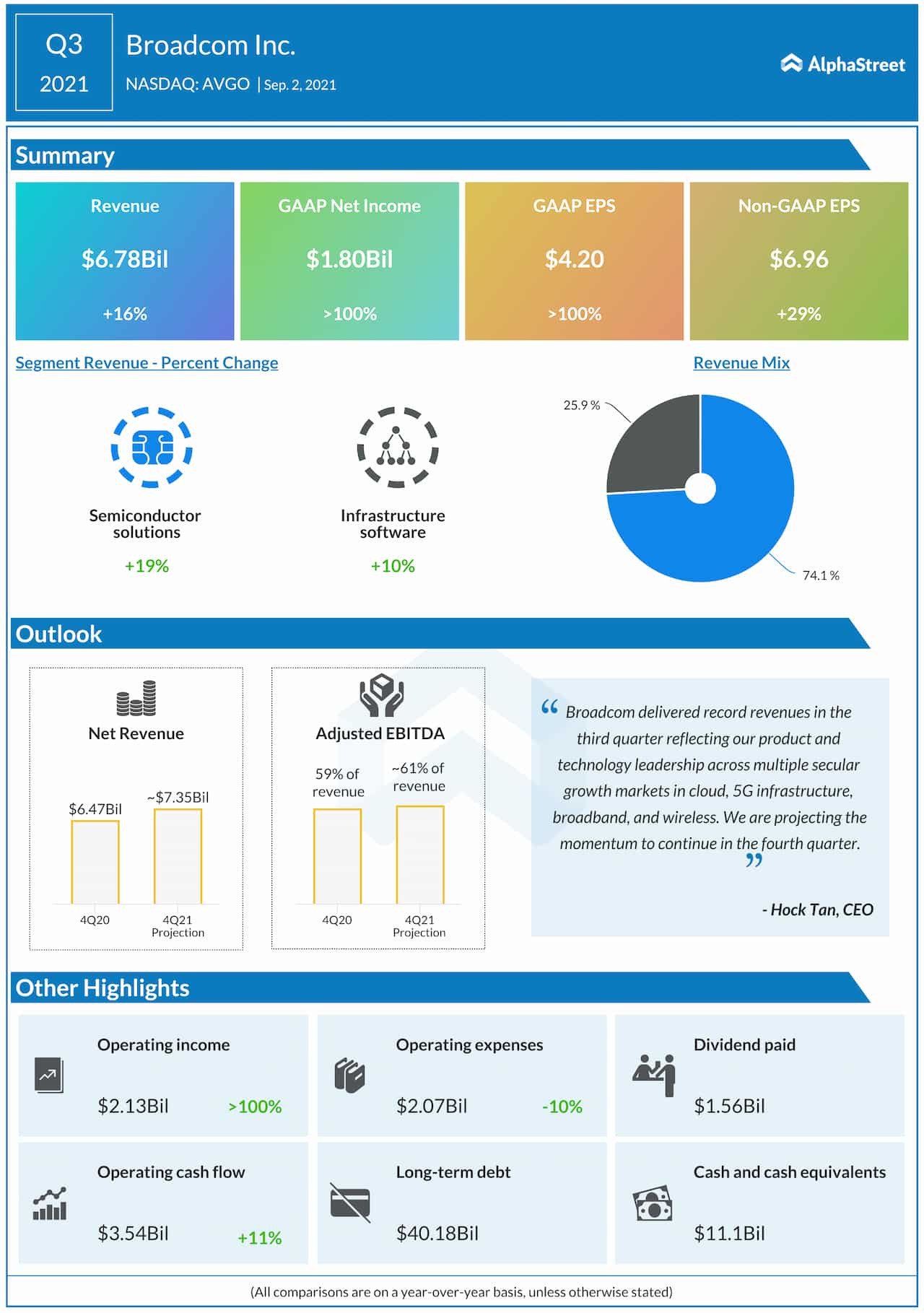

In the third quarter, the core Semiconductor Solutions segment grew in double digits, pushing up total revenues by 16% to $6.8 billion. That translated into a 29% growth in adjusted earnings to $6.96 per share. A marked decrease in operating costs also contributed to the bottom line. The numbers topped expectations. Encouraged by the positive outcome, the management is looking for strong year-over-over increase in fourth-quarter revenue and EBITDA.

Stock Gains

Broadcom’s stock has gained steadily since the earnings release and maintained the uptrend in the early hours of Wednesday’s session. It has gained 18% in the past eight months, often outperforming peers and the broad market.